Sometimes I’m surprised I miss the most basic of mortgage definitions, seeing that this blog has been around for more than a decade, but alas, I’ve never written about occupancy specifically.

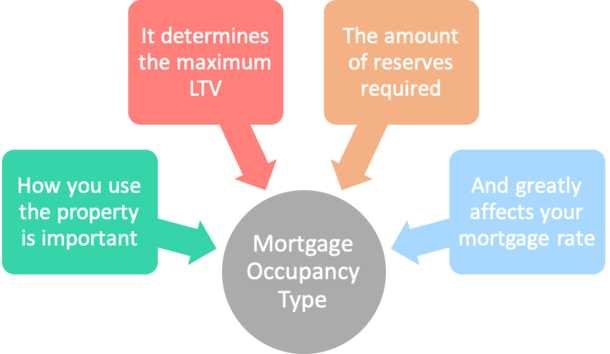

So without further ado, let’s talk about the three main types of occupancy with regard to qualifying for a mortgage because they’re pretty important.

Mortgage Occupancy Type

Primary Residence (Where you live)

- This is the property you live in all or most of the year

- Underwriting guidelines are easiest for this property type

- And mortgage rates are the lowest

This is your standard owner-occupied property, a home or condo you plan to live in full time. Or at least the majority of the time. It may also be referred to as your principal residence.

It can be a single-unit property or a multi-unit property, but you must live in it most of the year.

The property should also be reasonably close to where you work, if applicable, and you must sign a form that says you plan to occupy said property shortly after closing.

Now the good news. Since it’s your primary residence, mortgage rates are the lowest, and it’s also easier to get a mortgage because guidelines are more flexible. This means you can potentially put less down or refinance at a higher loan-to-value (LTV).

We’re talking a 3% down payment mortgage, which is pretty much the lowest down payment you can get away with unless the lender has a zero down program, which again would likely only work on a primary residence.

Additionally, you can get all types of different loans, from an FHA loan to a VA loan to a USDA loan. There are few restrictions because it’s a property you intend to occupy.

For this reason, unscrupulous borrowers will sometimes try to fudge the occupancy and say they live in the property, even if they don’t intend to. This is not a matter to be taken lightly as it constitutes fraud.

If you’re a real estate investor, or simply own more than one property, it’s imperative that your bank statements and other important documents are mailed to your primary residence each month.

If you claim one house to be your owner-occupied property, but your bank statements and other financial materials are currently going to another one of your properties, it’s a red flag.

The mortgage underwriter will surely question the occupancy, and your mortgage application will very likely be declined.

Here’s a common scenario. A borrower submits a home loan application for the subject property as their primary residence.

When conditioned to provide verification of assets, they use bank statements from another property they own and the file gets declined for occupancy fraud.

In the eyes of the bank/mortgage lender and the investor, it doesn’t make sense for a borrower to send bank statements, cable bills, and other financial statements to a property they don’t occupy for the sheer reason it wouldn’t make sense if you didn’t live there.

Banks and lenders will likely decline a file if it’s listed as owner-occupied, or at best they’ll counter the borrower to re-submit the loan as an investment property.

Anyway, if the property in question will be the home or condo you plan to reside in, it is considered your primary residence.

Second Home (Where you vacation)

- A second home is another way of saying vacation home

- Not necessarily that you own two homes

- Should be in a vacation area far from your primary residence

- Can only be a single-unit property and mortgage rates can be slightly higher

Then we have the second home, which as the name implies, is secondary to your primary residence.

In a nutshell, this means you already have another home you live in full-time, or most of the year, along with this secondary property, which is often referred to as a vacation property.

Think your cabin by the lake, or your ski chalet up in the mountains. Or perhaps your beach house, if you happen to be so lucky.

Distance is a factor here by the way, as is location. Lenders generally want it to be at least 50-100 miles away from your primary home, though exceptions are allowed if it makes sense.

For example, if you live inland and have a beach house 30 miles away.

It should also be a single-unit property, for obvious reasons. And you should occupy it for some portion of the year.

Put simply, it has to make sense as a second home, otherwise the lender may think you’re going to rent it out.

Because the property isn’t your primary, there will likely be a pricing adjustment for occupancy. This has to do with risk.

In the event of financial distress, a borrower is more likely to stop paying on their second home as opposed to their primary. This means mortgage rates must be higher to compensate.

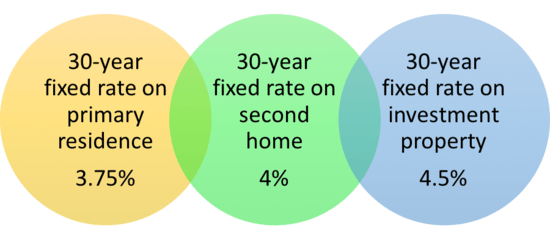

Expect a rate that is higher, all else being equal. How much higher depends on all the loan attributes, but maybe .125% to a .25% higher than a comparable loan on a primary.

Altogether, not too bad. The illustration above might give you a sense of what to expect.

Also note that there will be LTV restrictions as well, meaning you’ll need a larger down payment for the purchase of a second home, or more equity if refinancing the mortgage. Chances are you’ll need 10% down, or a max LTV of 90%.

You may also find that mortgage credit score requirements will rise, so you might need a minimum credit score of 680 instead of 620.

Note: Most underwriting guidelines allow you to rent out a second home for a portion of the year as long as you ALSO occupy it during the year. But it can’t be subject to an agreement that requires the property to be rented.

Additionally, you won’t be able to use any rental income from the property to qualify for a home loan.

Investment Property (The one you rent out)

- This is a rental property

- Can be condo or home, single-unit or multi-unit

- Typically requires a large down payment

- And mortgage rates can be much higher to account for risk

Finally, we have the investment property, which again as the name makes abundantly clear, is a property you plan to hold as an investment of some kind.

This generally means it will be rented out, and that it will generate income. This type of occupancy comes with the most restrictions because someone else other than the borrower will be living in the property.

Additionally, the borrower will be a landlord, which isn’t as easy as it might sound. That all equates to more risk, which results in more LTV restriction and higher mortgage rates.

You might be looking at a max LTV of 85%, meaning a minimum 15% down payment. This can get more restrictive if it’s a 2-4 unit property. If you want cash out, expect an even lower max LTV.

Also expect higher asset reserve requirements and higher minimum credit scores.

As far as rates go, it could be .50% to 1% higher than a similar loan on a primary residence, depending on all the loan details. It can get really pricey if the LTV is high and it’s a 4-unit property, for example.

In other words, it’ll be harder to qualify and you’ll have to pay more to finance your non-owner occupied property.

The takeaway here is that it’s easiest (and cheapest) to finance a primary residence, followed by a second home, and then finally an investment property.

Each has different rules and guidelines that borrowers must adhere to if they want to qualify for a mortgage. Knowing this beforehand is important to avoid any unwanted surprises.

- Can You Get a 4% Mortgage Rate Still? - August 10, 2026

- Mortgage Rates Catch a Break as Job Growth Goes Negative - August 7, 2026

- Mortgage Rates Move Higher on Jobs Report Defense - August 6, 2026

The rates with me for primary versus 2nd home are the same

don’t know who charges more

Warren,

Sometimes they’re the same, sometimes they’re not. Certain scenarios with some banks, not all, may charge for second home occupancy.

Hello Colin,

Thanks for the article and overall website dedicated solely on explaining mortgages.

Q) I have my first property but it is not my primary resident. ie., renting now. In this case, what happens when i buy another property which will be my primary resident. Will that count as second home or primary home?

master tez

It’s not about what you have first or second or third, it’s about occupancy. So the one you actually live in would be primary, regardless of when it was purchased. A second home can refer to a second property that is a vacation home or a rental property, but in either case wouldn’t be where you primarily live throughout the year.

Thank you for taking time to answer my question.

I can not afford to purchase a property in the area I currently work. I would like to purchase a property out of the area, and would commute on my days off (4 day work week / 3 day weekend) I would reside with a friend during the week. Would this situation qualify me for primary residence mortgage loan?

CP,

As long as it makes sense to the underwriter (to drive that far, etc.) and you don’t rent out the property or own another one that you occupy, it shouldn’t be an issue because in that scenario it would still be your primary, owner-occupied home.

Hi Warren

I have a business address in a city where my clients are and I spend time there with my sister. My office is in her home. My principal residence is 30 miles away and I spend 3 days there a week. I rented 2 rooms to my daughter because she insisted on it. Can I have her renting from me and me living in the same house as my primary residence. Will lenders look at this as a rental or primary residence.

Hello,

Say a borrower gets a mortgage for a home and claims it as a primary residence but ends up renting it out years later… Is there a way to switch it to an investment property? is there any way the lender could figure out that the owner is no longer living there? I assume if the bills are getting paid they probably don’t ever look into it?…

Thanks in advance! this thread has been very informative and helpful!

Kevin,

It sounds like in your scenario, the borrower purchased the property as their primary residence, and eventually rented it out, so it wasn’t disingenuous. Typically, you only need to occupy it for 12 months before renting it out. The problem is when people lie and say it’ll be their primary home but never actually move in, and instead rent it out immediately to get favorable financing and a lower mortgage rate. Post closing audits and/or occupancy reports can be used to discover potential occupancy fraud. They can see if bills are in the borrower’s name, check their other real estate holdings, etc. to see if it makes sense they occupy the property.

Good Day,

If a property was bought with intention to move in as primary residence, but the person is not able to move in (we are military family and move to new home is going to be delayed due to corona). Is there a way to change to second home mortgage so we don’t get into trouble for not being able to move in and sell our current home. We have every intention of moving in as soon as possible but may be delayed.

Shannon,

There might not be a need to change occupancy type if it’s your intention to move in and extenuating circumstances outside your control are delaying that. You might just want to have proof that’s the case.

I purchased a joint tenancy home with my grandson because he couldn’t qualify for the loan. He has lived there entire time, 5 yrs this next Oct. 2020. We took out joint bank account and he paid the payments from our joint account.

We are selling the house. Do we need to pay capital gains? I was thinking I might, but maybe he doesn’t. I do have a primary house, but my grandson only has this house.

Margie,

That’d likely be a question for a CPA or tax professional, sorry.

Hi Colin,

I would like your insights on something if you have the time. I am looking into purchasing a property listed as a single family residence and income property. The one 3.3 acre property has 8 separate houses on it. I would live in one of the houses as my primary residence. The other 7 are already rentals with tenants occupying them.

With this, could I apply for a primary residence loan because it would be my primary residence? This is also my first house purchase. Or would this qualify as an investment property? Also in any case could I use the rental income for approval on a loan. Any insight would be extremely helpful. Thanks

Jackie,

The occupancy part sounds like primary since you’d be living there and own no other property, but not sure it’d be considered residential with 8 houses on the lot. May want to run it by a few lenders/brokers to get some clear answers. Good luck!

Thanks for the useful info! My partner and I are in the process of buying our first home, however he will be the only one on loan but we will be on the title together. We are not married, we do not file joint.

If later down the road, I chose to take a loan out on another property, mainly for my parents to live in, what would that scenario look like? Would it be considered a vacation home even though hopefully it would be close by? or because I’m not on the first loan, would I be considered first time home buyer?

Sam,

It’s driven by occupancy, so if you don’t occupy yourself, it’s not primary. If you vacation there, it can be a second home, so long as you don’t rent it out. Otherwise you’re looking at an investment property.

I’m interested in refinancing a house I consistently drive to on Fridays at 5:00pm and return to get back to work Mondays by 8:00am. I spend most of my holidays and vacations there. I stay with family on work days. This is my only house. Does this qualify for primary residence in California? Am I at my home 4 days a week since I’m there Friday through Monday? Or do I need to actually count hours? If I count hours, do I include the commute to and from my house? I plan to register my car and change my license address. I can also work remotely, but I’d much rather work at the office.

Rob,

If it’s your one and only property, and you consider it your primary (and it makes sense to be that), the underwriter will hopefully classify it as such. But you may need a letter of explanation to connect the dots. Also may want to speak to a broker or loan officer before loan submission for their interpretation regarding occupancy.

Colin,

I own my primary residence but I also have a rental property that is Paid Off.

I would like to borrow 20 to 30K for extra cash. Is it possible to get a mortgage or personal loan against using my Paid Off property as collateral?

John

John,

Not sure about personal loans, which I don’t think require collateral, but if you were to take out a mortgage, it’d likely be a home equity loan/line seeing that the loan amount is probably too small for a traditional first mortgage. Could also explore a cash out refi on the primary assuming you had equity and it was favorable mortgage rate-wise.

Hi Colin,

My wife and I are building a new primary residence and a vacation home both of which will be completed in April 2021 and both are roughly the same price. We will purchase one property outright and pay cash and the other property will carry a mortgage. We will put roughly 25-30% down on the mortgaged property.

Can we buy the vacation home for cash and mortgage our primary home to secure a lower interest rate?

Gary

Gary,

Generally rates are lower all else equal for a primary home vs. vacation home, but you may want to compare mortgage rates for different occupancy types with your parameters to see the difference and whether it’s worth making one the primary and vice versa (assuming that’s up in the air). Just be sure the one you choose as primary makes sense and isn’t going to result in additional underwriter scrutiny.

All,

I recently bought a place as a primary residence but have to immediately rent it out as something came up at work (Washington DC); bought the place in Orlando, FL. I’ve been told by my property manager that I need to at least change my insurance policy to investment property. Now, i understand that my lender is going to get informed of this policy change. Do i need to inform my lender before my insurance company does to avoid mortgage fraud? Do i need to reach out to my lender or can i just wait to see if they care or not?

Dustin,

You may want to see what you signed in terms of occupancy requirements and act accordingly – generally the language is something to do with your intention to occupy, but if the unexpected comes up it can be legitimate to rent out.

Good article! I do have a question though. My wife and I plan to move to Tennessee in maybe 3 years, or sooner. Our home is paid off and we want to buy a home now in Tennessee. Our daughter will occupy it until we move. No rent. A couple of lenders are telling us we would have to take out a loan for a second home since WE will not be living there for 2 or 3 years. Is this correct even though we do plan on moving there permanently? It doesn’t seem fair we will be paying a second home mortgage with a higher interest rate after we move there. Thank you in advance!

Bill,

Yeah, unfortunately occupancy is based on immediate plans, not future plans. Because then everyone could claim that their second home or investment property would eventually be their primary home…an alternative could be to structure it where daughter buys as her primary, but that could involve more unwanted steps, tax issues, and so on. Might want to compare rates on second home vs. primary, it may only be an .125% to .25% higher. Good luck!

Thank you! Such a helpful article and thread!

Question, my husband and I sold our home and went full time RV for a few months and are now ready to settle in a little more but not back in to a forever home. As empty nesters we were thinking maybe we could by a townhome and live there a year or two then maybe it would become an rental either short terms long. But we found a place we would want to be in long term but would be good for investment as a rental.

What’s the difference if we buy one first or the other?

Scenario 1

Buy small one that would be primary for 2-8 months while we make it rental ready and buy one we want to be in for a couple years

Scenario 2

Buy the one we want for a few years then buy the small one as a investment straight out

The end is the same but am I right we save money in scenario one since, at least initially, it’s primary for some time and then investment?

Thank you

Hi Jenna,

In order for a property to be your “primary residence” you typically need to live there at least 12 months. The difference comes down to loan pricing and also flexibility in financing.

As noted in the article, mortgage rates are lower on primary homes, and you can typically get a higher loan amount and/or higher LTV. So it can be beneficial to buy and live in a property before you eventually convert it to an investment. But this may not always be feasible/practical.

Your timing question is tricky because who knows what will happen with home prices and mortgage rates in the future? You’ve got to consider that and where you ultimately want to live in terms of your comfort.

Either way, making at least one property primary for the minimum period could be a money saver.

I have a fully paid home (no mortgage) that is my primary residence on the West Coast. I am purchasing a second home on the East Coast in which my kids (in their early 20s) will be staying, and I will periodically be visiting 3-4 times a year, cumulatively for a month or so each year. Can I still consider this as a primary residence, especially as I do not have another mortgage?

Sandra,

It’s not so much about what you owe, as it is where you live. Mortgage or not, primary residence means the place where you reside the majority of the year.

Your article is great! May I ask a different version of a similar question already asked. I have a home where I live with my wife and kids. We genuinely started the search of a second home 80 miles from our primary, closer to the ocean, as our primary to be. While in the process of closing it, we started to run into conflicts with our (previously enthusiastic) kids because changing schools, losing friends etc. In one of our kids this derived into some mental issues that ended up affecting health (nutrition, etc). So in the weeks after closing this long escrow, we arrived to a family agreement that we were going to stay in our original home for the time being (initially one more year) and our new home was going to be used for summer, vacation, weekends, winter break. I don’t want to do anything wrong… the loan is in place. What should change? I’m pretty sure I have to change the insurance, but also talk to the lender?

Thanks

Andrew,

Changing occupancy type could completely change the terms of the underlying loan, including interest rate, maximum financing, etc. So it’s an important detail. Ultimately, lenders treat occupancy as an immediate arrangement, not what you might do with the property in the future. Otherwise everyone could claim their rental or vacation home will eventually be primary to save some money.

I have a small line of credit I’m paying on my primary residence. I inherited a paid off 2nd home 10 years ago and was occupied rent by my mother until 2 years ago. I have not rented this home as funds have dried up finish the last quarter of the renovation. My options seem to be: 1) sell take a tax hit or purchase another home for Airbnb or rental. 2)use the 2nd home as a second buisness and rent a room to my son. 3) try to get a high interest line of credit to finish 2nd home and rent, if I qualify.

Completely moving to the 2nd home isn’t an option as I run a studio buisness out of my first home. What are your suggestions to avoid the largest tax consequences but pay immediate debt issues.

Chris,

I’m not a tax guy unfortunately so can’t weigh in. Perhaps a CPA can advise. Good luck.