Month after month, and week after week, articles continue to focus on mortgage rates in the 1980s, to seemingly paint a picture that rates are still historically low.

And it’s pretty much always the same narrative – be happy with your 6%, 7%, and maybe 8% mortgage rate today because there was a time when it was a lot worse.

It runs parallel to the stories of having to walk to school uphill both ways, in the snow, without shoes or a jacket.

Suck it up, stop complaining. Today’s mortgage rates aren’t that high! That’s the message.

It also doubles as a sales pitch to remind you that a 7% mortgage rate isn’t bad, and could be much higher, so don’t look a gift horse in the mouth.

Why Do 1980s Mortgage Rates Matter Today?

There’s an article from CNN that talks about mortgage rates in the 1980s, complete with the “Think mortgage rates are high now?” headline.

It goes on to talk about how baby boomers dealt with interest rates as high as 19% in late 1981 when they peaked.

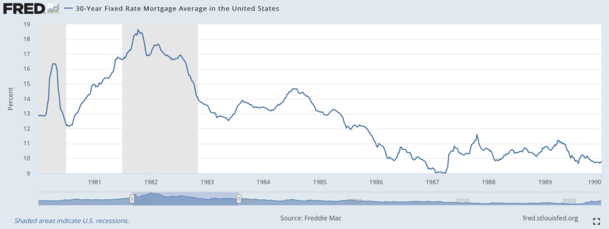

The 30-year fixed averaged around 9% in early 1978, before climbing to 10% later that year, 13% in 1979, and near 15% in 1980.

Mortgage rates then hit an all-time high in October 1981, averaging a staggering 18.45%, per Freddie Mac data. The chart above from FRED illustrates this movement.

But guess what? Earlier generations not only dealt with them, but were delighted to close with a rate at 19%. I guess it’s all relative, and 19% sounds a lot better than 20%, right?

A realtor quoted in the story adds that “our kids are shocked by 6%,” another one of those classic toughen up jabs at the younger generation.

Here’s the problem though. It’s not an apple-to-apples scenario, just like the boomers didn’t walk to school uphill, both ways.

It’s probably easy to think back to those times and remember it being a lot harder, but does the math agree? Or is it just a fuzzy memory?

Down Payments Were Higher and Home Prices Were Lower in the 1980s

Back in the early 1980s, home prices were a lot lower than today, even once inflation-adjusted.

While numbers vary by source, let’s say the typical home back in 1981 was going for around $65,000. In today’s dollars, that’s about $212,000.

Meanwhile, the median down payment was around $20,000 in 1981, despite home prices being so cheap relatively.

We’re talking a 30% down payment, give or take. At the same time, a quarter of home buyers surveyed back then said they could afford a down payment of $40,000 or more.

Long story short, there were smaller loan amounts and lower loan-to-value ratios (LTVs) in the 1980s.

Today, the median down payment is $27,500, per ATTOM Data Solutions for homes purchased with financing during the third quarter of 2021.

That represented just an eight percent down payment based on the nationwide median sales price.

Without getting too convoluted here, today’s home buyer carries a much larger loan balance, and thus a higher mortgage rate has a lot more impact.

If your loan amount is $45,000, an 18.5% mortgage rate isn’t so bad. It’s about $697 per month.

Now let’s consider today’s home selling for $400,000. You put down 10% and get a rate of 7%, resulting in a monthly principal and interest payment of about $2,395.

We’ll ignore the private mortgage insurance required for LTVs above 80%. It would take about 40% of today’s income (DTI ratio) to pay that mortgage each month (principal and interest only).

The $45,000 loan set at 18.5% in 1981 would only require about 37% of median income for that time period.

Using an inflation calculator from the U.S. Bureau of Labor Statistics, $697 in October 1981 would be about $2,215 today.

So despite that sky-high 18.5% mortgage rate, today’s home buyer is in a tougher spot with a 7% rate, without even factoring in compulsory PMI.

You Can’t Look at Mortgage Rates in a Vacuum

| 1981 Mortgage | 2022 Mortgage | |

| Purchase price | $65,000 | $400,000 |

| Down payment | $20,000 (31%) | $40,000 (10%) |

| Loan amount | $45,000 | $360,000 |

| Mortgage rate | 18.5% | 7% |

| Monthly payment | $697 | $2,395 |

| Household income | $22,390 | $72,000 |

| Inflation-adjusted payment | $2,215 | |

| Mortgage-to-income ratio | 37% | 40% |

Simply put, you can’t just look at two mortgage rates from different decades and conclude one is better or worse than the other.

Sure, a near-19% mortgage rate sounds incredibly bad, and certainly is much higher than today’s going rate of around 7%.

But one must also consider home prices, household income, and inflation. Without those details, it truly is an unverifiable walking uphill both ways type of story.

It’s also worth considering the astounding percentage rise in mortgage rates lately.

Back in 1981, they only basically doubled from early 1978 until their peak in late 1981.

From just the start of 2022, the 30-year fixed has gone from around 3% to 7% today, a 133% increase.

And that’s through about 10 months, much shorter than the nearly four years it took for rates to double in the late 1970s and early 1980s.

So let’s stop talking about mortgage rates in the 1980s.

(photo: Pascal Terjan)

- Mortgage Rates Narrowly Avoid New 52-Week Highs as Bond Yields Surge Higher - July 31, 2026

- Trump Says Warsh Wants Lower Interest Rates, But Has a Political Board - July 30, 2026

- Do Mortgage Rates Need a Hike to Move Lower? - July 28, 2026

You lost me when you stated average household income for 1981 at $22K. It was half of that. Not sure if I can trust any of your numbers.

Per the U.S. Census Bureau: “In 1981, the median family income was $22,390.”