Today was a rough day for mortgage rates as the market digested the Fed’s latest outlook, which confirmed its inflation fight is far from over.

While they didn’t raise their own fed funds rate yesterday, they did leave the door open for another hike in the future, assuming economic data warrants it.

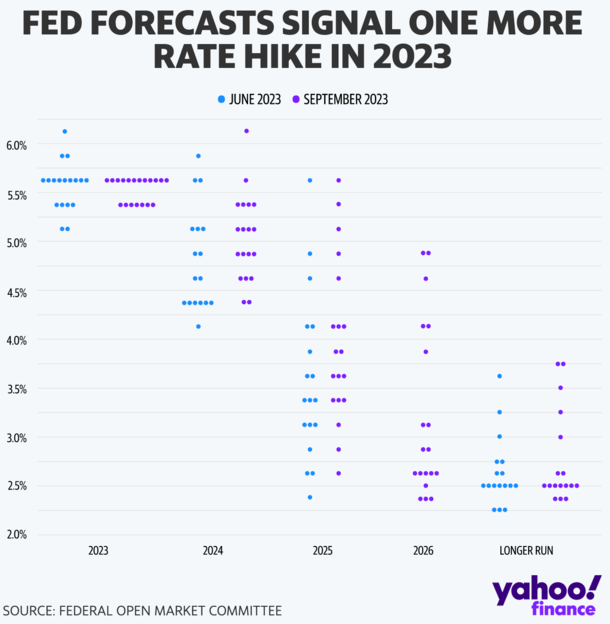

Their overall stance actually didn’t change, but their so-called “dot plot” revealed that more of the Federal Reserve’s policymakers expect another rate hike this year.

Granted, it appears only one more quarter percent (0.25%) hike is in the cards at this juncture.

So while we might be going higher, it might only be a tiny bit higher. And after that, there may be more certainty for mortgage rates.

Higher Mortgage Rates for Longer, However…

After the Fed’s announcement, everyone seemed to adopt a simple takeaway: “higher for longer.”

In other words, most don’t expect the Fed to pivot and begin loosening monetary policy anytime soon.

There had been some hope that we were at the terminal rate, where the Fed stops hiking. But maybe not just yet.

As it stands, the Fed has raised their own fed funds rate 11 times since early 2022, and mortgage rates have risen along with those hikes.

While the Fed doesn’t control mortgage rates, its policy decisions can affect the direction of long-term interest rates, such as those tied to 30-year fixed mortgages.

Simply put, they don’t set the rate on your 30-year fixed, but what they say or do can push rates higher or lower.

Of course, their decisions are rooted in economic data, so it’s really the economy that’s dictating the direction of mortgage rates.

Anyway, some market watchers were hopeful the Fed was done hiking rates prior to the announcement yesterday.

And again, while they did hold rates steady, the dot plot indicated one more hike could be in the cards before the end of the year.

The Dot Plot Got Worse

These individual estimates from the dot plot also moved higher for 2024 and 2025, meaning rates may have to stay where they’re at for a bit longer than expected.

However, what does higher actually mean? Does it mean one more 0.25% rate hike from the Fed, but nothing beyond that.

And how does that translate to mortgage rates? On the one hand, it’s another rate hike, but mortgage rates only take cues from the Fed’s monetary policy.

If the Fed follows through with one more hike, but also signals that it’s done hiking, mortgage rates could breathe a sigh of relief.

In the meantime, their more hawkish stance might also be a positive because they’ve lowered expectations (for lower rates soon).

They’ve effectively got everyone on board the higher for longer train. They finally tackled the sentiment piece.

In other words, with everyone so glum, any weak economic data may now carry more weight.

Continue to Watch the Economic Data, Not the Fed Announcements

While the initial reaction to the Fed’s latest forecast was not good news for mortgage rates, or the stock market for that matter, it’ll be interesting to see what transpires once the dust settles.

Economic data had been mostly improving recently, in the sense that inflation was trending lower, which is the Fed’s primary objective.

But there were some hiccups recently, including lower-than-expected jobless claims, pointing to more economic resiliency.

However, if weaker economic data continues to come down the pipe, the Fed will be less inclined to raise its own rate and perhaps provide more clarity on future policy.

In that sense, not much has really changed here. The Fed is still data-dependent as it has always been.

Instead of watching Jerome Powell’s pressers, you may want to continue looking at the data that comes in, whether it’s the CPI report or jobs report. This is more important than looking at the dot plot.

Assuming the data continues to show a cooler economy, interest rates may not rise much more, and could simply linger at these higher levels.

But until we see consecutive reports showing a real drop in inflation, it’s going to be more of the same.

More Certainty from the Fed Could Keep Mortgage Rates in Check

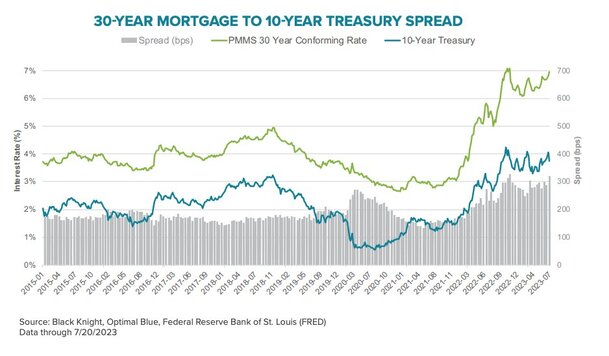

Lastly, we’ve got very wide mortgage spreads, which is the difference between the 10-year Treasury yield and the 30-year fixed.

It’s been close to 300 basis points for a while now, nearly double the long-run average of 170 bps.

If the Fed is able to provide more clarity on their policy by year-end, it might allow this spread to narrow. And that could offset any additional upward pressure on mortgage rates.

It’s somewhat bittersweet, but it could prevent the 30-year fixed from going even higher, say to 8%.

With the 10-year yield around 4.50 and the spread currently about 300 bps, 30-year fixed rates are hovering around 7.5%.

If that spread can come down to say 250 bps, you might get a mortgage rate back in the 6s, or at least offset any additional increases.

Tip: The prime rate, which is tied to HELOCs, moves in lockstep with the fed funds rate. So those with open-ended second mortgages have seen their rates go up each time the Fed raised its own rate.