If you think home prices are too expensive, you wouldn’t be the only one.

A new analysis from First American revealed that housing affordability is the lowest it has been in more than three decades.

In other words, it hasn’t been this expensive to purchase a home since the 20th century.

The title and settlement company’s Real House Price Index (RHPI) determines house-buying power using median household income, mortgage rates, and home prices.

And they found that real house prices, adjusted for these factors, were up nearly 17 percent year-over-year in July.

Blame Higher Mortgage Rates and Home Prices for a Lack of Affordability

As for why housing affordability continues to erode, it’s a combination of factors.

The first and most obvious issue is markedly higher mortgage rates, with the 30-year fixed mortgage now priced above 7%, assuming discount points aren’t paid.

Per Freddie Mac, rates on this most-popular loan program are up about 1% from year-ago levels. First American pegs the annual change at a higher 1.4 percentage point increase.

And if we zoom out a bit more, this key interest rate was in the 3% range to start out 2022.

So interest rates alone have wreaked havoc on housing affordability and home buying power.

Just consider a loan amount of $400,000 at a 3% rate versus 7% rate. We’re talking about a monthly principal and interest payment of $1,686 vs. $2,661.

That’s nearly $1,000 based on the interest rate increase alone. Then you have to factor in higher property taxes, higher insurance premiums, and so on thanks to a higher purchase price.

Yes, despite higher interest rates, nominal home prices have also risen year-over-year.

While people logically think there’s an inverse relationship with home prices and mortgage rates, this isn’t always true.

Per First American, nominal home prices (not adjusted for inflation) were also up 4% year-over-year.

This means a prospective home buyer faces both a higher purchase price and a significantly higher mortgage rate.

And though household income increased 3.7% since July 2022, it wasn’t enough to offset the higher costs associated with the jump in rates and rising nominal home prices.

Real Home Prices Are Now Above the 2006 Peak

If you recall the year 2006, you might remember that home prices peaked and then began to fall.

Back then, unsustainable home price gains were fueled by exotic financing.

Many home loans were underwritten via stated income or no documentation at all, while the products offered may have been option ARMs and other adjustable-rate mortgages.

Additionally, the typical down payment was at or close to zero, while the loan-to-value (LTV) ratio was often 100% when it involved a mortgage refinance.

In other words, home prices were too high, borrowers had little to no skin in the game, and many weren’t even qualified to be homeowners.

Without the widespread use of loose underwriting, home prices would not have been able to continue rising as high as they did.

As we know, the housing bubble burst set off the Great Recession, leading to double-digit home declines and scores of short sales and foreclosures.

Today, unadjusted home prices are 53.7% above those during the peak in 2006, while real prices are 0.7% higher than that housing boom peak.

While this might be reason to worry, consider the new mortgage rules that were born out of that crisis.

The Ability-to-Repay/Qualified Mortgage Rule (ATR/QM Rule) essentially outlawed much of what I just mentioned.

Borrowers today must be fully qualified when taking out a mortgage, and the vast majority are going with a 30-year fixed-rate mortgage.

Gone are the days of stated income underwriting and negative amortization. That makes the current situation more of an affordability crisis than a housing bubble.

It is driven more by a lack of supply than it is loose financing, with not enough inventory to meet demand.

Housing Is Overvalued Nationally, But Some Markets Remain Affordable

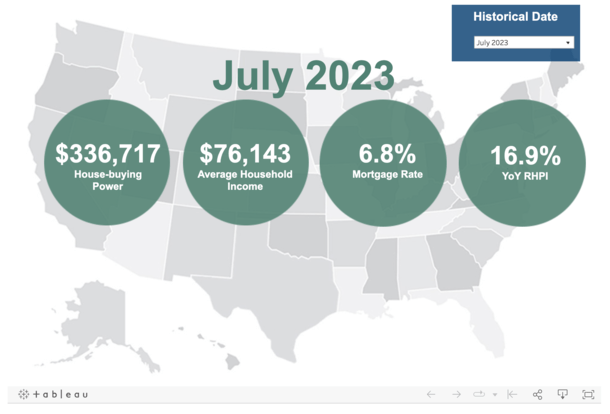

As noted, the July 2023 Real House Price Index (RHPI) increased about 17% from a year ago.

This meant the median sale price was roughly $345,000, while the median house-buying power was just $337,000.

Since house-buying power is below the median price, it means housing is overvalued. In an ideal world, it should be at or below the median.

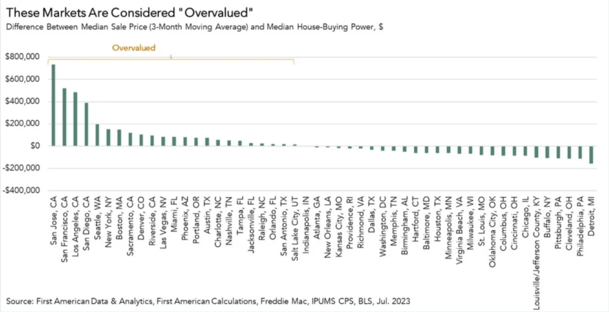

However, that applies to the national median price of real estate. Only 24 of the 50 top markets tracked by First American are overvalued by this measure.

Granted, it has worsened over time, as only 15 markets were considered overvalued last July.

At the moment, San Jose, California is the most overvalued metro, with the median sale price nearly $1,440,000 and consumer house-buying power just $700,000.

San Francisco and Los Angeles were also quite overvalued by this measure, though to a lesser degree.

Meanwhile, some undervalued markets still exist, if you can believe it. The metros of Detroit, Philadelphia, and Cleveland are undervalued by roughly $126,000.

How Do We Fix the Unaffordable Housing Market?

We know home prices are out of reach for many, but how do we fix it? Well, the Real House Price Index (RHPI) takes into account home prices, mortgage rates, and incomes.

So if you want housing to be more affordable, you need relief via those three elements.

This means either mortgage rates need to fall, home prices have to come down, or incomes must increase.

Or you get some combination of the three, such as a 1% drop in mortgage rates and a pullback in prices, which boosts affordability.

The problem at the moment is mortgage rates might be higher for longer, and home prices are pretty sticky due to a major lack of inventory (why are there no homes for sale?).

Incomes also don’t look to be increasing by a material amount, making it difficult for prospective buyers to get in the door.

One exception is new home sales, which have relied heavily on temporary and permanent mortgage rate buydowns to tackle the financing piece.

But there are only so many new homes for sale, and such sales only typically account for 10% of the overall market.

This explains the current housing market dynamic. Ultimately, there aren’t many existing homes on the market, not a ton of demand, and not a lot of sales.

And until something changes, this will likely be the status quo.

Read more: Why are home prices so high right now?