It’s no secret that homes just aren’t as affordable as they used to be.

An unwelcome combination of significantly higher mortgage rates coupled with ever-higher asking prices has put a major dent in affordability.

In May, the monthly mortgage payment on a median-priced home ($401,100) was over $2,000, up from around $1,000 back in 2020, according to the National Association of Realtors.

And that assumes a 20% down payment, something that just isn’t a reality for many home buyers these days.

The good news is there are lots of creative financing options out there, whether it’s from a state housing agency or even a national lender.

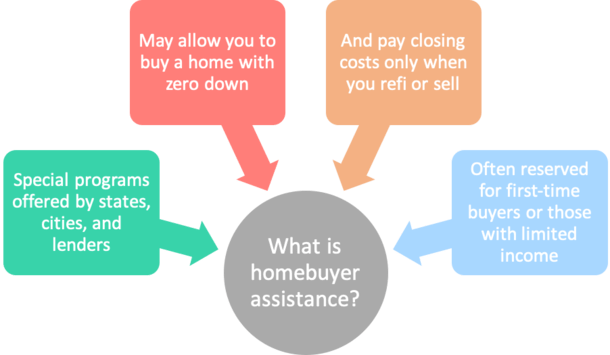

What Is Homebuyer Assistance?

In short, homebuyer assistance is a special program or series of programs offered by a local municipality, state, or private lender that reduces borrowing costs and promotes homeownership.

This can come via down payment assistance, closing cost assistance, reduced interest rates and mortgage insurance premiums, or a combination of these and other programs.

Collectively, it makes homeownership more attainable, especially for first-time home buyers and/or those with low-to-moderate income.

As noted, there are countless homebuyer assistance programs available, many of which are offered at the state or municipality level.

For example, the California Housing Finance Agency, or CalHFA for short, offers a series of homebuyer assistance programs.

The same goes for every other state in the nation. Programs are also offered for certain cities or underserved areas throughout the nation.

At the city level, one example is LA’s Home Ownership Program (HOP) loan, which provides a second mortgage for first-time home buyers up to $85,000, or 20% of the purchase price (whichever is less).

Beyond that, there are also homebuyer assistance programs offered by individual mortgage lenders, banks, and credit unions.

Private companies often have affordable housing goals and initiatives, which are sometimes geared at specific areas or priorities like increasing minority homeownership.

These offerings include both government options (FHA loans, USDA loans, VA loans) and conventional options (Fannie Mae and Freddie Mac).

Homebuyer Assistance Program Examples

The CalHFA has been around since 1975, with a stated goal of helping low- and moderate-income renters and home buyers via down payment and closing cost assistance.

It’s important to note that they aren’t a lender, but rather offer their products through private loan officers who have been trained and approved to originate them.

It may also be possible to work with an independent mortgage broker who is approved to work with a CalHFA-approved wholesale lender.

Anyway, to give you an idea of what they offer, let’s look at their CalHFA Conventional loan, which is a Fannie Mae HFA Preferred first mortgage.

This means the loan isn’t subject to costly loan-level price adjustments (LLPAs), and reduced mortgage insurance coverage is offered to those with limited incomes.

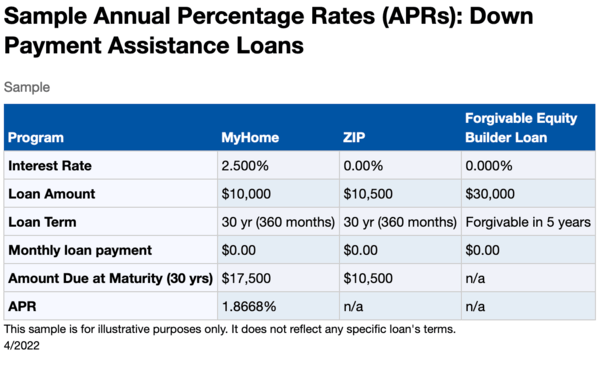

But wait, there’s more. This loan may be combined with the MyHome Assistance Program, which is a deferred-payment junior loan (second mortgage) that can be used to cover down payment and/or closing costs.

As you can see in the table above, which is just a sample, the monthly payment is deferred ($0) until the loan is refinanced, paid off, or the home sold.

But interest does accrue on the balance over time if you don’t pay it off.

There’s also the CalPLUS Conventional Loan Program, which combines a conventional 30-year fixed first mortgage with the CalHFA Zero Interest Program (ZIP) for closing costs.

That ZIP loan is both deferred and interest-free, meaning no payments or interest, as seen in the table.

Your closing costs can effectively be set aside until you refinance or pay off your loan, or sell your home.

You can actually combine all three programs if needed to get a more affordable first mortgage, a second mortgage for the down payment, and a third mortgage for the closing costs.

Aside from these standard offerings, the agency also launched the “Dream For All Shared Appreciation Loan” earlier this year.

As the name suggests, borrowers share future appreciation in lieu of a down payment.

Regarding the LA City homeownership program known as HOP, you get a 0% interest loan with a deferred payment.

And repayment is required if the home is sold, if there’s a title transfer, or the home is no longer owner-occupied.

You must be a first-time home buyer, income limits apply, and the property must be in an eligible area.

Tip: If you work with a housing agency, inquire about a mortgage credit certificate before you apply to potentially save money on taxes.

Homebuyer Assistance Via Private Banks and Mortgage Lenders

To give you an idea of a private offering, there is the recently launched U.S. Bank Access Home Loan.

It comes with up to $12,500 in down payment assistance and a lender credit up to $5,000.

Then there’s the Guild Mortgage 1% Down Payment Advantage, which combines a 2% non-repayable grant offered by the company and a 1% temporary buydown in year one.

Speaking of grants, some may be fully forgivable, while others might be required to be paid back when you refinance or sell.

Be sure to pay attention to details like that when researching potential down payment assistance or homebuyer assistance programs.

One such example is Movement Boost from Movement Mortgage, which is a zero down FHA loan that features a repayable second mortgage.

Despite having to be paid back, it eliminates the roadblock of needing cash at closing, and instead spreads it out slowly over a 10-year loan term.

Then there’s Rocket Mortgage ONE+, which offers a 2% grant from the Detroit-based lender and private mortgage insurance at no cost.

I could go on and on, but you should get the idea. There are lots of grants, credits, special purpose credit programs (SPCPs), and other specials out there.

But it’s up to you to do some digging to find them. So when you’re shopping around for the lowest rate, also inquire about homebuyer assistance if you want/need it.

Update: On March 25th, 2025, FHFA director Bill Pulte terminated the special purpose credit programs (SPCPs) supported by Fannie Mae and Freddie Mac.

Who Qualifies for Homebuyer Assistance?

- Typically need to be a first-time home buyer (but not always)

- Area income limits often apply to those receiving assistance

- May also need to purchase a property in a specific location/city

- Property must be owner-occupied and usually only 1-unit is permitted

- Still must qualify for a mortgage (e.g. min. FICO score and max DTI ratio)

While it might sound pretty good to buy a home with little or nothing down (and sans closing costs), not everyone will qualify.

Many of these programs are geared toward first-time home buyers, generally defined as someone who hasn’t had ownership interest in the past three years.

This means those who have never owned a home, or an individual who sold their former home three or more years ago and hasn’t owned since.

Depending on the program, you may be required to complete homebuyer education and counseling. While it might seem like a pain, you may actually learn something valuable along the way.

Beyond that, income limits often apply as well, typically based on the state agency’s limits or area median income (AMI) limits.

You can look up income limits via Fannie Mae’s website to see where they stand in your desired purchasing area.

Speaking of income, non-occupant co-borrowers or co-signers are typically not permitted.

There are also loan limits to worry about, which are usually based on the conforming loan limit, but sometimes even lower.

And in most cases, the property is going to need to be your primary residence, aka the one you occupy full time.

Homebuyer assistance programs are geared toward those in need, not investors or second home buyers.

To that end, 2-4 unit properties are generally not permitted, though condos/townhomes, and manufactured housing are.

Lastly, you will still be subject to a minimum credit score requirement and a maximum debt-to-income (DTI) ratio.

So you’ll still need to qualify for a mortgage like you would any other type of loan, though there may be more flexibility via state housing agencies.

In closing, if you’re not sure homeownership is in reach, take a moment to research the many homebuyer assistance programs out there. You might be surprised at what you come across.

- Mortgage Rates Catch a Break as Job Growth Goes Negative - August 7, 2026

- Mortgage Rates Move Higher on Jobs Report Defense - August 6, 2026

- Mortgage Rates Are Now Higher Than They Were a Year Ago - August 5, 2026