What a difference a year makes.

While the mortgage industry has been purchase loan-heavy for several years now, it could finally be starting to shift.

A new report from Optimal Blue revealed that rate and term refinance volume increased nearly 110% in August from a month earlier, and 310% from the year before.

Driving the emerging trend is cheaper mortgage rates, which have finally begun to accelerate lower in recent months.

Assuming they continue on their newfound trajectory, there’s a good chance refis will be back en vogue in 2025 and beyond.

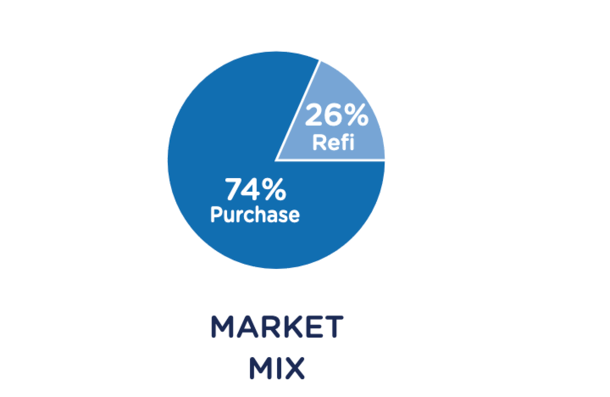

Mortgage Refinance Share Highest Since Spring 2022

It has been a rough few years for loan officers and mortgage brokers, but it’s possible the worst is over.

As mortgage rates nearly tripled from sub-3% levels in early 2022 to over 8% last year, originators came up with the saying, “Survive ‘til 25.”

The idea was that if you could hang on and ride out the storm (of low lending volume) in 2024, you’d be rewarded in 2025.

And while that sometimes felt far-fetched, it looks like it could actually come to fruition, and perhaps even ahead of schedule.

The latest Market Advantage report from Optimal Blue found that mortgage refinances accounted for 26% of total home loan production, the highest share since March 2022.

At that time, you could still get a 30-year fixed in the 3% range. But rates ascended rapidly from there, basically wiping out all refinance activity in a matter of months.

So it’s pretty telling that refinance market share is now back to those levels and likely rising in coming months and years.

The 30-year fixed has fallen fairly dramatically after peaking at around 7.25% this May. It now stands at around 6% and looks poised to hit the 5s sooner rather than later.

Rates have a pretty strong tailwind right now with weakening economic data, higher unemployment, and a bunch of Fed rate cuts in the pipeline.

That could unleash millions of additional refinance candidates, including many of four million who took out a 6.5%+ rate mortgage since 2022.

The Only Way Is Up

While this is great news for the mortgage industry, and for recent home buyers, loan volume is still small potatoes relative to recent years.

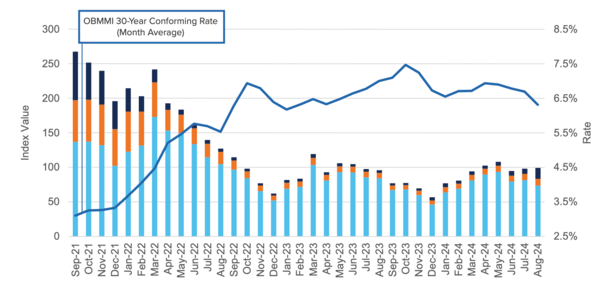

If you look at the chart above, you’ll see the context of that 109% monthly increase and 310% annual surge.

The dark blue vertical line (rate and term refinance share) has gotten a lot wider, but is still just a tiny sliver of overall mortgage market volume.

But when you compare it to levels seen in 2021 and early 2022, it doesn’t take much to register big percentage gains.

When we include cash out refinances (orange line), which increased 8% on a monthly basis and over 20% annually, you get a respectable refinance share again.

And chances are this will only go up as more mortgages fall into the money for a refinance.

Lately, it’s mostly been VA loans that have benefited from a refinance because mortgage rates on such loans are the lowest.

But if rates continue on their merry may lower, you’ll start seeing more conforming loans benefit, which make up the lion’s share of the market.

It has been harder to make the math pencil on loans backed by Fannie Mae and Freddie Mac because of LLPAs (pricing adjustments). That could soon change.

Home Purchase Lending Has Fallen Flat Thus Far

While refis are finally having a moment, the same can’t be said of home purchase lending (light blue vertical line above).

Sure, it still holds a majority share of the mortgage market and likely will next year too, but it’s beginning to cede some of it back to refis.

And that’s troubling given the big drop in mortgage rates, which was supposed to get home buyers off the fence.

So far, the effect of lower mortgage rates has been muted, with purchase locks actually down 16% year-over-year and a staggering 45% since August 2019.

Optimal Blue blamed it on “continued affordability and inventory challenges,” with home prices out of reach for many despite the improvement.

Many expected home prices to surge when rates fell, but I’ve been arguing for a while that there’s no inverse relationship.

And in fact, home prices and mortgage rates can fall together if economic conditions warrant it.

Remember, there’s a reason the Fed is looking to cut its own fed funds rate more than 200 basis points (bps) over the next 12 months.

A slowing economy might be good news for mortgage rates, but not necessarily the housing market.

With home prices still at all-time highs nationally and affordability near all-time lows, it’s just not a great time to buy for many folks.

Sprinkle in uncertainty regarding the economy, the election, and even how they’ll pay real estate agent commission and it’s not so rosy anymore.

In other words, significantly lower mortgage rates might not amount to higher home prices, or a greater number of home sales just yet.

But given the timing of these lower rates (post peak home buying season), we won’t really know for sure until next spring.

That’s where the rubber meets the road.

- Can You Get a 4% Mortgage Rate Still? - August 10, 2026

- Mortgage Rates Catch a Break as Job Growth Goes Negative - August 7, 2026

- Mortgage Rates Move Higher on Jobs Report Defense - August 6, 2026