With mortgage rates above 6.50% these days, the average home buyer today actually pays more in interest than the purchase price.

For example, a $400,000 home with 20% down and a 6.5% interest rate equates to $408,000 in total interest over 30 years.

And that’s if you put down 20%. Many home buyers do not put down 20% or anywhere close.

For these buyers, the math is even worse, something highlighted in a recent report from Best Interest Financial and Clever Real Estate.

While monthly payment might still be the focus, it’s yet another hard pill to swallow for a prospective home buyer today.

You Pay More In Interest Than the Home Costs?

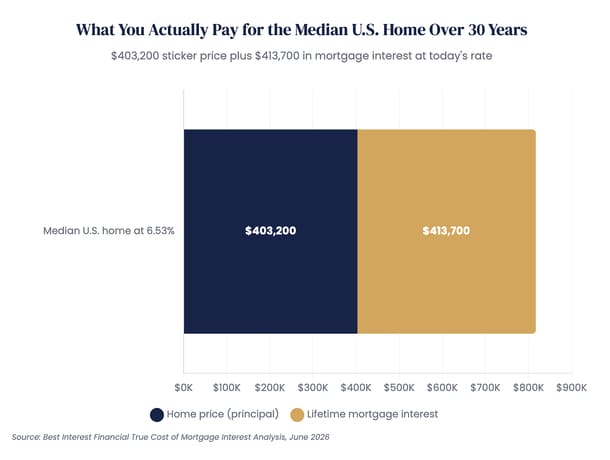

Best Interest Financial and Clever Real Estate came up with this interesting little graphic showing a median home price would cost more in interest over 30 years than the purchase price.

The reason is simple; mortgage rates are a lot higher today than they were in the recent past.

So a $403,200 home with a 20% down payment and a 6.53% 30-year fixed would set you back $413,700 in interest.

It might seem hard to believe given the interest rate is a low 6.53%, but that’s how mortgage interest works.

Because it’s amortized over such a long period of time, and the outstanding balance is so large for most of that time, you pay a ton of interest over three decades.

With a 20% down payment, total interest actually exceeds the home price once your 30-year fixed mortgage rate is over 6.4%.

Currently, mortgage rates are closer to 6.7% so the total interest expense is even higher than this.

To make matters even worse, the typical home buyer might put down as little as 3% (what Fannie Mae and Freddie Mac allow as an absolute minimum).

In this case, an interest rate of 5.45% is high enough so that total interest equals the purchase price.

As noted though, most folks only focus on their monthly payment and what they can afford, not what they’ll actually pay in interest over the life of the loan.

In addition, most won’t keep their loans for the full term for one reason or another, whether it’s an early sale, refinance, or prepayment.

The takeaway is that the lower the down payment, the lower the rate needs to be for total interest to not exceed the cost of the home.

For example, if you put nothing down on a home purchase, a mortgage rate as low as 5.30% means interest exceeds the purchase price.

Whether that matters to you is another question.

What You Can Do to Reduce Total Mortgage Interest

If it bothers you that you’re going to pay more in interest than what you paid for your home, there are options.

The nice thing about a mortgage is it’s typically permissible to prepay it as you see fit without penalty.

So if you want to pay an extra $250 per month, you’re able to do so. That would reduce the total interest expense significantly.

For example, let’s use a $400,000 purchase price with 20% down payment and a 30-year fixed rate of 6.75%.

The total interest is just over $427,000 over the full 30 years, assuming you keep the loan to term.

Alternatively, if you pay $250 extra each month the total interest drops to $296,623.

You’re no longer paying more in interest than the cost of the home. Woo hoo!

You’d also pay the loan off nearly eight years earlier as well. Nice.

The point here is that there’s optionality with mortgages and you’re not stuck with only the “minimum payment.”

If you have the means, you can pay extra whenever you’d like and reduce that interest expense.

Using the $250 extra example, you wind up with an equivalent interest rate of about 4.97%.

Meaning a 30-year mortgage set at 4.97% would produce almost exactly the same total interest.

Read on: Try my early mortgage payoff calculator to run your own scenario.

- How Mortgage Rates Avoid a Return to 7% - July 24, 2026

- Mortgage Rates Hit New 52-Week High - July 23, 2026

- Light Data Week Means Mortgage Rates Will Be Dictated by Middle East - July 20, 2026