It was a good week for mortgage rates thanks to tame inflation data.

I use the phrase “good” loosely because mortgage rates didn’t really come down during the week.

However, they didn’t move much higher either, so we can call it a win for now.

We got a lot of inflation data this week, and fortunately it came in cooler-than-expected.

Had it been hot or even at consensus, rates may well have hit a fresh 52-week high. But perhaps we’re just delaying the inevitable anyway.

Cool Inflation Data Gives Mortgage Rates a Much Needed Breather

As noted, this week was a big week for inflation data, with both CPI and PPI released.

Both reports showed cooler-than-expected inflation, which is bond-friendly.

When economic data comes in cold, mortgage rates tend to fall. The opposite is also true.

You don’t want high inflation because bond investors will demand higher yields, aka interest rates, in return.

The good news is inflation was tamer than most thought it would be, with consumer prices in June dropping the most since April 2020.

Similarly, the Producer Price Index (PPI) dipped 0.3% in June, the biggest drop in 14 months and well below the 0.0% expected.

The end result was slightly lower mortgage rates, which had matched their wartime-highs on Monday thanks to new aggressions in the Middle East.

So any hot reports would have been more than enough to push mortgage rates up to the next rung, whether it was 6.875% or even higher.

We’ve been able to evade the dreaded 7-handle all year, but that doesn’t mean it can’t surface again.

And either way, we’re more than likely going to hit a fresh 52-week high again.

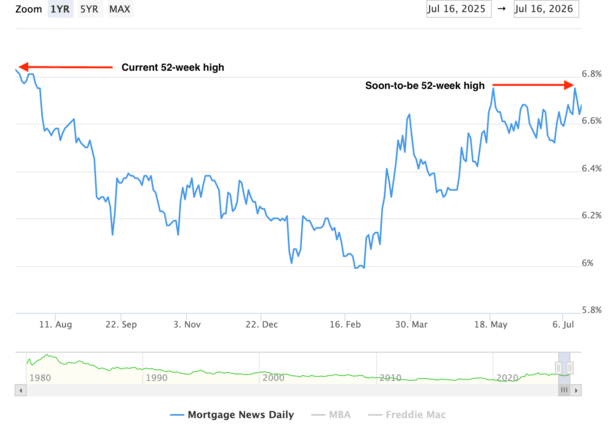

Mortgage Rates Don’t Need Much Bad News to Hit a New 52-Week High

The 52-week high for the 30-year fixed is 6.82%, per Mortgage News Daily. It was reached back on July 17th, 2025, essentially a year ago.

However, mortgage rates moved sharply lower thereafter, plummeting to around 6.50% that August. Then briefly fell close to 6% in September.

We all know they eventually went sub-6% in February of this year, before the war with Iran drove them abruptly higher.

They’ve ebbed and flowed since, but have remained elevated due to the uncertainty in the Middle East.

The core issue has been oil prices, which surged in response and put renewed pressure on inflation.

There’s also the matter of all that military spending, which might result in even more government debt (and bond issuance). Again, not good for bonds and thus interest rates.

The point here is mortgage rates were quite a bit lower in the second half of 2025, so the new 52-week high will drop to 6.75%, which we saw most recently on Monday. That’s also the 2026 calendar-year high.

If things don’t miraculously improve soon, we could be at new 52-week highs.

If nothing else, we’ll cross above our year-ago levels. When that happens isn’t 100% clear, but it’s looking like sometime in early August.

A year ago, the 30-year fixed slipped about 25 basis points (0.25%) after the July jobs report came in below expectations along with massive revisions for May and June.

So we’ll likely be above August 2025 levels at the very least. Not great optics for home buyers.

Lately, employment has been fairly steady and the story has been more about war-driven inflation.

But if jobs take another turn lower, mortgage rates could benefit yet again like they did last year.

More importantly, if this war actually gets resolved, we could see a big move lower as well.

However, before all that happens, mortgage rates will likely reach new 52-week highs and could even dance with a 7-handle.

So watch out!