A new report from Zillow revealed that home prices need to come down by about 25% to become affordable again.

But chances are they won’t, despite a lot of sensationalist media calling for a housing crash.

At the end of the day, home prices have gotten inflated, but limited supply and homeowner lock-in effect, combined with mostly healthy mortgages should limit downside movement.

Additionally, if and when mortgage rates do come back down to more reasonable levels, affordability can also improve.

So a combination of factors could rebalance the housing market without an outright crash.

Typical Home Purchase Now Requires 30% of Household Income

Per Zillow, it now requires 30.2% of income to afford a mortgage on a typical U.S. home, which they say is “well above the norm.”

That’s also beyond the 30% threshold for a household to be considered “cost burdened,” and significantly higher than the 22.8% average seen from 2005–2021.

While high home prices are partially to blame, the real tipping point of late has been mortgage rates, which have increased about 400 basis points since the start of 2022.

Yes, a 30-year fixed mortgage is pricing around 7.25% today versus 3.25% back in January, as crazy as that appears.

Zillow adds that the typical monthly mortgage payment is now about $1,850, up 75.5% (or $800) from a year ago.

On more expensive properties throughout the nation, we’re talking thousands more per month to pay the mortgage.

This has shocked prospective home buyers, a move somewhat engineered by the Fed to cool the overheated housing market.

As I’ve mentioned before, the Fed manipulated mortgage rates for several years via their Quantitative Easing (QE) program that included hundreds of billions in purchases of mortgage-backed securities (MBS).

But they have since ended that program, began Quantitative Tightening (QT), and raised their fed funds rate several times.

So it appears they’ve been successful at both lowering and raising mortgage rates, though the Fed typically isn’t so involved in mortgage rate movement.

Zillow Expects Home Prices to Be Flat Over the Next 12 Months

While home prices might need to fall substantially to boost affordability, don’t count on it.

Zillow itself forecasts flat home values through the end of this year, and a small increase of 1.3% for the 12 months ending September 2023.

Take that housing crash folks. Of course, a gain of 1.3% would mark a major deceleration from what has been double-digit annual gains in home prices.

But my assumption is most would be happy with flat home prices over the next year.

The reason home prices aren’t under as much pressure as you’d think is because inventory remains very scarce, at roughly 40% below pre-pandemic levels.

At the same time, most existing homeowners have 30-year fixed-rate mortgages in the 2-4% range and significant home equity.

That further strains inventory, making it difficult for home prices to drop too much.

And if mortgage rates come down next year as inflation concerns wane, affordability could get a boost without a drop in home prices.

This supports the idea to buy a home before mortgage rates come back down.

Remember That Home Prices Are Local and Will Vary by Market

As it stands, the average home is worth about $358,283, and median household income is $71,895.

This makes the monthly principal and interest on a 30-year fixed-rate mortgage (assuming a 20% down payment) unaffordable.

But not all housing markets are in the same position, with some more overvalued than others, by quite a large margin.

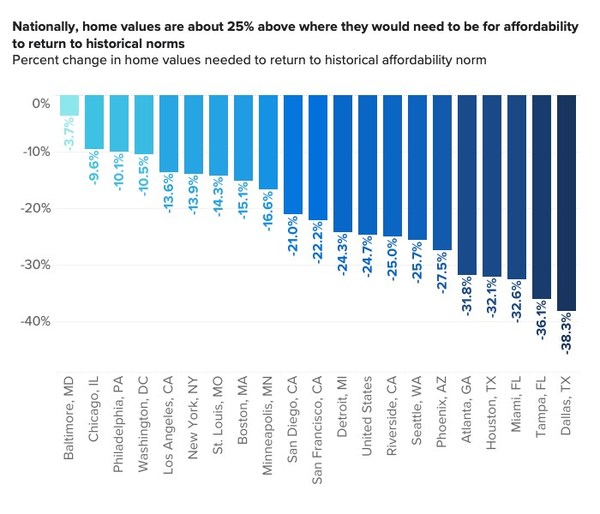

For example, home prices are only 3.7% overvalued in the Baltimore, Maryland metro in terms of historic affordability norms.

They’re also only about 10% overvalued in Chicago, Philadelphia, and Washington, D.C.

Conversely, cities like Dallas, Las Vegas, Nashville, and Salt Lake City are far away from their historical norms, and need declines of at least 37% to get back to affordable levels.

These are place that saw a huge influx of buyers recently, driving prices up faster than other areas of the country.

The same is true in places like Phoenix, Atlanta, Houston, Miami, and Tampa, where home prices got way ahead of themselves.

These metros could see more sizable home price declines if mortgage rates continue to climb, or fail to come back down to more reasonable levels.

This means it’s now more important than ever to know your local housing market if you’re a buyer or a seller.

Forgot about what home prices are doing nationally and focus on your own market. Either way, don’t expect a full-blown buyer’s market due to ongoing supply constraints.

Read more: The Truth About Falling Home Prices

- Mortgage Rates Catch a Break as Job Growth Goes Negative - August 7, 2026

- Mortgage Rates Move Higher on Jobs Report Defense - August 6, 2026

- Mortgage Rates Are Now Higher Than They Were a Year Ago - August 5, 2026