The housing market has been stubbornly frustrating for prospective home buyers.

Not only have mortgage rates doubled over the past year, but home prices remain highly elevated, despite some minor improvements.

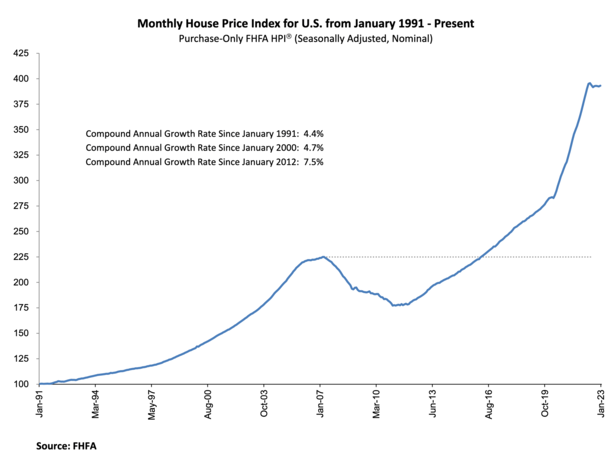

Sure, you might hear that the housing market is crashing, or that we’re in a home price correction.

But that doesn’t mean a whole lot when you zoom out and look at home prices over the past couple years.

What’s worse is despite abysmal affordability, home prices may not even come down.

Home Prices Are Up 5.3% From a Year Ago

While there have been declines in certain overheated metros nationwide, home prices are up 5.3% nationwide from January 2022 to January 2023.

This is according to the latest Federal Housing Finance Agency (FHFA) seasonally adjusted monthly House Price Index (HPI).

And they rose 0.2% in January from a month earlier after registering a 0.1% monthly price decline in December 2022.

If we drill in a bit more, looking at the nine census divisions, seasonally adjusted monthly home prices from December 2022 to January 2023 showed a wider range.

Home prices were off 0.6% in the Pacific division and up 2.0% in the New England division.

On a 12-month basis, prices were -1.5% in the Pacific division and +9.6% in the South Atlantic division.

As I always say, real estate is local, and this is especially true these days with some markets in different stages than others.

But just look at the national home price chart above. Home prices have absolutely surged over the past few years.

And they pulled back by a tiny amount before flattening out. The takeaway is that home prices are high and might not come down much.

Home Prices Haven’t Fallen Much Because Inventory Remains Tight

Despite frothy home prices and questionable, speculative buying from investors, home prices have held up pretty well.

If you’re looking at that home price chart and wondering how on earth prices can be well above levels seen in 2006-2008, blame inventory.

There’s been a serious lack of homes for sale for many years now, exacerbated by the mortgage rate lock-in effect.

In short, many of today’s homeowners have 30-year fixed-rate mortgages that are priced between 2-4%.

Also referred to golden handcuffs (assuming they want to sell/move), these low rates make it very difficult to part with the property.

Even if they are able to afford a subsequent home purchase, they might be turned off by the new interest rate set at 6%.

This explains why the inventory of unsold existing homes was a mere 980,000 at the end of February, per the National Association of Realtors.

That’s just 2.6 months’ supply at the current monthly sales pace. And as we know from supply and demand, when supply is low and demand is high, the price goes up.

For the record, the median existing-home price fell 0.2% in February to $363,000, ending 131 consecutive months of year-over-year increases, the longest in history.

So there is some downward pressure on home prices, but 0.2%? That’s not going to do much is it?

How Much Income Is Required to Buy a Home Today?

The rule of thumb for housing costs is about 28% of your gross income. So if you make $80,000, no more than $1,867 can go toward the mortgage.

That includes principal and interest, property taxes, homeowners insurance, and PMI and HOA dues if applicable.

The problem is the average United States home value is $327,514, per Zillow, and is up 6.8% over the past year.

The real median household income in the U.S. was $70,784 in 2021, and actually declined since 2019 due to inflation.

If we consider a $325,000 home purchase with a 20% down payment we arrive at a $260,000 loan amount.

We’ll throw a 6% mortgage rate to arrive at a P&I payment of $1,558.83. Now let’s add taxes of $340 per month and homeowners insurance of $100 per month.

That takes us to roughly $2,000 per month, or about 34% of that $70,784 median income.

It’s not horrible, but it’s still above the 28% rule of thumb for a housing payment. And that’s using favorable math.

If it’s a 5% or 10% down payment, you’ll have PMI, a higher mortgage rate, and a larger loan amount to contend with.

So it’s pretty clear that home prices are unaffordable for most at their current levels. But without a meaningful addition of inventory, things won’t change.

And as noted, many existing owners aren’t going anywhere. The only game in town is newly-built homes, but builders can only build so much.

Additionally, new builds often aren’t located in densely-populated areas where there is a greater need for new, affordable housing.

In California, just 21% of all residents earned the minimum income needed to purchase an $822,320 median-priced home in 2022, down from 27% in 2021, per CAR.

It was slightly better nationwide, with 43% able to afford a median $392,800 property.

What Happens Next for Home Prices?

Black Knight noted that home prices rose 0.16% in February after seven consecutive monthly declines.

It was the strongest single-month gain since May 2022, though at 1.94%, annual home price growth dipped below 2% for the first time since 2012.

This supports the thesis that home price growth was going to slow, aka lower year-over-year home price gains.

But that actual, falling home prices would still be hard to come by. And now that we’re entering the spring home buying season, home prices could actually re-accelerate.

Mortgage rates just happen to be falling too, with the 30-year back to its February low of around 6.125%.

Rates were about 1% higher in early March, so there might be some serious tailwinds for the housing market, at least in terms of home price trajectory.

Sadly, this means it’s going to remain difficult to purchase a home with median income. And that even though home prices are overpriced, they may remain that way for the foreseeable future.

Ultimately, we could face years of relatively flat home price growth, which would still put homeownership out of reach for many.

Of course, there are affordability solutions coming to market, whether it’s the California Dream For All loan, or temporary rate buydowns.

For those hoping for or expecting a housing crash, you’ve got to look at the fundamentals. It’s not 2008 even though home prices are significantly higher.

The mortgages are much different and housing supply is a lot lower. Until that changes it’d be hard to draw too many parallels.

Read more: What will cause the next housing crash?

- Mortgage Rates Could Drop as Much as Half a Percent with Basel Re-Proposal - June 30, 2026

- Mortgage Rates Face Big Week of Jobs Data - June 29, 2026

- Are Mortgage Rates Finally Poised to Start Falling Again? - June 25, 2026

The last housing “crash” was more like a slight downdraft. A drop of about 10% in price at “worst”. Then right back to the regularly scheduled climb-out like a jet plane on steroids. Meanwhile wages never budge upward. Want to fix the housing affordability crisis? Easy. The government needs to go on an absolute rampage of building condos, enough to add supply so 2 bedroom condos cost $100,000 in the rest of the market.

Nothing short of this will do any good toward the crisis. To buy these condos, the household income needed would be WAY more attainable than the current case. A household income of a measly $50,000/year would suffice – assuming they could ever get the loan, a new can of worms. After all, people who aren’t made out of money usually don’t have awesome credit scores – or use credit in the first place. A good question is why gross not take-home income is used in the calculation. This makes no sense, because people need money to live on including paying the “mortgage” on the car! ARM mortgages aka neutron bomb loans should be illegal because they are designed to blow up in the homeowner’s face when time’s up.