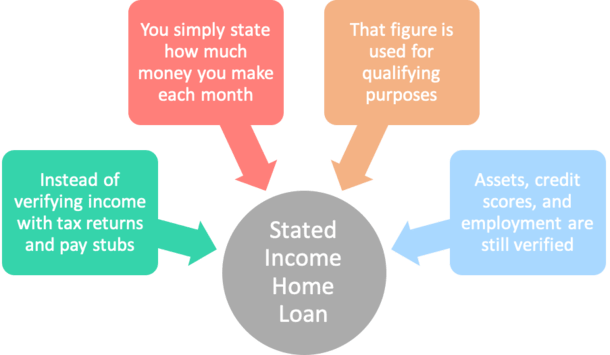

In short, stated income loans allow borrowers to simply state their monthly income on a mortgage application instead of verifying the actual amount by furnishing pay stubs and/or tax returns.

This simplified method was originally intended for self-employed borrowers with complicated tax schedules.

It became widespread in the lead-up to the financial crisis, often because borrowers found it that much easier to qualify for a loan by stating their income.

For that reason, stated income loans are also occasionally referred to as “liar’s loans” because it is suspected that many borrowers fudge the numbers in order to qualify for a home loan. Back to that in a minute.

How Does a Stated Income Loan Work?

- Instead of documenting and verifying your income when obtaining a home loan

- By providing the lender with IRS tax returns and employment pay stubs

- A gross monthly income figure is simply inputted on the home loan application

- And not actually verified by anyone!

Prior to the housing crisis in the early 2000s, it was very common to use stated income to qualify for a mortgage loan.

Instead of providing tax returns and pay stubs from your employer, you could verbally state your gross monthly income and that is what would be used for qualification.

Clearly this was a high-risk approach to home loan lending, which is why it’s basically a thing of the past. However, there are new versions of stated income lending, which I’ll discuss below.

A Mortgage Doc Type for Every Situation

To get a better understanding of what a stated income loan is, it may help to learn about the many different mortgage documentation types available. There are actually several types of stated loans these days.

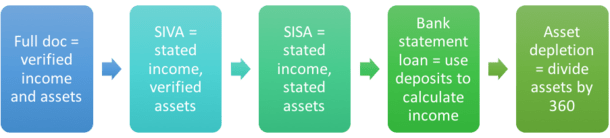

A full documentation loan requires that you verify income with tax returns and/or pay stubs and also verify assets by providing bank statements or similar asset documentation.

That’s just listed here for comparison sake; it’s not a stated income loan. It’s the typical way a mortgage borrower is underwritten.

A SIVA loan, or stated income/verified asset loan, allows you to state your monthly gross income on the loan application and requires you to verify your assets by furnishing bank statements or a similar asset document.

By state, I mean just inputting a gross monthly income figure on the loan application.

A SISA loan, or stated income/stated asset loan, allows you to state both your monthly gross income and your assets.

In this case, both items are simply stated, and the bank or lender will not ask you to verify the information.

In all these examples, a debt-to-income ratio will be generated because income figures are provided, even if it isn’t actually verified.

In cases where a borrower doesn’t even fill in the income box on the loan application, it is referred to as a no doc loan. See that page for more details.

Bank Statement Loans and Asset Qualification

- True stated income loans are rare these days

- Most lenders now require verified assets at a minimum

- Including bank statements, retirement accounts, etc.

- Meaning you may need to be asset-rich to qualify for a mortgage if your income won’t suffice

Nowadays, it’s a little more complicated. There are new methods of stating income post-mortgage crisis such as “alternative-income verification loans” and “bank statement loans.”

Bank Statement Loans

- Lender will ask for 12-24 months of bank statements

- And calculate your monthly income using deposit history

- Averaged over that time period

- To come up with qualifying income

Instead of simply stating what you make, the lender will ask for at least 12 months of bank statements, maybe 24, to determine your income. These can be personal bank statements, business bank statements, or both.

They will then calculate your monthly income by averaging those deposits over the accompanying 12- or 24-month period.

If you’re a self-employed borrower, you may also be asked to provide a Profit and Loss Statement (P&L) that substantiates the deposits.

Again, everything needs to make sense, and any large deposits will be flagged and require explanation.

In other words, taking out a loan or having someone make deposits into your bank account will likely be noticed/scrutinized by the underwriter.

Asset Qualification

- Lender adds up all your assets

- Subtracts your proposed loan amount from that number

- Then tallies up all your liabilities and multiplies them by X months

- If your remaining assets exceed your liabilities you may be approved

There is also a way of qualifying for a mortgage using just your assets, with no requirement to disclose income or employment.

This method requires borrowers to have a lot of liquid assets.

The lender usually adds up all your assets (checking, savings, stocks, bonds, 401k, etc.) and subtracts the proposed loan amount and closing costs.

Then they total up all your monthly liabilities, such as credit card debt, auto loans, etc. and taxes and insurance on the subject property and multiply it by a certain number of months.

Let’s assume a $400,000 loan amount and $800,000 in verifiable assets. And pretend our borrower owes $3,000 a month for their car lease, credit cards, and taxes/insurance.

They’ll multiply that total by say 60 (months) and come up with $180,000.

Since our borrower has more than $180,000 in verified assets remaining after the loan amount is deducted, they can qualify for the mortgage using this method.

Note that reserves to cover 2+ months of mortgage payments and closing costs will also usually be required.

Asset Depletion

- Lender adds up all your assets

- Then divides that total by 360 (months)

- Which is the length of most mortgages

- To come up with your qualifying monthly income

Then there’s so-called “asset depletion,” which again favors the asset-rich, income-poor borrower. These types of loans are actually backed by Fannie Mae and Freddie Mac and are calculated a bit differently.

Generally, the lender will take all your verifiable assets and divide them by 360, which is the typical 30-year term of a mortgage represented in months.

These assets may be assigned a 100% value if cash, and perhaps 70% if they are retirement funds and you are below retirement age. Once tallied up, the figure is divided by 360 and that is your qualifying monthly income.

For example, if you have $1,000,000 in cash and $750,000 in retirement, you’d have a total of $1,525,000 ($1m + $525k).

We then divide $1,525,000 by 360 and come up with around $4,250 per month in income. As you can see, a very asset-rich borrower can’t get very far using this method.

However, the lender may be able to add other income such as Social Security, pension, etc. to stretch the numbers a bit further, or use a shorter term, such as 180 months if it’s a 15-year fixed.

This type of loan might be well-suited for a retired high-net worth individual.

Employment and Credit Still Verified on a Stated Loan

- Even if stated income is permitted to qualify

- You’ll probably still need to verify your employment

- And document your assets (bank statements, retirement accounts, etc.)

- Your credit report will also be pulled to ensure you pay your bills on time

In some of the cases above, the bank or lender will verify your employment by calling your employer, or request a CPA letter or business license if you are self-employed.

If you’re retired, they obviously won’t, but they’ll still want to verify any retirement income you take in.

This is important because your job title will determine what you can reasonably state in the way of gross monthly income.

If you’re a doctor, it’d be normal to state that you make $50,000 a month. But if you’re a kindergarten teacher, underwriters won’t believe that you’re making $10,000 a month.

It’s just not likely, nor does it make sense for the position. And for this reason, many loans that “overstate” income will subsequently be declined.

It’s actually quite common to see a mortgage declined on the basis that the income does not match the job title/description, or seems too high for the related position.

And if you’re curious where underwriters determine how much a certain occupation should earn, check out Salary.com. That’s where many are instructed to pull the numbers to see if it adds up.

Another “setback” to a stated income loan is that a bank or lender can ask that you fill out an IRS Form 4506-T, which basically authorizes the lender to request your tax returns from the IRS for the previous two years.

Although it’s not common for them to actually look up your returns, it can be enough to deter a would-be “liar” from overstating their income.

It’s most common for a lender to pull a 4506 only if you become delinquent on the loan in a short period of time.

But if they do pull a 4506 and find that you indeed overstated income, you could be face some steep consequences, so take caution.

Additionally, a mortgage lender will still pull your credit report to determine if you’re a sound borrower.

Since they’re taking more risk by extending financing without verified income, they have to pay close attention to what they can verify.

If you are seeking a stated income mortgage, it’s imperative that you have good credit to obtain a favorable mortgage rate.

Sure, you might be able to get approved with a 620 score, but you’ll pay more as a result.

Stated Income Mortgage Rates Are Higher

- If you choose to state your income as opposed to verifying it

- Expect a higher mortgage interest rate, all else being equal

- And a lower max LTV (or higher minimum down payment)

- To account for increased risk of the unknown…

If you do choose to state your income, you must pay a premium because you’re putting more uncertainty and risk in the hands of the lender and subsequent buyer of the loan if sold on the secondary market.

For this reason, mortgage interest rates on stated income loans are often .25% to .50% higher than a full doc loan.

Of course, it depends on all the loan details. It might be possible for someone to state their income and get a lower rate than someone going full doc if they have better credit, and/or a larger down payment.

Conversely, someone with poor credit requesting a reduced doc loan might get a mortgage rate several percentage points higher than the typical, going rate. It can get expensive fast.

Related to that, you may also find that you’ll have to put down a larger down payment or sport a higher credit score to obtain the financing you need when going the stated or asset-verification route.

Again, this becomes an issue of layered risk, and because you chose to state your income, the lender may limit risk in other departments such as credit and down payment.

In closing, after some years of intense credit tightening, there are now plenty of options for those who may have trouble qualifying for a mortgage using traditional income.

However, you’ll often pay the price for this convenience in the form of a higher mortgage rate and/or be forced to come to the table with a larger down payment, more reserves, and more scrutiny. So be prepared.

- Are Mortgage Rates Finally Poised to Start Falling Again? - June 25, 2026

- Mortgage Rates Are Having a Good Day as Oil Prices Fall to Pre-War Levels - June 24, 2026

- You Can Still Get a Sub-6% Mortgage Rate, But Is It Worth It? - June 23, 2026

What lenders are offering SIVA loans? Tennessee

Michael,

Look into non-QM loans, many of which allow for stated income.

what is a non-QM loan.

Roy,

A loan that doesn’t fit the Qualified Mortgage standard, one such rule being a max DTI ratio of 43%.

Are stated income loans available on Conforming loans? I am anticipating a loan amount 350.000-400,000.

Kathy,

Possibly, you might want to look for a non-QM loan, which is kind of the new stated income standard.

Are stated income loans available in Texas, if so, please refer a company to me.

Thanks.

Kim,

You may want to search for a non-QM lender in Texas.

I have several income properties I’d like to refinance, for a variety of reasons. Can you tell me if a stated income non-QM mortgage would work for me? I’m in Idaho (so are the properties.). Thanks!

Erin,

There might be a program suited for you…I can’t say with certainty, probably best to do some research on non-QM lenders that lend in Idaho.

Hi, I am a real estate broker & had switched professions because I had stopped making money doing real estate but now I would like to get back in business (I’ve kept my real estate license). Do you know names of banks in the secondary mortgage market that work through brokers, especially those that do SIVA/SISA loans. None of the other brokers want to share this info & I’ve been gone from this business for few years now. I’ll greatly appreciate your help, you can email me. Thanks in advance.

Norma,

You’d be looking at non-QM lenders nowadays…track those down and you’ll find your stated income stuff.

Can equity be used in a refinance as a down payment?

Sean,

People have been known to use equity from one home to use toward down payment on another.

Colin,

Looking for 150K-165K. I own my house- no present mortgage. House was recently assessed at 1.38 Million. Live in New Jersey. Recently lost my job. My wife and I have a combined income of between 80-90k/year. Other the 12k from SS the remaining income is part time, Ebay selling and hard to doc. I had very good credit – until I applied to 2-3 National Banks for a mortgage. Thoughts? Any companies I could speak with?

sg

SG,

May want to look into asset depletion if income is light, national banks probably not the most informed about programs like that.

Can you please explain? Could use some help. Very frustrated.

SG,

Research asset depletion…there’s also a chance your wife could apply on her own if she has stable job/income seeing that the loan amount doesn’t seem to be very high. A broker might be helpful to explore the many routes you can take here.

I have a 740 credit score just went into escrow I am trying to buy the house with a 90% stated income loan My gross income for my business I am self employed is $234000 but I take every legal write off I can so my net is low on my tax forms the sales price is $420,000 riverside county ca.I will have $88,000 in the bank when the deal closes but I dont want to put any more money into the deal because I am 69 years old and I feel like I need the security of the cash in bank know of any one who will loan me

Hi Colin,

I am looking for a stated income loan for a home I’d like to purchase.

I have my own business and can provide corporate and personal bank statements. The loan amount is no more than $750,000 and I would be providing 40-50% downpayment. Do these loans exist with decent rates and amortized over 30 years? If so, do you have any recommendations of companies I could reach out to?

Thanks

Angie,

With that size of a down payment you should have options…might have to find a portfolio lender or go non-QM route. Do some digging to see what your available options are.

I am looking for stated income refinance 900,000 please let me what is the best way to go.thanks

Artoush,

You’ll likely need to use a specialty lender that offers portfolio loans or non-qm options.

The article references complicated tax returns. This is misleading as the Borrower is not going to be the one analyzing the returns, it will be the lender. I am in mortgage banking for the last 33 years and I will always fight on the side of not offering the no income verification option on ANY loan regardless of who the investor may be. This is how the foreclosures started to begin with, stretching the rules. If you can’t PROVE your income, you don’t NEED a loan.

Robin,

Write off is something banks and all kinds of business in this country was allowed to file for the tax return. While banks and their CEOs’ are happy with large tax cut in their tax payments, why don’t they approve the mortgage loans for the self-employed with their legitimate tax’s write off?

Hi..I’m trying to qualify for 170,000 with an income of 40,000 and student loans of 80,000. Hubbs has no w2 but an income of about 30,000. What do you suggest..we both have about 600-630 credit score

Carla,

If you actually document income, it will depend on how the student loan payment is listed on your credit report as it can take a big bite out of your income. If you go stated there might be more flexibility. Your credit scores are also quite low and it might make sense to work on them before applying for a mortgage in order to access more loan programs and get a lower mortgage rate.

Tim,

The banks do allow many write offs to be added back in to a self-employed borrower’s income. I do it every day of the week. But not all of what the borrower wants to write off can be added back. The problem is that the self-employed borrower wants to cut that bottom line as much as possible to avoid paying taxes. Actually everyone, not just the self-employed. But what happens is that the bottom line doesn’t add up when going to buy a house. Only so much paper write off can be added back to income. My gripe is not with a self-employed borrower – but with a borrower who cannot show sufficient income and still thinks they should get a loan. You cannot have it both ways – show as little income to government as possible and still expect to get financing without being able to prove your income from your returns. It’s a catch 22 that no one gets explained to them when being self-employed and looking for a house.

Hi and I understand your angst though I am one of those small business owners who fall into this category. I am just now researching on alternative lending as a result. Since 2010, my income range had been from $85k to $115k but in DEC 2012 I went from full time employment with an additional small business to strictly small business. Now, unfortunately when seeking a mortgage to relocate my bottom line on tax returns implies my income is quite low due to me re-investing profit back into my company. So although I only seek $80k on a $200k home, with a credit score of 740 and no debts – my tax returns are still like a condemnations- so now I’m faced with just getting a little hut and paying cash. There has got to be another way. I sacrificed to earn a phd but now I have to live in a rehab site or rent.

Tatia,

I feel your pain. My husband and I are in the same boat. Stated income has worked for us we’re able to get rates better than hard money but significantly higher than the conventional mortgage rates that we once enjoy. Seems the best going to do is accumulate cash to purchase or pay the piper one tax year preceding your purchase. We’re in the rental income properties business and are always looking to make additional purchases so it’s not easy.

I’m a highway contract carrier. We do write off as much as possible , however all we spend is almost all related

To our jobs , which can be normal expenses.

I personally had some life experiences which interfered with my taxes which is in the process of being corrected , however I have paid 1500-2000 a month plus all utilities in rent for many years. Clearly I can make the mortgage payment. I think this should be the focus. Can the consumer make the payment.

Robin, you are absolutely correct about the type of borrower that this loan appeals to. Too often marginal buyers would hear the mortgage rep say they need to have income of “X” amount, and miraculous, that was what their stated income became! I sold real estate for 28 yrs including 2001 – 2008. Each office meeting we talked about when the bubble would burst because the home prices were artificially increasing under supply vs demand. But too many of those buyers were marginal at best and doomed to fail from the outset.

oh, my. time to update this to the crazy world of 2021. I’m trying to “just simply” get info on SIVA loans and everywhere I turn I’m supposed to already have a house in mind, the location, how much it is, the loan amount in mind… how would I know that? Isn’t that what the broker is supposed to tell me? I just want to find out if the loan is even offered. All online, all third party, all wanting to capture information before the fact … virtually impossible. Then, relentless follow up selling and selling of captured info to other parties. Exhausting.

I’m working with a broker on a refinance of 254,000.

He’s all over the place with closing cost estimates, 2%,

(5300.00) brokers fee plus 5600.00 standard closing costs.

Now I received a loan estimate from xxxx lending for 24,874.00. Is this for real? I’M SPEECHLESS.

The rate is 4.95%.

Leopoldine,

It depends on the loan’s attributes, as stated income loans are typically much more expensive. Also, rates have risen recently so if the loan wasn’t locked that same rate may cost a lot more in the way of discount points paid by the borower. Ultimately, you need to break down the costs on the LE to see where it’s all going. Does it include points, property taxes, and other escrow items? If it’s all commission that might be a different story.

I have a 47-acre residential property with a 1,440 square foot home on it in eastern Merced Co, CA. There is also a near-400 square foot shop. My water well is capable of pumping over 200 gallons of minute; the water is so pure I could bottle and sell it. I put in a huge septic system and all the utilities are underground. There is over 1/2 mile of county road frontage. Houses are all around on adjacent land and otherwise, and recreational lakes are a few miles east of me, as is Yosemite, which is 70 miles to the east. The property is in the Merced River corridor, but not in a flood zone. I need $400,000 to pay off $230,000 short term first and second loans, and I want About $150,000 plus to go back into business there, gathering, sorting packing and selling cobble rock off of 15 of my acres. I have been in the business there before and can take in $10,000- $20,000 a month from cobble rock sales.