Even though mortgage rates have fallen quite a bit from their highs seen a year ago, they remain quite elevated relative to much of the past decade.

Sure, a 6% 30-year fixed is better than an 8% 30-year fixed, but it’s still a far cry from a 3 or 4% 30-year fixed.

This might explain why prospective home buyers haven’t exactly rushed back into the housing market in recent months.

And now we’re being told this is as good as it’s going to get for mortgage rates. That remains to be seen, but what’s interesting is I’ve seen quotes down into the high-4s for mortgage rates recently too.

So how are lenders able to advertise rates that low if the Freddie Macs of the world are telling us rates are still above 6%?

Well, the secret is a little thing called mortgage discount points.

Mortgage Rates Are Lower When You Pay Points

After mortgage rates surged since beginning in early 2022, the secondary market where investors buy and sell mortgage-backed securities (MBS) got all out of whack.

Basically, uncertainty and volatility surged while volume plummeted. Long story short, MBS investors wanted more assurances, which generally meant borrowers had to pay points upfront.

This ensured a profit even if the mortgage was short-lived and paid off in a short period of time.

It also allowed lenders to keep mortgage rates from going even higher, completely decimating lending volume in the process.

Conditions have since improved, and it’s again possible to get a home loan today without paying points.

But you’re still seeing lenders offer rates with points attached. And the reason why is because you can offer a lower rate!

Obviously, it looks a lot better if you’re able to advertise a rate starting with a 5 instead of a 6, or a 4 instead of a 5.

And that’s exactly what some lenders do, at least the ones that lead on price as opposed to service or brand name.

Interestingly, I discovered over the weekend that this isn’t a new phenomenon. Back in the 1980s and 1990s this was also common.

Homeowners Paid Over Two Points on Average from 1981 to 1991

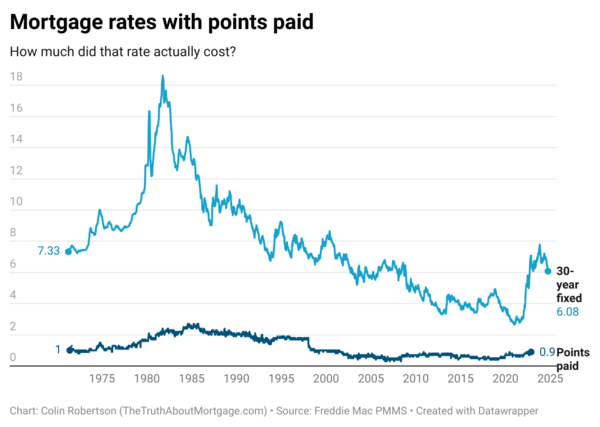

Remember those super high mortgage rates in the 1980s? Well if you don’t, the 30-year fixed climbed as high as 18.45% in late 1981, per Freddie Mac.

Despite the rate being astronomically high, the average amount of discount points required at that time was a whopping 2.3.

In other words, on a $250,000 loan amount, you’d be talking about $5,750 in fees just to obtain that ridiculously high rate.

Did that mean a borrower who only paid one point would have been subject to a 20% rate? Perhaps, I don’t know, but that’s generally how it works.

If you opt to pay less or nothing upfront, your mortgage rate will be higher, all else equal.

This average amount of points paid by homeowners hit its peak in 1984 and 1985, when the average amount paid was 2.5 points.

So for every $100,000 borrowed, a home buyer would have to fork over $2,500. And again, to wind up with a mortgage rate around 12 or 14% (they came down a bit after peaking in 1981).

Are Mortgage Rates That Require Upfront Points Legit?

Now that brings me to modern day, where lenders still charge multiple points for the lowest rates.

While not obligatory, as I mentioned, you do typically have the option to pay points at closing.

The tradeoff being a lower interest rate if you do. This is essentially what home builders have been doing to draw in business with their permanent and temporary rate buydowns.

They’re buying the rates down to lure in home buyers, which allows them to keep their asking prices steady (or even rising).

Those who comparison shop mortgage rates may also find that some lenders are offering “below-market rates” versus what they see in the mortgage rate surveys.

The way lenders accomplish this is by asking you to pay points upfront, which are a form of prepaid interest.

So the rate offered might be 6% with no points or for a no cost refinance. But 5.25% if you’re willing to pay a point (or more than a point) at closing.

These are entirely legit rates, they just cost money to obtain them. And that cost is essentially an investment in the mortgage that you’ll only realize if you hold it long enough.

Paying Points at Closing Might Not Be the Best Move

While the promise of a lower mortgage rate, especially something that starts with a 4 is enticing, it might not be worth it.

Let’s consider a quick example where you pay two points to get a rate of 4.875% versus a rate of say 5.75% with no points.

On a $500,000 loan amount that would set you back $10,000 at closing.

The monthly payment would be $2,646.04 versus $2,917.86, or roughly $272 per month.

While that’s a decent amount of savings, it would take about three years to breakeven on the upfront cost.

Now imagine then 30-year fixed falls to the mid-4s or even lower during that span. Or if you want to sell your home and move.

You’ve already paid for the lower rate and might not get the full benefit. This is not to say it’s a bad decision, since you, me, and everyone else doesn’t know what the future holds.

But you’re making a conscious choice when paying points and there are no refunds.

If we look back at those folks who paid 2.5 points back in 1984 for a 14% rate, only to see rates fall to sub-10% by 1986, it makes you wonder.

- Are Mortgage Rates Finally Poised to Start Falling Again? - June 25, 2026

- Mortgage Rates Are Having a Good Day as Oil Prices Fall to Pre-War Levels - June 24, 2026

- You Can Still Get a Sub-6% Mortgage Rate, But Is It Worth It? - June 23, 2026