Mortgages can be viewed very differently.

Some see them as a positive financial instrument, a way to free up their money so it can be invested elsewhere, ideally for a better return.

Then there are those who view mortgages as the root of all evil, as a debt overhang that must be terminated as quickly as possible.

Whatever your stance, you’ve probably entertained the idea of making “extra mortgage payments,” though you may not know the exact impact, due to the complexity of mortgage amortization.

Fortunately, there are early payoff calculators available that take the guesswork out of the process and make it easy to see how much you can save in a number of different scenarios.

Adding an Extra Mortgage Payment of $10 Per Month

- Even adding a nominal amount such as $5 or $10

- On a monthly basis over a long period of time

- Can save you thousands of dollars on your mortgage

- And shorten your loan term at the same time

Let’s start with a simple scenario where you add just $10 a month in extra payment to principal.

Assuming you’ve got a $100,000 loan amount set at 4% on a 30-year fixed mortgage, that extra $10 payment would save you $3,191.81 over the full loan term.

It would also shorten your mortgage by 13 months, meaning your 30-year mortgage would be a 28-year (ish) mortgage.

So that’s good news, right? You save thousands and you only have to pay a measly $10 extra per month. You probably wouldn’t even notice the difference.

What if you bumped up that extra payment to $25? Well, you would shave 32 months off your mortgage, nearly three years, and reduce total interest by $7,450.04.

Feeling ambitious? Add $100 a month and you reduce your term by 101 months, or nearly 8.5 years, while saving $22,463.79 in interest.

You can also just make your mortgage payments a solid round number and save money that way too.

The world is your oyster really, so long as your loan servicer understands and accepts that these payments are to go toward the outstanding principal balance.

Speaking of, make sure it’s very clear that any extra payments go to the right place. Often, you can’t make split payments, or payments for less than the total amount due.

So any extra should be on top of the minimum amount due for the month.

Some servicers will let you indicate where the extra should go, such as toward your escrow account or the principal balance.

If your goal is to pay the mortgage down faster, you’ll want it to go toward the principal balance.

Tip: If you can’t commit to the higher monthly payments associated with a 15-year fixed mortgage, extra payments could provide similar savings on a 30-year fixed.

Extra Mortgage Payments Are More Valuable Early On

- You get more value out of extra mortgage payments early on in the loan term

- Because the outstanding balance is larger at the outset

- And early payments are composed mostly of interest (front-loaded)

- Any extra payments will lower future interest for the remaining months, which will be more plentiful if you make them during the early years

As you can see, it’s not that hard to save a ton of money via extra mortgage payments, but it also matters when you start making those additional payments.

Using our $100 example, if you started making extra payments in year six of your 30-year mortgage (month 61), you’d only save $15,095.21, and shed just 78 months off your mortgage.

Even if you procrastinated for just one year to initiate the extra $100 payment, your total savings would drop to $20,989.55, and only eight years would come off your mortgage term.

In short, the earlier you start making extra payments, the more you’ll save. This is mainly because mortgage payments are interest-heavy in the beginning of the term.

[Are biweekly payments a good idea?]

One Extra Lump Sum Mortgage Payment

- An extra lump sum mortgage payment could be more valuable

- If made soon after you take out your mortgage

- Its value diminishes over time since less interest is due later in the loan term

- But it could be a better option than paying a little each month

Now let’s assume that you came upon some extra dough and want to make one lump sum payment to reduce your mortgage balance.

Using our same loan details from above, if you made a one-time extra payment of $5,000 to principal in month 13, you’d save $10,071.67 and reduce your loan term by 31 months.

Amazingly, this single extra mortgage payment would save you money each month for the next 30 years.

Just look at the amount of interest paid each month after the extra mortgage payment is made versus the same home loan without extra payments below.

As you can see, payment 14 above consists of $310.30 in interest, while it’s $326.96 for the mortgage without extra payments.

In month 15, we see the same disparity, with $309.74 in interest versus $326.46. So each and every month after the extra payment has been made, interest savings are realized.

Assuming the loan term is 360 months, it’s easy to see how the savings can really add up over time.

Of course, the borrower who pays extra won’t have to make payments the full 360 months because they’ll also wind up paying off their mortgage ahead of schedule.

Now I mentioned that paying extra earlier on in the loan term can save you even more because you can tackle that interest expense before you start paying it off naturally.

For example, if you made that same $5,000 extra payment at the beginning of year six of the mortgage (instead of the beginning of year two), the total savings drop to $7,943.99 and the term is only reduced by 27 months.

So again, it matters when you pay extra.

Making an Extra Mortgage Payment Each Year

- Some homeowners prefer to make an extra payment each year

- Perhaps related to a tax refund check or from a year-end bonus at work

- This is another good strategy to cut your mortgage term and save lots of money

- And ensure that the bonus money you receive is put to good use as opposed to spent frivolously

You could also make one extra lump sum payment at the beginning of each year, perhaps after receiving your year-end bonus.

So let’s say you make a $1,000 bonus payment each year in January, starting in month 13.

That would save you $19,005.22 in interest and shave 85 months (just over 7 years) off your loan term.

Now that 30-year fixed mortgage rates are closer to 6%, the math might look a little different.

For example, making one extra payment each year might shave about five years off a 30-year loan term, while two extra payments made a year could take nearly 10 years off your term.

In other words, if you make two extra mortgage payments annually instead of just one, you could reduce your 30-year loan term down to about 20 years.

But you can easily determine this yourself using an early payoff calculator, as previously noted.

To sum it up, there are all types of scenarios that abound here, and which one you choose, if any, is up to you.

You might argue that mortgage rates are super cheap, and thus determine that making extra payments now makes little financial sense.

Or you could be living in your dream home and not too far from retirement, with the hopes of living “free and clear” sooner rather than later.

If that’s the case, making the extra payments now may be very appealing. Refinancing your mortgage to a shorter term could also make a lot of sense.

Just remember that plans (always) change; homeowners are much more likely to move or refinance their loans as opposed to carrying them to term.

So while the math might excite you, it may not actually pan out.

How to Pay Extra on Your Mortgage

If you’re looking to pay extra principal on your mortgage, it’s fairly straightforward. Though there are a few things to take note of to ensure it gets processed correctly.

After all, the last thing you want is a missed or late mortgage payment when attempting to save some money.

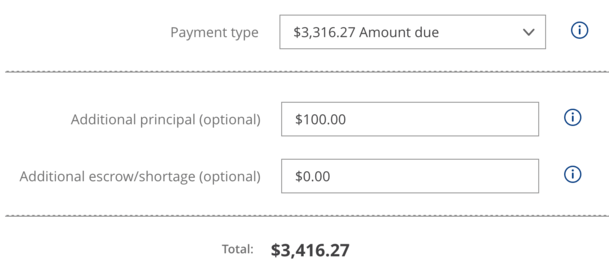

When you go online to make your regular mortgage payment, you should see a section labeled “Additional Payments” or “Additional Principal.”

In this section, you can input any number you’d like beyond the minimum amount due, which is your regular mortgage payment.

For example, if your payment is $3,316.27 per month, you can allocate additional principal with your payment, say $100.00.

This would make your grand total $3,416.27, with the extra amount going toward paying down your loan balance ahead of schedule.

It would save you interest over the rest of the loan term, but it wouldn’t lower future payments. Any remaining payments would still be $3,316.27 per month.

Also note that you might see the option to pay extra toward your escrow account, assuming there’s a shortfall or an expected one. This has nothing to do with paying your loan down faster.

For those paying by phone, explain to the representative exactly what you’re trying to accomplish, with any overage going toward the principal balance.

And if you happen to be paying by mail, there might be a section on the payment coupon regarding additional principal. Simply write in the amount you want allocated.

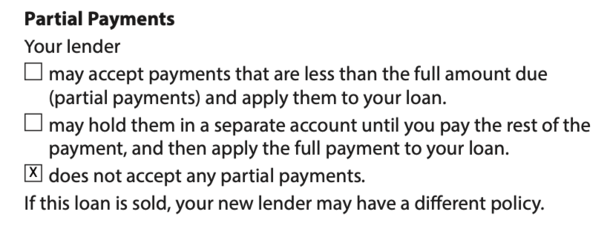

What About Partial Mortgage Payments?

An option to make a partial payment could also be listed on your loan documents and/or your loan servicer’s payment page, but this differs from paying extra.

Typically, this option is for those who are behind on their mortgage and looking to catch up.

And it often results in the money being held aside until enough for a full payment is allocated.

For example, if you make a $1,000 partial payment it might be put in a “suspense account” until the remaining $2,316.27 is sent (using our same payment example from above).

In some cases, the money could simply be returned to you if it’s not the full amount due.

I suppose it could also be utilized for biweekly payments, assuming the servicer accepts that arrangement.

The key here is to ensure you make at least the minimum payment before paying any extra. And verifying that it’s allocated correctly.

If you’re not sure, it might be best to contact your loan servicer directly to confirm payments are made as expected.

Even if you are “sure,” it could be helpful to verify with the servicer before paying any amount other than the amount due.

Read more: Should you pay off the mortgage early?

- Just When You Thought 7% Mortgage Rates Were Off the Table - July 8, 2026

- Light Week for Economic Data Means Flat Mortgage Rates Likely - July 6, 2026

- Soft Jobs Report Takes Pressure Off Mortgage Rates - July 2, 2026