Mortgage Q&A: “Pre-Qualification vs. Pre-Approval”

When you initially set out to purchase a new home, the real estate agent(s) and home seller will want to know you can actually afford the thing. Heck, you should want to know too.

After all, if you can’t afford to buy it, you’ll be wasting everyone’s time, including your own. Aside from affordability concerns, you may find other issues that disqualify you from obtaining a mortgage (do I qualify for a mortgage?).

And these issues aren’t always obvious, especially to the first-time home buyer who has never obtained a home loan before.

You might think you’re good to go, but because of the nuanced and ever-changing mortgage landscape, it’s better to know for sure.

You Won’t Get Very Far Without a Mortgage Pre-Approval…

As noted, real estate agents and home sellers will want to be certain that you’re committed to buying a home, as opposed to those just casually browsing, so they don’t miss out on a legitimate buyer in the process.

After all, if it’s between you and another qualified buyer, and they pick you, without knowing you can obtain a mortgage, it’ll be a tough sell to go back to that other buyer after the fact.

They’ll lose a lot of leverage, assuming that other buyer sticks even around.

For these reasons, most real estate agents will demand that you get pre-approved for a mortgage loan before they even begin showing you potential properties.

Additionally, most agents have a preferred mortgage contact they’ll likely refer to you to get the ball rolling.

Tip: You can use this contact for your pre-qualification and pre-approval needs, but don’t forget to shop around with other banks and brokers as well to ensure you obtain the lowest mortgage rate possible!

There’s absolutely no obligation to use the broker, bank, or lender that provided the pre-approval.

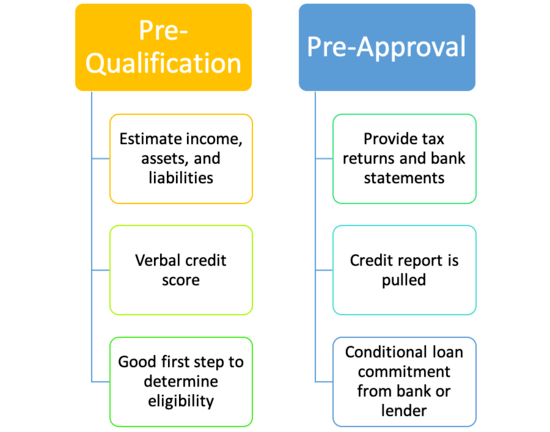

What Is a Mortgage Pre-Qualification?

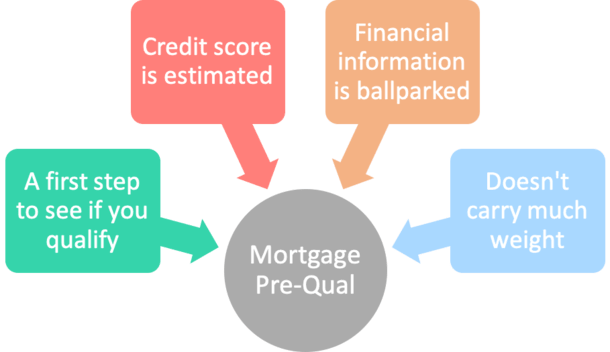

- A quick check to see if you qualify for a mortgage

- It doesn’t require a credit pull (just an estimated credit score)

- Nor any verified information such as tax documents or bank statements

- It’s simply a first-step to get the ball rolling to see what you can afford

If you choose to finance the home purchase with a mortgage, as opposed to cash, you’ll likely need to get pre-qualified first.

A “pre-qualification” isn’t as robust as a pre-approval, but it’s a good first step to ensure you can purchase the home you desire (or any one at all).

It’s a pretty straightforward, simple check to see what you can afford based on your income/debt levels (debt-to-income ratio), assets, down payment, employment history, perceived credit score, and so on.

[What credit score do I need to get a mortgage?]

You can get pre-qualified very quickly and easily with a bank or mortgage broker, but it won’t carry much weight in the eyes of the agent or the seller.

After all, with a pre-qualification you’re simply supplying estimates of how much you make, or what’s in your savings account, and your credit report may not even be pulled to avoid the hard inquiry.

You should pull your own credit report via a free website like Credit Karma before you even speak to a mortgage lender so you know where you stand. Doing so won’t count against you, whereas a lender-initiated credit report will.

In short, a pre-qualification, or pre-qual as its known in the industry, is just a quick determination of what you’d likely qualify for if you made an offer and applied for a home loan.

It’s not necessarily a waste of time, but it’s not going to get you very far. You can liken it to running a few numbers to see where you stand, but it cannot be used in place of a pre-approval.

However, it might uncover some issues that will need to be addressed before you can be approved for a mortgage, so it’s certainly something to consider as you learn more about the process.

While you’re at it, consider running the numbers through some mortgage calculators, such as my mortgage payment calculator and mortgage affordability calculator.

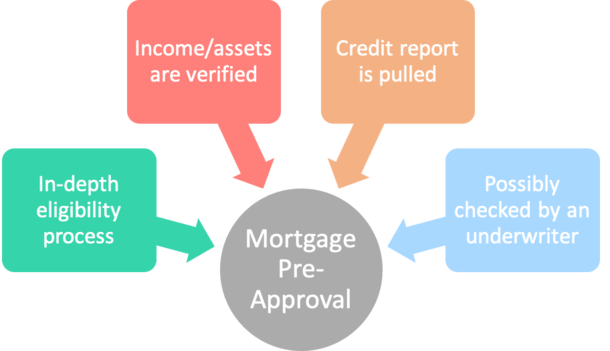

What Is a Mortgage Pre-Approval?

- A more official process to see if you qualify for a mortgage

- It requires a credit check from the lender (they’ll pull your credit report)

- And a real review of financial documents (bank statements/W-2s/tax returns)

- Possibly an automated underwrite as well or even a glance from a human underwriter

A mortgage pre-approval, on the other hand, actually has legs. It’s a written, conditional commitment from a bank or mortgage lender that says you are pre-approved for the mortgage financing in question.

It comes only after filling out a loan application, supplying verified income, asset, and employment documentation (assuming these items are necessary), running credit, and underwriting the loan file based on current mortgage rates.

When mortgage lenders verify these things, they can actually calculate minimum credit card payments, student loans, and other debt obligations against your income to figure out your DTI and subsequently what you can afford.

Aside from being way more accurate, furnishing a pre-approval letter shows the interested parties (sellers, agents) that you’re a committed home buyer, boosting your chances of sealing the deal at the price you want.

Getting preapproved will also show you how much house you can afford, not just a flimsy estimate. This is important for you as well to ensure you don’t get in over your head.

Mortgage Pre-Approval Requirements:

- Credit report (to verify credit history and scores)

- Bank statements (to verify assets for down payment, closing costs, reserves)

- Pay stubs (to verify income and recent employment)

- Tax returns (to verify employment history and income over time)

How Long Is a Mortgage Pre-Approval Good For?

- A mortgage pre-approval is generally good for 60-90 days

- But there’s no guarantee depending on what transpires during that time

- It’s just a conditional approval based on the information in the file

- So if anything material happens, your approval status may also change

Once you provide all the required documentation and get the mortgage pre-approval letter from a bank or lender, it is typically valid for 60-90 days.

Just note that a lot of things can change during that time, such as your credit score, so it’s not 100% guaranteed.

Again, a pre-approval is not a guarantee that you will be approved for a mortgage. Otherwise it would just be an outright approval.

And even a mortgage approval is still conditional on you meeting a series of requirements set forth by the lender.

If things do change dramatically, or even a little bit, it won’t matter if the pre-approval is just a few days old, as material changes can affect the outcome of your approval.

For example, if your credit score falls below a key threshold, like from 620 to 618, you could be denied after getting your pre-approval letter. It’s not the bank’s fault either, it’s just an unfortunate turn of events.

Same goes for anything the underwriter sniffs out during the approval process. They get a lot more involved and may find things that were initially missed, such as a late payment or a credit card or personal loan you didn’t disclose.

When it comes down to it, an approval is never a sure thing until the mortgage is funded and closed!

As you can see, being pre-approved and pre-qualified are not the same thing, so make sure you know the difference before shopping for a home.

Do You Need a Mortgage Pre-Approval Letter to Make an Offer on a Home?

- In a hot real estate market it’s generally a necessity to have a mortgage pre-approval in hand

- While highly recommended, it’s not an outright requirement

- And it may not be necessary in colder real estate markets

- But it’s still important to know where you stand regardless of the seller’s stance

At the end of the day, you don’t necessarily NEED a pre-approval letter to make an offer on a piece of property.

But nowadays, with so few properties on the market, and so many multiple-bid situations, it’s often a requirement just to hear back from the seller’s agent.

Sure, you can tell your real estate agent to tell the listing agent that you’ve got an 800 credit score, $1 million in the bank, and a job that pays you $500,000 a year. And they might say fine, skip the pre-approval.

But chances are that’s not your financial profile, so just to play ball and keep everyone happy, it often makes sense to get the pre-approval done. It will also strengthen your offer. And you might learn or catch something along the way.

As I alluded to earlier in this post, it’s good to know where you stand as well. You might think you’re a sure shot at getting a mortgage, but surprises aren’t all that uncommon and mortgage underwriting guidelines change all the time.

So a pre-approval could actually save you time and money, despite being a task that needs to be taken care of upfront. It shouldn’t take very much work to get one anyway.

There are brokers and lenders that can get you one the same day, or even within a few hours, thanks to new technologies that are able to automatically verify things like your credit scores, employment, income, and assets.

Just remember not to feel obligated to use the bank that furnishes the pre-approval letter for you! It’s entirely possible to go elsewhere, and even use the letter to get a better offer from a different lender.

Can You Get Pre-Approved for a Mortgage Online?

Absolutely. This is actually the most common way to get pre-approved these days, thanks to newer technology.

Most banks, lenders, and mortgage brokers have the software in place to get you pre-approved on your own.

All they really need is some basic information about you and the property (if you’ve already found it), along with your employment history, income, and assets.

They may also request authorization to pull a credit report, while others may allow you to simply estimate your creditworthiness (e.g. excellent, good, bad).

Some will even let you generate pre-approval letters on the fly if and when you’re house shopping.

The savviest of lenders allow you to personalize these letters with the property address you’ve got your eye on to really make them stand out to home sellers.

Tip: If you don’t want the pre-approval to “hurt your credit,” make sure the company in question only does a soft pull of your credit report.

These types of inquiries allow lenders to see your credit scores and history without it counting against you as a formal application for credit.

Can You Get Pre-Approved for a Mortgage From More Than One Bank?

Sure. There’s no limit to how many pre-approvals you gather, though it can take time and may hurt your credit if these companies are also doing “hard pulls” of your credit report.

The only real case where I’d see the benefit or purpose of multiple pre-approvals is if you got one on your own, then got one from a referral or preferred lender.

For example, you may have gotten pre-approved from your bank or a lender you found on your own, then once your real estate agent got involved, suggested you also get approved with their person/company.

Again, it’s not a negative by any means, as long as your credit isn’t dinged in the process.

But as noted, it takes some time and legwork, so you may get annoyed filling out similar forms more than once.

You can still shop around without getting the pre-approval. It’s perfectly fine to just ask for mortgage quotes without all the form filling.

And when all is said and done, you’ll likely only apply with one company.

Can You Get Pre-Approved for a Mortgage Without a Job? Or With Bad Credit?

Similar to wondering if you can get approved for a mortgage without a job or bad credit, folks are often curious if you can get pre-approved with these shortcomings.

Ultimately, it depends on the situation. There are some lenders that are okay with an applicant with lots of assets, even if they lack an income.

So if you don’t have a job, but have a ton of money in the bank, you might still be able to get approved. But you need to have a good deal of assets.

With regard to credit, it depends how bad your credit scores are. Some consider bad to be a 650 credit score, while others might think bad is 500.

If it’s the latter, you could have serious trouble securing a home loan. But if it’s in the low-600 realm, or even high-500s, you could still get pre-approved and eventually approved for a mortgage.

Both of these circumstances illustrate the importance of getting pre-approved so you don’t leave anything to chance, or find out the bad news at the eleventh hour!

Next Step After Mortgage Pre-Approval

- Either formally apply for a home loan with the lender who pre-approved you

- Or apply for a mortgage elsewhere if you find someone else you’d like to work with

- You aren’t obligated to use the lender who supplied the pre-approval letter

- Still put in the time to comparison shop to ensure you get a good deal

The next step after receiving a mortgage pre-approval is to either apply with the lender who provided it or apply for the loan elsewhere. You can certainly shop around and decide which company is the best fit.

In fact, you can even use the pre-approval quote as leverage to get a better mortgage rate (and/or lower closing costs) with a different lender. Remember, you can use any company you wish, regardless of what your real estate agent tells you!

Once you’ve selected a lender, you’ll need to sign disclosures and express your intent to proceed with the loan application.

The lender will then begin collecting paperwork and signatures, including the purchase contract, in order to process the loan.

It will eventually land on an underwriter’s desk for full approval, at which point a list of conditions will be generated (if applicable) in order to draw docs and fund the loan.

You will also be given an opportunity to lock your loan early on so the interest rate you are quoted won’t change.

If you think interest rates may improve in the interim, it’s perfectly acceptable to float your rate as well. Be sure to consult with your loan officer or mortgage broker if you need direction.

To summarize, the difference between a mortgage pre-qualification letter and a mortgage pre-approval letter (for you lazy readers):

Mortgage Pre-Qualification:

- First step, less involved

- Based mostly on estimates

- Doesn’t require a credit pull

- Carries less weight/ not a sure thing

- Not taken very seriously

Mortgage Pre-Approval:

- Based on verified information

- Requires a credit pull

- Must be underwritten (manual or automated)

- Written conditional commitment from a lender

- Shows home sellers/real estate agents you’re serious

I am a 50 yr old woman who is coming out of a 30 yr marriage, I have a part time job that guarantees me 28-30 hours per week, I have had this one and only job, 14 months.

Can you recommend any low income/first time home buyers programs in the Central Georgia area for me ?.

I have good credit, low debt ( no current car or home loan or rent), and approximately 10 % down for a $55,000 ( or lower )

for a home.

Please point me in the right direction?

Hi Katherine,

I am not familiar with loan programs in the state of Georgia, but perhaps contacting a local HUD-approved housing counselor might be a good starting point. Or the Georgia Department of Community Affairs. The lack of employment history could be a problem, but the more time that goes by the less that’ll be a concern. Good luck!

Colin,

I have put in a loan application for a home it was pre-approved for 120,000, changed to 95,000 and now 60,000. I had a bankruptcy and divorce in 2011. I only have school loans, but I was told that they had to rerun my credit again in my maiden name. Is it not the practice of lenders to run loans by social security #s. In addition, they indicated that my bankruptcy was contested by some creditors. It was not the case, I asked them to send me the source they were getting the information from because this was puzzling, they indicated from my credit report. Which they highlighted the information as the consumer disputes this account. I am not sure what is occurring, I may be a risk to them. I started this application process on Feb. 17th, they gave me 3 pre-approval letters but the realtor indicated that it is not the correct type of notice. What do I do?

Hi Veronica,

If the 3 pre-approval letters are from three different lenders you may have a problem. If they’re all from one lender you may want to shop around a bit more and/or determine what’s going with your credit and try to clean it up before reapplying to avoid the same result over and over again.

I have a question? If your pre approve for a certain amount on a new construction loan but before you sign any document you decide you want to add upgrades can the amount on the loan be change. example if the house is $240,000 but the upgrade will bump it up too $260,000?

Sara,

If a bank says you’re pre-approved to buy a $240k home, it generally means it’s conditional upon the home actually selling for $240k. If it turns out to be $260k, you may need to get another pre-approval for that amount, assuming a pre-approval is required. Or just hope you can get a larger mortgage based on your borrower profile.

Hi. I am just beginning the ‘Gee, I think it’s time to stop renting and buy a place’ process and research. My quesiton is about pre-qualification. I understand that it’s only to get a rough estimate about how much you can afford. But it also feels like the best place for me to start as I don’t know what amount of house I can afford ($150k?, $250k?, $350k) is a pre-qualification. But, I don’t know what number I should put into the loan amount field. Shouild I put a number on the higher end ($350k+) to see what the most is I can qualify for? Or should I put in a smaller number so that my pre-qualification doesn’t get a thumbs down? If it helps, I’m single, make about $90k per year, have no debts and could have about $40k or $50k to put down in about a year. Thanks.

Hey Mary,

You can simply ask a bank or broker to determine how much you can borrow based on your income, debt, assets, etc without putting in a loan amount. But if you do they shouldn’t give you a thumbs down, they’ll just tell you that you can only get a loan size of X if you overshoot it.

How long does getting pre qualified take?

Michael,

It depends on the broker/lender…could take a few hours, a day or a few days.

my husband and I were pre-approved for a FHA loan. We made an offer it has gotten accepted and now we are awaiting the contract to be drawn. Im trying to be as optimistic as possible but im concerned that when its time to close we wont get approved for the actual loan. I believe our Pre-Approval was for around 300,000 and the offer was accepted at 197,240. Combined last year we made 90,000. Have 2 car loans but no other debt. I guess im just looking for peace of mind that this will not get pulled out from under us at the last minute. Any reasons as to why it should, and should I be worried?

Christine,

There are many reasons why loans get declined, and it’s impossible to say without the loan being underwritten. It’s certainly a stressful process, but hopefully your pre-approval was thorough and caught any potential issues. It seems to be for an amount well above what you’re actually purchasing. Good luck!

Hi Colin,

About two months ago I took out a loan,paid off all our debt, and now have a one payment for that. We decided that its also time to start the process of home ownership. We will be using the VA home loan. We looked online and a realtor got in touch with us, the man then got us in contact with a broker from a bank, who then took our ss# and DOB. told us we are proved for xxxx$. The realtor who first spoke to us, put us in contact with a different realtor who just showed us a house tonight that we are interested in. He said that we can contact the bank broker that we spoke to earlier in the week and/or speak to a lender that he knows and works with. Now here is where I’m confused. (also have to mention my husband has left for duty for two wks and won’t return until 7/25) do i seek out both the broker and the lender to see who can give us the best deal and most affordable? What questions do I ask them? I’m confused as to all that I’m reading about pros and cons. they are also both familiar with VA home loans and other deals for veterans..

Hi Mr. Robertson. I want to know, if I get pre-approved now and it is not to my liking and I decide to get pre-approved next year, would it affect my credit score, with each credit check? I have a part-time job but applying to get another and I am not sure I will get approved for an amount that can get an okay place in Maryland. But I still wanted to go through the process so that I can see what I need to improve in. Please advise, thanks.

Ruth,

Pre-approvals a year apart will likely result in two unrelated credit inquiries (assuming they both pull your credit). It could ding your credit score somewhat, but the effect of inquiries diminishes over time, especially after one year. And sometimes they only lower your score a handful of points if at all. If you don’t want them to pull your credit, perhaps getting pre-qualified instead makes more sense.

Maria,

Realtors generally have preferred lenders they work with…it’s a referral network so they’ll usually always recommend that you work with “their guy or gal” instead of someone else. But you aren’t obligated to use their person. You can still shop around and compare costs and pros and cons of working with both.

My husband and I are curious to do a pre-approval, but mainly to just get an idea of what we can currently afford. Does it look ‘bad’ on credit etc. to do a pre-approval process but not actually buy a home?

We currently only have $10,000 saved for a down on a home.

Emily,

You can check your own credit (without the inquiry/ding) and provide your scores to a potential lender to get a good idea of what you can afford/qualify for without the lender actually running your credit themselves.

What kind of information are underwriters looking for? I have heard that they “dig deep”. I am not sure what this means but I do know that I have had credit issues in the past that have been resolved. Will I have to attempt to contact past creditors (over 10 yrs old for example) to obtain proof that the debt was satisfied. I have no debt other than school loans. Make $31,000 a year and have around $10,000 so far toward a down payment. I have worked with and completed the HUD credit counseling program and at this point I am just saving for more of a down payment but am also researching prior to actually going to get a pre-qualification or pre-approval.

Hi Colin. Me and my fiancé just got pre-approved for an FHA loan for 200K last month. We have been looking but are leaning more and more towards a new house but the houses are just out of reach being at $219 and up. We have about 10K saved for a down payment. I was told that if in 6 months we don’t find anything we have to be pre-approved again? Here is says the loan amount is good for 30-90 days. I am confused on which is more accurate. Also do you think since I just got a raise and my fiancé just did, will that increase the loan amount if we need to get pre-approved again? We have good credit, well over 700s. Thanks.

Cristal,

Pre-approvals “expire” after a few months because things change, so lenders can’t just assume your situation is exactly the same for months. Raises are great but lenders like to look back at your income over the past couple years to determine affordability. If you have costly monthly liabilities that can be paid down, like loans and credit cards, that might be one way to lower your DTI and increase what you can afford in the way of a mortgage payment. But paying down existing stuff will obviously reduce your cash on hand, though the raise could help minimize that. Good luck!

Hi Colin,

I’ve been casually looking at listings for condos on the West side of Chicago in the $285-300K range. I’m a first time buyer, so I’m a little apprehensive about starting the pre-approval process until I’m sure of what to expect. I think I’m in a good position to qualify for a mortgage, I’m just not sure whether a bank will lend me enough for the price range I’m looking at. Here is my situation: 800 credit score, stable work history, no debt, $55K/yr salary, $15-20K for a down payment. The majority of the mortgage calculators I’ve used say I’d qualify for a mortgage well short of the amount I’d need for my stated price range (~$280K).

Are the calculators right, or do you think a bank would pre-approve me for the price range I’m looking at?

I appreciate the advice, thank you.

Practical commentary . I learned a lot from the information ! Does anyone know if my company would be able to obtain a blank a form version to fill out ?

Hi Colin,

My wife and I are preapproved for a home loan in Florida and we started placing bids and our finance agent told us that we have to work in Florida at least 30 days before we can actually get the home. We currently live in SC and moving down without a home is out of the question and we don’t want to waste the money of sec deposit, first months rent, cutting on utilities etc. is there any way at all around this? Both my wife and I work in the service industry and we are both getting transfers to the Orlando area from our franchise restaurant jobs that we currently work for (two different companies). We have a lot more than 30 days history at these jobs and we will be doing the same job when we move down, please help us understand

Daniel,

I haven’t heard of having to live in X state for 30 days to get approved. So long as the job is in the same industry/line of work and is stable, it shouldn’t be a roadblock…how else would people relocate and own homes? And why would 30 days make any difference at all?

I live in Texas and I recently took the first time home buyers education class so I can learn about the home buying process and I qualify for down payment assistants through my county. My question is does the down payment assistants lower the cost of the mortgage pre month or what exactly does it go towards?

Hi Colin,

My husband and I are wanting to buy our first home and really don’t know where to start. He is an OTR trucker so far this year he’s brought in around $30,000 and is currently buying his truck and we have a car payment. I bring home about $630 a month. Our credit is not the best, his is at about 572 right now and mine is 604. Do you think that we could get a loan with those scores or no?

Charisse,

It would lower what you need to put down on the home. So if you needed to put down $20k, and it provided $10k, you’d only need $10k of your own money for down payment.

April,

While it may be possible, you might be better off working on your credit for a bit longer to get the scores above 620 at minimum, and ideally even higher to get more favorable mortgage rates and more loan options. Good luck!

Hi Colin,

I was pre-approved for a conventional, but portfolio loan. I think the portfolio, specific to my bank, is relevant because of new student loan laws in place as of 03/31 of this year, which says that 10% of student loan amount be applied to your debt/income ratio, rather than the actual payment- a problem for most of us with student loans. This loan uses my actual payment.

I found a home and supplied the P&S to bank for full mortgage application.

My concern is that rather than asking for current and even last year’s contracts (I am a teacher-new career to me), the bank wants 2 years of W2s. This reflects a year of grad school and unpaid internship (2014) and only half a year of my last contract (2015-16 school year) and it does not even consider my current contract(2016-17), which includes a raise in salary, small as it is.

Do you think this is a problem or is the prequal a decent indicator of mortgage outcome?

Thank you,

Lauri

Lauri,

If they did a proper pre-approval using everything you wrote here and said you qualify it may not be an issue; they may just want that paperwork to be thorough. However, things can come up after a pre-approval so it’s never 100% guaranteed. If you’re concerned you’ll fall short because of income you may want to let them know sooner rather than later instead of just hoping it all works out. You could also shop around a bit to get some other opinions and rates/loan options while you’re at it.

I was filled out a loan application and received a phone call saying I’m eligible for pre-qualification and now have to supply two bank statements, two check stubs, two years of w2s and tax returns, and etc. They also sent me a list of do’s and dont’s. One of them says the amount in my checking account shouldn’t go below what was told to them. If it does, would this affect my chances of getting the home loan?

Marilyn,

While I can’t say with certainty, lenders basically look at a snapshot of your financials to determine eligibility. It may be the case that you need X amount in assets to qualify for the loan you were initially pre-qualified for. As a rule of thumb, if you are looking to get a mortgage it’s recommended that you not move money around if you can avoid it. It just complicates things and often requires more paperwork, though you may still be approved once you paper trail everything.

Hello Colin

I would like to know if lenders pull your credit and ask for check stubs again after being preapproved? Do lenders consider overtime as part of your income if it’s consistent? Thanks

Reginald,

Lenders generally check your credit just before closing to make sure no new obligations have been created or credit ran up during application process. Pay stubs tend to be good for X amount of days before new ones might be required. Overtime income may be used if consistent (been receiving past 12 months+) and expected to continue for foreseeable future.

The lender that I am talking to is telling me that pre-qualification and pre-approval are the same thing. Everything I have read says that it is not. why is this lender telling that it is? Do you have to go through pre-qualification before getting pre-approved?

Natalia,

Maybe they’re just getting caught up in semantics…or trying to keep things simple for you. You don’t have to do one to get the other. As noted, the pre-approval is more robust and holds weight while the pre-qual is more of a rough estimate.

My Boyfriend and I are in the process of a preapproval, he is better versed in this but I am trying to get a better understanding…. if the mortgage broker has taken everything from us to see what we are approved for, will he return with the highest amount we are approved for ? Or for example if we mentioned we were looking spend around 250k on a house, is he looking to get approved at that amount?

Veronica,

Should come back with the highest amount so when you shop you know if you can stretch to fit your budget.

HI Colin. Thanks for this informative article. Here’s my situation. I’m originally from India. Now a US citizen, I’ve been here in the states for 7 years but I never applied for a credit card. Both by husband and I work. But we don’t have any other debts. We pay our regular bills from our bank account. Also neither of us have credit cards or loans. I think in trying to be safe we ended up being too safe and now I don’t have a credit score. Or at least I think I don’t. I can’t obtain my credit score online for some reason and have to mail my personal documents. My address has funky characters so I can never apply for a CC online because it’s not in the right format. Anyway, by next summer we can put a down payment of $40,000. We want to be able to buy something upto 300k. Does that make any difference in being pre-approved ? What can we do to remedy the lack of credit score. Where do I begin?

Anita,

Normally you would have other loans and credit cards to establish your credit history and with it a score. Fannie Mae just made it easier to qualify without traditional credit, but lenders still have to go with their guidelines, which some may be wary to do (and for good reason if they don’t know much about your credit). Generally they want two years of history on those lines of credit to see your payment history, so it might be tough to do that before you buy. Importantly, you want to be able to document your housing history and ideally some alternative forms of credit such as utility bills, cell phone, etc. to show you’re a good borrower. May want to speak with some brokers or lenders now to see what hurdles you might encounter next year.

I was pre-approved for an FHA loan from a specific lender. my credit I have rebuilt with much attention over the past 4 years. once I get the house in mind to make an offer, what (if any) will they look at to get the actual approval? when I was “pre-approved” they just ran credit, verified income, and verified employment. Do I have to disclose ALL checking/savings accounts I use? I have 4 and 2 of them I don’t actively use, just more of a rainy day fund. I have a few times accidentally paid online bills with them and didn’t realize they went negative. will they look at that, or only the checking account(s) bulk of my check is deposited in?

Nick,

General rule of thumb is to disclose account(s) where reserves and/or down payment are coming from. Basically what’s needed for approval.

I got a approval for a mortgage and can’t get them to return any of my phone calls found a great house and want to put the offer in but if they won’t return my calls should I chance it?

Karen,

Might want to seek out a different lender if they aren’t responsive and time is of the essence.

Hi Colin,

I just got my discharge letter from my bankruptcy. My husband and I get okay income but our lender said I can’t be on the loan. How can we use my income to get a higher loan amount or how can we include my income?

Hi Colin, I used finger hut store credit line and a small personal loan to build my credit up when paid them both off not missing one payment, then I applied for the finger hut revolving credit card, which they offered me. and my credit went from my 643 to 558, it came down 85 points. Also I am self employed cleaner. No bank account. The property we are looking to purchase is where we are living and renting now. Its a single wide mobile home (loan hard to get on single wide I heard) for $80,000.00 on close to 5 acres in NC. What are my chances of getting a mortgage? My brother in law, said he is willing to purchase with me, his credit is 550 with steady income and bank account would that help? Thanking you in advance for taking the time to read this.

Lori,

While his income may help, his credit score of 550 will likely complicate matters. You’ll have to shop around to see who offers what. However, improving your credit score (and anyone else’s who is on the loan) before you apply might make life a lot easier.

Mayra,

What they’re saying is your credit would disqualify you both for a mortgage, and income can only be included if you’re on the loan, which you apparently can’t be on because of your credit.

Sir,

You stated ( You can check your own credit (without the inquiry/ding) and provide your scores to a potential lender to get a good idea of what you can afford/qualify for without the lender actually running your credit themselves.)

I have had three lenders tell me that the scores i provided them mean absolutely nothing because they are from free sites like credit karma.

Where can i check and see the scores that the lenders see without having to pay?

Lenders check different sites so how do i know they see what i see?

Thank you,

Richard,

They just mean the scores can’t be used for a proper pre-approval, but like I said, you can get an idea of where you stand and have them provide pricing assuming the scores you get for free closely match the scores they pull. You can’t get the scores they pull unless you have them pull them for you as part of a pre-approval or application.

my question is me and my husband are looking to buy a house his credit score is 725 and mines is 630 my husband is the only one working making 700 a week we have a 15k for a down payment would we be okay to apply for a loan what are our chances to get approve??

I’m a 1st timer! Getting ready to start the pre qualifying process.

I live in NC.

I make $1,500 a month minimum. I’ve had one job for over 2 year and started another 6 months ago.

My credit score is 670

Do you think I can qualify for a mortgage home for around $130,000 to $160,000 ?

Start the process and thinking of a beautiful home that could be mine made me extremely excited, but after reading things on the Internet, it has definitely discourage me about my chances. Any feedback back would help. Thank you

Sam,

It depends on the monthly housing payment versus your monthly liabilities (car payment, credit card minimum payments, etc.). The fewer liabilities you have, the further your income will go toward a housing payment. Check out my page on DTI for more info.

Stephanie,

Probably a better chance if only he applied because your low credit score would make it harder to qualify and likely result in a higher mortgage rate. Only way to know for sure is to speak to a bank or broker or two.

I’m thinking of buying a fixer-upper home in a vacation area. I have a strong credit score and I work very steady freelance – I do fairly well but with fluctuating amounts. My work history (except for 20 years ago) is only 2 years old, after a divorce, but I have a decent income, and successfully went through a recent credit check for my $$$ rental home. Two questions: 1. Can a freelancer get pre-approved? 2. Can a freelancer get approved for a mortgage for a second home or a rental property purchase when I’m paying rent?

Rose,

Best way to know for sure is to speak with a broker/bank, etc. As long as your freelance work is steady and proven over a couple years it should be doable, but only a bank can tell you for certain.

me and my husband are thinking of buying a house. We are self employed and we did not pay ourselves enough on paper, but our company grossed $450,000 this year and $295,000 last year is there any loan we can get with no verifiable income? I can supply tax returns and bank account info. also our credit scores are 640 and 630

Stephany,

There are non-QM loans, which specialize in flexible income documentation. But you may want to get a few opinions from a mortgage broker to see if they can make your income work with a bank/lender they do business with. Or if you can file taxes for 2016 ASAP and increase your salary?

Hi Colin,

I got a pre-qualification letter from my lending bank. Your article here says that they don’t run your credit for a pre-qual, but they did with mine (I can see the credit run on my history, and they made me sign something saying I consented to having my credit run). I then received my pre-qual letter in the mail.

I got a signed and executed contract from both myself and the seller of the house I offered, after I made an offer on it. It’s now in attorney approval. However their real estate agent has informed mine that they plan on using the attorney appeal to get out of the contract (by having their attorney reject it) so they can accept another offer, since they said they don’t like my mortgage. They said something like they don’t think I can get the mortgage, even though I had the pre-qual letter where my credit was run and tax docs checked.

I don’t know what’s going on, or what any of this is, because it doesn’t seem normal. I thought I did everything right. Were they expecting me to get something else from my bank and now they want to cancel the contract? I had my credit run and had to bring my tax documents to the bank to get my letter.

I’m really angry and confused. I thought my bank gave me everything I needed. They told me in the letter I received I needed a signed and executed contract to take it a step further, but the sellers won’t even let me do that, now that they are trying to get out of the contract.

Julie,

It sounds like you got a pre-approval if they ran credit and collected financial documents. Not sure why the sellers no longer want to proceed with your offer. You may want to consult with your realtor/lawyer to look over the contract you signed to determine your options.

My lender is asking us to send a letter to widthdrawl from my preapproval? We have one late payment from September we missed it by one day for the 30 day mark. Will this hurt my chances applying another mortgage preapproval another bank? I understand the late payment affect. We found a bank That will work with us we don’t want any negative impact.

Sarah,

I doubt it, especially if other lenders already said they’d work with you. May want to get their pre-approval in order first.

My husband and I want to buy a house.

All the houses that we are looking at are from 170,000 – 190,000.

My question is what amount should we ask for when we do the “pre-approval”?

We got “pre-qualified” for 180,000, but I’m afraid to ask for too much and it will get declined.

Is there a way to see the max we could get? Or will it just tell us the most they will lend us when we apply?

I hope this makes sense.

Thank you!

Brittany,

It’s possible to get a maximum loan amount if you’re just shopping around to ensure you only look at suitable properties in your price range, but the agent/lender/broker may tell you to keep this to yourself so you don’t show your hand to a seller. After all, if they know you can afford more, your lowball offer may go nowhere.

Once you get serious about a specific property, you can revisit the pre-qual/pre-approval and modify it for a specific loan amount based on a certain property’s purchase price including what you intend to offer.

Colin,

Do you recommend setting up an initial consultation with a lender to go over finances and what we can/should do before seeking pre-approval? I have friends that went this route and were given tasks to compete financially to put them in a good position to apply for home loan. But, my brother did not go this route – he and his wife simply started the process and jumped in feet first.

Do you recommend one path or another?

Liz,

I suppose you can do either but the pros of getting the pre-qual/pre-approval first are that you know how much you can qualify for (and thus can shop accordingly) and any red flags/surprises can be dealt with in advance. If you go in feet first, sellers may not take you seriously if you don’t have a pre-approval at the ready, and you may not give yourself enough time to fix any unforeseen mistakes.

Hi Colin. My husband and I are getting ready to purchase our first home. We have zero debt (except the monthly credit card that we pay off in full every month), I’ve been with the same employer for over 9 years, my husband going on 4 years, and we have excellent credit. We have about $75K saved up, and additional assets in stocks, bonds, and retirement accounts. We applied for a pre-qual back in March, and it will expire June 18th. The problem is, we are having a difficult time finding homes in our price range in the neighborhood we desire (we need to be near a school with a special program for our son), and time is running out. We are not super-picky, but would prefer not to pay down all our cash on a “fixer”, because it’s such a seller’s market right now. We’ve conceded that we may have to wait until later in the year, but are concerned that the “hard credit inquiry” will negatively effect our mortgage rate. Any advice? Thanks.

Carmen,

Inquiries generally only move credit scores 5-10 points, and sometimes not at all. Other factors (revolving monthly debt, even if paid off by due date) may move your scores in the meantime since your scores don’t live in a vacuum. Ultimately, it shouldn’t be an issue unless for some reason your scores were on the cusp of a certain threshold, and happen to fall into that lower bucket.

Colin,

Useful Q and A’s. RE: Pre-qualification letter in AZ for FHA loan with good DTI and LTV. Over a week since we have: 1. Provided financials etc. 2. Heard anything from Broker. Yesterday he sent a text saying that he was returning from vacation. Still nothing today. We did receive our credit scores in the mail, though they reflect some dated negative information. We have a house in our sights and with our ~114K range, time is very much of the essence. I think that we need: 1. Lender process info. 2. Credit report fix. 3. New broker. A bit overwhelmed at this point..help! Thank you!

Alan,

It sounds like the broker isn’t too motivated because you’re still home shopping. They seem to get more excited once you actually make an offer. But as you said, getting your financials all in order first is very important in today’s housing market so you can make your move ASAP once you find the right house. It appears as if you know what you’re doing…cleaning up credit can certainly help with qualifying and potentially obtaining a lower rate. Good luck!

Hi, my family and I found a house recently for $248k. But we only got pre approved for $175k. That house has been on the market for 172 days. The seller’s willing to negotiate but we don’t know by how much and we don’t want to insult him by offering the price too low.. What should we do?

Natasha,

Someone once said if your offer isn’t insulting, you offered too much. That being said, $175k vs. $248k is quite a gap, so I don’t know if the sellers would be able to go down that low. May also want to explore your financing options if you really want the house to see if it’s possible to get a larger loan and/or a gift to cover more down payment. Good luck!

Hi, you say the pre qualification is less robust, but I got a pre qualification certificate with detail the include the following: is this a pre qualification or pre approval i’m confused. I have removed the personal info for security purposes.

The borrowers/buyers listed on this form have INQUIRED with our firm about financing to purchase a home and the information of income, down payment and credit report have been reviewed by the loan originator listed below. After careful review, it is the opinion of said loan originator that the borrowers/buyers should/would qualify for the terms listed below.

Date: 07/05/2017

Loan Originator’s Name:

Borrower’s/Buyer’s Name:

Loan Originator’s NMLS ID:

Subject Address: TBD, To be determined, FL 34606

Loan Originator State License #:

Purchase Price Amount: $165,000.00

Loan Originator Phone:

Loan Amount: $162,011.00

Total Monthly Payment not to exceed $1,308.92

Loan Type: FHA

Loan Originator Address:

Lourdes,

The names are often used interchangeably so it’s always tough to tell what you’ve got, but actual pre-approvals should be a lot more involved than simple pre-quals.

I am currently working with a Loan Officer who works at a mortgage company. He has basically collected everything from me and has checked my credit score. He is only telling me what I qualify for, which is a monthly mortgage, and not how much of a loan I qualify for (I.E. a $200,000 house). He tells me it does not matter how much the home costs. When I asked him for a pre-approval letter, he tells me I cannot get one because I do not know what type of house I want when I have given him prices and addresses of various homes. Can’t he just use my personal information and apply it to each home price? Or can he just use my personal information and based on that, give me an estimate of how much of a loan I can afford? I am so new to this. Please help!

Rachael,

You can ask him to add an “up to” purchase price to the pre-qual, with an associated down payment and loan type (such as conventional or FHA). It’s important to know what that $200k loan amount is based on, as you could be putting down $20k or $100k, and if that’s not specified, it’s not that clear how much you can really afford. And remember you can always shop around elsewhere to get more quotes and/or different service. Good luck!

I just wanted to say thank thank you Colin and Rachael for the string of questions and answers. I am working on getting pre approved and this has given me more knowledge so I can speak a little more intelligently when I talk to my mortgage broker.

My boyfriend and I are looking to buy a house. He got Pre-Approved for 200,000. We found a house for 230,000 so we decided to go in together. The lender we talked to and gave my information to add to his came back and said it was still only 200,000. How can that be possible with my added income??

Kendra,

That is strange – maybe he initially made a mistake and the math was off. Perhaps get a second opinion to see where they put you as well.

This might be a silly question but I’m still trying to figure everything out about this home buying process. If I submit a pre-approval application for 300,000, will my pre-approval only state if I am clear for the 300 or does it tell you the max amount I would be good for? I was originally looking for homes up to 300 but I am quite smitten with a house that is around 325. I just want to be sure that I would qualify.

Sarah,

The lender should be able to provide a max loan amount based on your financials. So if you qualify for a higher $325k

(or even more), they should make that clear as long as you provide detailed information to them to make that assessment.

Hi I’m interested in becoming a first time buyer. I have a few credit cards that got closed out. Should I do a settlement to pay those or is it best to pay it all off in full? Also if I owe student loans does that count against me as well? Or should I have those in deferment?

Celene,

Not sure what you mean by closed out (was this voluntary?) or settlement, but paying off credit cards in full instead of going on a payment plan is advisable both to keep debt down and avoid any credit score dings. Sometimes those payment plans can adversely affect your credit. As for your student loans, you may want to consult a loan officer or mortgage broker to determine your monthly payment now vs. what it would be if deferred to determine best approach.