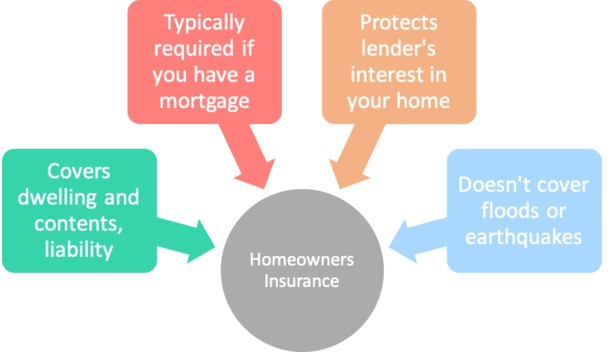

Homeowners insurance provides coverage in the event your home is damaged or destroyed, and also provides liability for injuries incurred by visitors to your property.

In addition, the loss or damage of property in and around the dwelling is covered as well (the contents).

The amount of money your home is insured for is called the dwelling limit coverage.

It is one of the most important and overlooked aspects of the mortgage process, and most homeowners fail to shop around for it.

Mortgage Lenders Typically Require Homeowners Insurance

- While homeowners insurance might be optional if you own your home free and clear

- Most mortgage lenders require a specific amount of coverage if you carry a home loan

- This protects their financial interest in your property

- Because remember, they let you finance a large chunk of it

Most banks and lenders require that homeowners buy enough insurance to cover the amount of their mortgage.

And your mortgage broker or loan officer will usually comply with the lender, and ask that you get a policy that simply covers the value of the loan amount.

But you should also ensure that your homeowners insurance policy covers the cost of rebuilding your property in the event of serious damage.

Your home is probably your greatest liability, and for many its also their nest egg, so full coverage is a must.

What is covered by homeowners insurance?

– Dwellings and other structures on your property

– Personal property

– Personal liability

What is not covered by homeowners insurance?

– Earthquake insurance

– Flood insurance

– Personal valuables beyond your coverage limits (think expensive jewelry)

Damages caused by extreme weather such as wind, lightning, hail, and fire are generally covered.

As are claims arising from vandalism, civil unrest, plumbing accidents, explosions, and events where a vehicle or aircraft causes damage to your home.

However, natural events such as earthquakes and floods require separate insurance.

Additionally, know your policy limits because expensive items aren’t automatically covered (think jewelry), and may need their own extended coverage.

Knowing the cost to rebuild your home is one of the most important and misunderstood aspects of homeowners insurance.

Many homeowners feel that coverage based on the value of their home is sufficient.

But in reality, the value of your home may be less than (or more than) the actual cost to rebuild it from the ground up.

And construction costs may rise as property values fall, so it’s important to gauge the cost of a complete rebuild.

How to estimate the value of your home:

– Style of your home

– Number of rooms

– Square footage

– Local construction costs

– Other structures on your property

– Special features

Do note that if you make any significant improvements to your home, you should also increase your coverage in the event that you need to rebuild.

And if you have expensive valuables such as fine art, jewelry, etc, it’s best to insure those separately if your coverage has lower limits.

Make sure they are insured for replacement cost and not ACV, or actual cash value, which is the depreciated value.

Set your policy to update each year based on inflation and rising building costs, and ensure that your policy covers living expenses while your home is being repaired if the damage is too severe to stay in your home during construction.

Make sure you take the time to shop around and understand the homeowners insurance policy you ultimately purchase (types of homeowners insurance).

Most borrowers simply take whatever policy is thrown at them, or worse, purchase the minimum required by their bank or lender.

For many homeowners it’s simply a stipulation or requirement to get the deal done, much like car insurance, but failure to insure your biggest asset/liability properly could be the biggest mistake of your life.

Read more: Homeowners insurance vs. mortgage insurance.

- Trump Says Warsh Wants Lower Interest Rates, But Has a Political Board - July 30, 2026

- Do Mortgage Rates Need a Hike to Move Lower? - July 28, 2026

- How Mortgage Rates Avoid a Return to 7% - July 24, 2026

I have not found this to be true at all. All the lenders I have spoken to require rebuilding cost coverage as a requirement for the loan. Can you provide even one lender that doesn’t ?

Most banks and lenders require that homeowners buy enough insurance to cover the amount of their mortgage. And your mortgage broker or loan officer will usually comply with the lender, and get the borrower a policy that simply covers the value of the loan amount. But you should also ensure that your insurance policy covers the cost of rebuilding your property in the event of serious damage. Your home is your greatest liability, and for many their nest egg, so full coverage is a must.

Dennis,

I have been in the process of buying a home recently. We applied for 7 mortgages. None of them required rebuilding cost coverage as a requirement for the loan. This is in Pennsylvania for what it’s worth.

Are you kidding me. I can only cover the loan amount? They have been telling me I have to cover replacement value.

I work in insurance and for most, the rebuild cost of your home will be significantly less than your loan amount. A mortgage provider can require you to insure for the rebuild cost of your home, however they cannot require that you insure for the full loan amount (it’s illegal for them to do so). Even if you did voluntarily increase your dwelling limit to match a loan cost that is greater than your rebuild cost it would actually be a huge waste. If there was a total loss and the home needed to be rebuilt, the insurance company would only pay the actual rebuild cost anyway, despite any higher limit you may have.

I am in the last week of purchasing a home in Texas and the lender is requiring me to purchase homeowners insurance for the amount of the loan $250,000, yet the insurance will not go up that high because the home is only worth $150,000 at most. The sales price includes 6 acres. I don’t understand how this is possible the land isn’t going anywhere. Do you have any idea about this?

I have a different question. I might be able to buy a “Victorian” style house dirt cheap. We’re talking turrets, chimneys, conical roofs, interior wood trim, etc. (Estimated to be built in 1900.) But the cost to rebuild it, should it be destroyed, would probably be at least 10 times its current sale price. Do I “have” to purchase homeowner’s insurance that will pay for a rebuild of such a house? (Say, $500k – $1mil.) Or, can the house be insured for maybe $100k-$150k and then, if the house is destroyed, the policy would simply replace the house with a “new” house that costs 100-150k to build?

I am having the exact same issue as you in Canada. We purchased a house for $222,000 and our bank is making us count that as the rebuild value. But when the insurance company’s do their calculation the rebuild doesn’t come to enough. Why would our lender require us to insure for a rebuild of $222,000 when that price includes land and we put 20% down so our mortgage is only $178,000. Did you find out any answers?

I wish I could insure for just the loan amount. I got my house, that was built in 1897, very cheaply. But the rebuild costs are far higher and I’m having a hard time finding an insurer that wants to cover my house.

I have similar. Old home with 3 builds worth $250k but $1.8 million to rebuild!!! What?! And my insurance company of 13 years suddenly decided they would not renew my policy as I was not in agreement to more than triple my premium on 1 months notice! Amica insurance if anyone was wondering.

Daniel: Try Foremost. They insure homes on the national historical registry.