If you ask most people, they’ll probably say you should save up a good chunk of money before buying a home, possibly even 20% of the purchase price.

A mortgage underwriter might share similar sentiment, even if their very own loan programs allow for low or even zero down payments.

The general thinking is that someone who puts down more money has skin in the game, and is therefore a lower default risk.

They won’t want to miss their mortgage payments and in the process lose their home, the equity they’ve accrued, and the down payment they plunked down with it.

But a new study from the JPMorgan Chase and Co. Institute reveals that liquidity appears to be more important than equity, income, or payment burden.

Money in the Bank More Important Than Down Payment

- If you put a large amount down when buying a home

- Be sure not to overlook the many closing costs involved

- While the monthly payment will be cheaper if you put more down

- You might not have a lot set aside if things go wrong

When you purchase a home, it comes with lots of closing costs, ranging from appraisal and inspection fees, title and escrow charges, lender fees, moving fees, new furniture, renovations, and so on.

It can be quite the financial hit, which explains why mortgage lenders often require asset reserves to ensure you can make your mortgage payments for a few months if money gets tight.

Those who put down say 20% or more might feel an even bigger pinch, once you factor in those other costs mentioned.

For example, someone buying a $500,000 home would have to fork over $100,000 from their bank account, along with thousands more in upfront closing costs.

Then you’ve got the moving costs, the renovations, the new couch and big screen TV, the monthly utility bills, and last of all the higher housing payment via your new mortgage, which includes taxes and insurance.

Someone who purchases that same $500,000 home with just 3% down would only have to come to the table with $15,000 plus the closing costs and other expenses mentioned.

That’s a stark difference in terms of having an emergency fund if things go sideways.

The downside for the low down payment mortgage borrower is their monthly payment will be higher.

As I’ve said before, there are three things that can raise your mortgage payment if you put down less than 20%.

They include mortgage insurance, a higher mortgage rate thanks to additional pricing adjustments, and a larger loan amount.

But in many cases, the monthly payment difference might not be all that significant in the grand scheme of things.

And for many folks, a slightly larger monthly payment may not be a deal breaker.

It is often the lack of savings that seems to be the biggest problem for Americans. So giving it all away to the bank on day one could lead to trouble.

When It Comes to Mortgage Default, Liquidity Is King

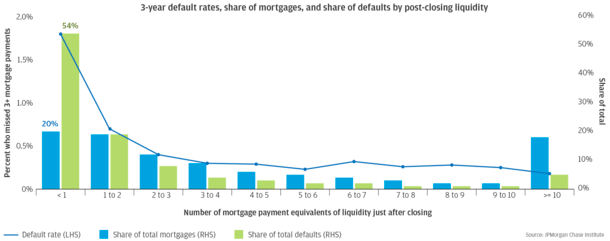

Now back to that study from Chase, which was authored by Diana Farrell, Kanav Bhagat, and Chen Zhao.

The trio found that borrowers who had little set aside post-closing defaulted at a “considerably higher rate” versus borrowers who had the equivalent of at least three monthly mortgage payments in the bank.

Specifically, those with less than one month of reserves defaulted at a rate of 1.8%, six times higher (0.3%) than the borrowers with between three and four months’ reserves.

They also discovered that homeowners with low liquidity but more equity defaulted at “considerably higher rates” than those with more liquidity but less equity.

And payment default was often the result of a loss of liquidity, regardless of the borrower’s home equity position, income, or payment burden.

The group also noted that loan modifications resulting in increased borrower liquidity reduced default rates, whereas mods that simply increased borrower equity (but left them underwater) didn’t impact default rates.

An Emergency Mortgage Reserve

- Instead of exhausting all of your liquidity when taking out a mortgage

- The authors suggested setting aside a small amount in an emergency mortgage reserve fund

- That way you’ll have a few months covered if you run into trouble

- It could allow you to get back on your feet and avoid default

So what does it all mean? Well, the authors have suggested an interesting pilot program where borrowers could put a little less money down and send the residual cash to a so-called “emergency mortgage reserve.”

They argue that the existence of such a fund could produce lower default rates, and even serve as an alternative to measuring a borrower’s ability-to-repay using their total debt-to-income ratio (DTI).

Whether that happens or not, it brings up a good point for those grappling with what to put down on a house.

Ultimately, you’ve got a lot of choices these days, ranging from zero down in some cases to 3-3.5% to 20% down or more.

While lenders do often require borrowers to show that they have a couple months of reserves (PITI) in bank, you could well use that money to buy a couch (or anything else) after closing.

And if you parted with much or all of your hard-earned savings, it could be very easy to get into trouble quickly.

Even if your mortgage payment is higher, there is an argument to put down less in certain situations if it’ll mean you’re protected in the event your finances take a hit.

Sure, you could make the point that someone shouldn’t be a homeowner to begin with if they can’t manage 20%, or at worst 10% down, but reality is a lot different.

Last year, I noted that nearly half of home purchase mortgages were considered “low down payment,” defined as a down payment below 10%.

My guess is this isn’t going to change anytime soon, especially as home prices continue to rise.

If you’re unsure of what to put down, do the math and determine how much you’ll have leftover when all is said and done.

Even if the bank only requires you to have a couple months’ reserves, it might be prudent to come up with a down payment that leaves a little bit extra in the event you hit a snag.