If you have a mortgage, you’ve undoubtedly had some company urge you to refinance, especially right now with mortgage rates being as low as they are.

And hey, the bank or lender probably has a point if you received your loan several years ago because the interest rate is likely much higher.

But for some reason, many homeowners don’t refinance despite the seemingly obvious benefit of a lower monthly mortgage payment.

Interestingly, many borrowers with what would be considered “high” interest rates don’t refinance. So why would someone with a 5% mortgage rate not take advantage of a 3.5% 30-year fixed rate?

Well, because maybe they can’t.

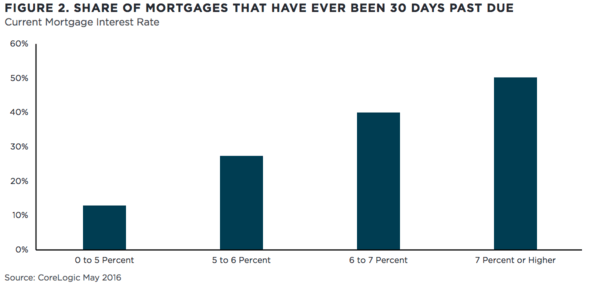

If You Have a High Mortgage Rate, You’ve Probably Been Late

- CoreLogic found that those who don’t refinance

- Often missed a mortgage payment at some point

- Which would explain why they didn’t bother

- Since it’s very difficult to get approved with late payments

An analysis performed by CoreLogic revealed that some 23% of mortgages had interest rates above 5% as of the end of May, which would appear “ripe for refinancing.”

Seeing that the 30-year fixed is averaging close to 3.5% at the moment, these mortgages should generally be “in the money,” that is to say, where it makes financial sense to refinance.

This appeared to be a perplexing situation so they drilled down some more to determine what was holding these homeowners back.

It turns out many higher-rate mortgages are either seriously delinquent, or have been 30-days past due at some point. Both of these situations make it difficult, if not impossible, to refinance.

If you look at the chart above, you’ll notice a correlation between being late and owning a high-rate mortgage.

I’ve always felt it to be ironic that borrowers more likely to fall behind on payments are stuck with higher interest rates, thereby increasing their chances of slipping up. But that’s risk-based pricing for you…

As you can see, those with the highest rates are also the likeliest to have missed a mortgage payment here and there.

The same goes for seriously delinquent mortgages, which though not pictured, shows a near identical chart.

But it’s not just late payments that are holding back borrowers from refinancing.

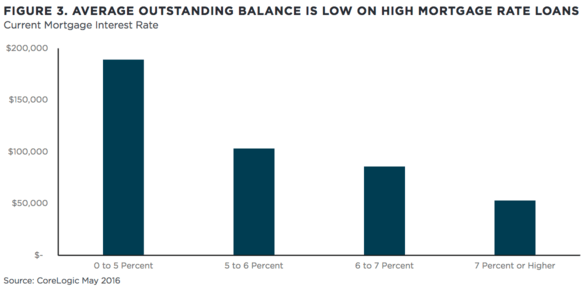

The Remaining Mortgage Balance Might Be Too Small

- Another common issue

- Is that their remaining loan balance is too small

- To justify a refinance

- Even if the new interest rate could be a lot lower

After removing the “ever-30” crowd from the mix and also loans that are in private-label securities, and thus not eligible for a HARP refinance, the 5%+ interest rate group drops to 13% of all outstanding mortgages.

However, this relatively large group of homeowners only accounts for seven percent of the unpaid principal balance of all those mortgages.

And it is for this other reason that these mortgages often aren’t refinanced, even if they can obtain a significantly lower rate.

Like that other chart, there’s a strong correlation between interest rate and loan balance. In short, those with the highest interest rates tend to have the smallest loan balances.

In fact, the average balance was just $53,000 for those with mortgage rates of 7% or higher.

That gives them much less incentive to refinance, and also explains why they’d held onto those higher rates for as long as they have.

Read more: 18 reasons to refinance your mortgage.

(photo: Véronique Debord-Lazaro)

Colin,

You and many other leave out a large contingent of people who cant refi….who were never HARP eligible.My loan while serviced by Ocwen is owned by Deutsche-Bank. Since it is not owned by Fannie/Freddie it was never eligible…Any loan serviced by a US banking institution by the time HARP 2 came around should have been included….they have not been nor will they. You don’t even mention this, and it effects your chart greatly.