If you’ve got a home equity line of credit (HELOC), payment relief may finally be here.

The Fed is expected to “pivot” today, meaning they’ll shift from a tightening monetary policy to a loosening policy.

In other words, they’re going to start cutting rates instead of raising them!

While this won’t have a direct impact on long-term mortgage rates, it directly affects loans tied to the prime rate, including HELOCs.

This means your HELOC rate will go down by whatever the Fed cuts. So if they cut 25 basis points today, your HELOC rate will be adjusted down 0.25%.

Though one cut isn’t likely to provide major relief, there are expectations that this is the first cut of many, with possibly 200+ bps of cuts penciled in over the next 12 months.

So if you’ve been given the option to “lock your HELOC rate,” it’s probably best to give it a hard pass.

How HELOC Rates Are Determined

As a quick refresher, HELOCs are variable-rate loans, meaning they can adjust each month based on the prime rate.

To come with your HELOC rate, you combine the HELOC’s margin, which is fixed, and the prevailing prime rate, which moves in lockstep with the fed funds rate.

Whenever the Fed decides to raise or lower its own fed funds rate (FFF), the prime rate will also go up or down by the same amount.

Since early 2022, the Fed has raised the FFF 11 times, from near-zero to a range of 5.25% to 5.50%.

Today, they are expected to lower the FFF either 25 or 50 bps. This means banks will lower the prime rate by the same amount shortly after.

Quick note: The Fed does not control long-term mortgage rates, so their action today won’t directly impact the 30-year fixed. If they cut the 30-year fixed could actually rise today!

Anyway, let’s assume you have a margin of 2% and prime is currently 8.50%. That’s a 10.50% HELOC rate. Ouch!

But if the Fed cuts 25 bps or 50 bps today, that rate will fall to 10.25% or 10%. Okay, we’re getting somewhere.

Still not a low rate, though it’s finally not going up and in fact is coming down.

Now factor in another 200 bps of cuts and the rate is down to 8%. Sweet, that could actually result in some decent interest savings and a lower monthly payment!

What Is Locking Your HELOC Anyway?

That brings us to “locking your HELOC.” As noted, HELOCs are variable-rate loans.

But the banks will sometimes give you the opportunity to lock the interest rate in for the remainder of the loan term. This happened to my friend, who asked today if he should lock in his rate.

This only happens once you’ve had the HELOC open for a period of time and made draws on it. Not upfront, otherwise that’d simply be a fixed-rate home equity loan.

So Bank X might say hey, we know rates have been rising and there’s a lot of uncertainty out there.

If you don’t want to deal with any further adjustments, you can lock in the rate you currently have.

For those not paying attention to the Fed, this might sound like a decent idea. After all, many homeowners are risk-averse, which is why they also don’t tend to go with adjustable-rate mortgages.

And many borrowers may not have actually known that their HELOC was variable to begin with.

They could jump at the offer to lock in the rate and stop worrying. But this could actually be a terrible time to do that.

You watched helplessly as your HELOC went up and up over the past couple years. And now you’re going to lock it in, when rates are finally slated to fall?

Probably not a good idea. This would just benefit the bank, who will make a lot less if you simply do nothing and let the rate fall as prime drifts lower and lower over the next 12 months.

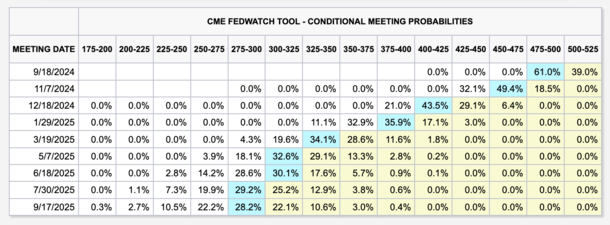

If you’re curious where the prime rate is expected to go, keep an eye on the fed funds rate predictions. A good place to do that is the CME website.

They’re currently predicting a prime rate that is 2.25% lower by September 17th, 2025, as seen in the table above.

In other words, if you have a HELOC set at 10% today, it might be 7.75% in 12 months. Don’t lock in the 10% rate and miss out on those savings!

Update: The Fed cut its own rate 50 basis points today, so HELOCs will be .50% cheaper at their next adjustment (typically 1st of next month). Nice little win for those who already hold one.

- Mortgage Rates Narrowly Avoid New 52-Week Highs as Bond Yields Surge Higher - July 31, 2026

- Trump Says Warsh Wants Lower Interest Rates, But Has a Political Board - July 30, 2026

- Do Mortgage Rates Need a Hike to Move Lower? - July 28, 2026