These days, it seems as if you can insure just about anything. Your car, your house, your dog, your phone, and maybe even your hair?

At one time, there was a form of home down payment insurance, which at last glance appears to no longer exist.

While all these new policy options may be perceived as “great news!” by overzealous insurance agents, for individual consumers it’s often just more money down the drain.

After all, paying for insurance always feels like a chump’s game until you actually need to file a claim, which never seems to happen if you actually have insurance in place.

And if you do file a claim, your insurance rates will go up! What a deal!

When you purchase a home, your insurance needs will certainly rise, which will put even more strain on your already-strained checkbook.

Let’s look at two common forms of insurance tied to homeownership, and explore what each actually provides.

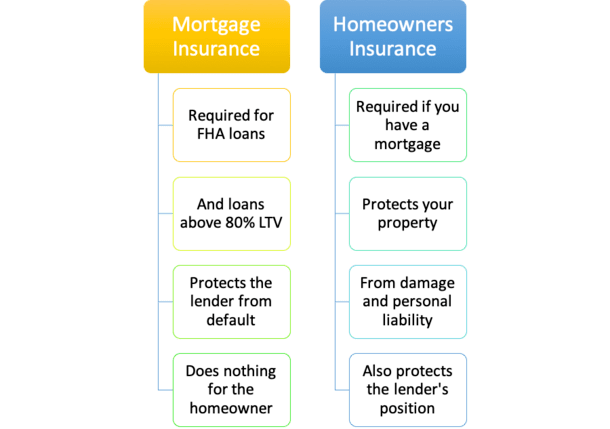

Mortgage Insurance Protects the Bank/Lender

- Mortgage insurance doesn’t protect homeowners

- It protects the mortgage lender from payment default

- It exists because they’re taking a bigger risk by offering you a home loan with very little down

- The trade-off is you get a mortgage despite having a sizable down payment

If you’ve been shopping for a home (and a home loan) lately, you may have heard about mortgage insurance.

At first glance, it might sound like something that protects you in the event you can’t pay the thing.

But contrary to what you might believe, mortgage insurance doesn’t do anything to protect the homeowner.

Conversely, it serves to protect mortgage lenders in the event of borrower default, something deemed necessary when you put down less than 20% on a home purchase.

In short, you pay extra for the additional risk you present to the lender. And until your loan-to-value ratio (LTV) dips below 80%, you’ll continue to pay that premium.

If you take out a conventional loan above 80% LTV, you’ll need private mortgage insurance (PMI), which your lender will facilitate when going through the loan process.

If you take out an FHA loan, you’ll get mortgage insurance through the FHA. And it’s not avoidable, even if you’re able to put down 20% or more.

So we know a little more about mortgage insurance, but let’s talk about what it isn’t.

It is not insurance that protects you in the event you can’t make your mortgage payment.

For example, if you lose your job or fall ill and are unable to make payments, mortgage insurance does not cover you.

That’s an entirely different product known as “mortgage protection insurance.” Yes, there’s insurance for every single possible situation folks!

It also doesn’t cover you if your home value falls, or if anything else nasty happens to your home or your mortgage. Again, it’s not for YOU. It’s for the lender! And you pay for it!

This is yet another reason to put 20% down when buying property. The other reason is a lower mortgage rate, which are often cheaper at lower LTVs.

Check out my PMI calculator to ballpark costs if you plan to put less than 20% down.

Homeowners Insurance Protects You

- You have to buy homeowners insurance if you have a mortgage

- But this type of policy actually protects you in the event of property damage or liability

- So the coverage is beneficial to the homeowner if something catastrophic takes place

- It indirectly protects the lender too because the home serves as collateral for the loan

I assume a lot of individuals get homeowners insurance and mortgage insurance confused, and for good reason.

They sound pretty similar, but don’t share much in common.

Homeowners insurance is actually in place to protect YOU, the homeowner, from perils that exist and may cause damage and monetary loss.

So if a fire burns down your home, or a tree crashes through your roof, your homeowners insurance should be triggered.

And the insurance company should pay to fix any damages, less your deductible.

In other words, homeowners insurance serves the owner of the home, not the lender. It also has nothing to do with your home loan, though there is some overlap.

Technically, if you own your home outright, you don’t NEED to get homeowners insurance. But you’d be pretty foolish not to purchase it if your home has any significant value.

Without it, you could expose yourself to major financial risk, which clearly isn’t wise with insurance premiums relatively cheap in the grand scheme of things.

And you certainly wouldn’t want to jeopardize your ability to make mortgage payments if all your money was caught up in home repairs.

Homeowners Insurance Also Protects the Lender’s Interest

While homeowners insurance does indeed benefit the homeowner, it also protects lenders (even though you pay for it).

Why? Because most individuals don’t actually own their homes free and clear, or anywhere close to it.

Remember how mortgage insurance is required if you put very little down on a home purchase? Well, a lot of people put very little down!

The average down payment ranges from like 6-12% depending on the survey/data set, so most homes across America are majority-owned by banks and mortgage lenders.

This also explains why you MUST take out a homeowners insurance policy if you have a mortgage, to protect the lender’s interest.

At this point, you may be thinking it’s all about the lender. But when it comes down to it, you’ve got a massive loan on the property, so it’s really the bank’s more than it is yours.

And without insurance in place, in the event of a major loss, most homeowners would probably run, not walk, away from the property.

Lenders know this, which is why they demand that you buy homeowners insurance.

The good news is mortgage insurance is totally avoidable. Just bring more money to the closing table or check out lender-paid mortgage insurance.

You might also be able to find a lender that doesn’t charge it. Just know if you put less than 20% down and they aren’t charging it, it’s baked into your (higher) mortgage rate.

Mortgage Insurance vs. Homeowners Insurance

| Mortgage Insurance | Homeowners Insurance | |

| Required on… | FHA loans and mortgages with less than 20% down payment | Any property with a mortgage |

| Protects the… | Lender from borrower default | Homeowner and lender’s interest in the property |

| What does it cover? | Borrower’s inability to make payments (foreclosure) | Liability and property damage |

| Who pays for it? | The borrower | The borrower |

| How is it paid? | Either monthly, upfront at closing, or lender-paid | Annually or monthly via an escrow account |

| How can it be avoided? | By putting down 20% and/or taking out a conventional loan | Owning a property free and clear (though you may still want to keep the insurance!) |

- Despite Headwinds, Odds of a 7% 30-Year Fixed in 2026 Are Super Low - July 9, 2026

- Just When You Thought 7% Mortgage Rates Were Off the Table - July 8, 2026

- Light Week for Economic Data Means Flat Mortgage Rates Likely - July 6, 2026