The housing market is in trouble. The latest blow being mortgage rates returning to 7%.

But the ongoing issue has been a severe lack of inventory, which differs greatly from conditions around the time of the Great Recession.

And the higher mortgage rates go, the worse the inventory situation gets. This is because existing homeowners are disincentivized to sell and lose their low rates.

At last glance, 84% of all outstanding mortgages had a mortgage rate at or below 5%, per 2022 HMDA data.

And 63% had a rate at or below 4%. Simply put, these homeowners don’t want to give up their low rate and replace it with a new 30-year fixed priced near 7%.

The Housing Market Is Hurting Due to a Lack of Inventory

As noted, the current state of the housing market is a lot different than the one seen back in 2008.

At that time, there were way too many existing homes on the market. And countless new housing developments littering the country.

In fact, there were so many homes that many projects were halted before they finished.

I vividly remember driving around the outskirts of Los Angeles and Phoenix, documenting the many new subdivisions that were desperately attempting to unload inventory.

There were so many vacant homes that it seemed nearly impossible for them to sell, ever.

Meanwhile, disgruntled owners who were often the only ones living on a particular street would post warnings to would-be buyers.

One owner literally had a sign posted on their yard that said something like “Don’t buy a house here!”

There was regret and they felt wronged. And they didn’t want others to fall prey to buying a home at a lofty price in the middle of nowhere.

But that was then, and this is now. Today, prospective buyers are hard pressed to find homes.

Sure, existing inventory has ticked slightly higher, and builders have supply gluts. But it’s nothing like it was.

Housing Inventory Is Up, But Remains Miniscule

The National Association of Realtors released its existing homes sales report for January earlier this week.

They noted that sales fell for the 12th consecutive month to a seasonally adjusted annual rate of four million.

Sales of existing homes were down 0.7% from December 2022 and a whopping 36.9% from the same time a year earlier.

Meanwhile, the median existing-home sales price actually rose 1.3% from one year ago to $359,000.

But here’s the most interesting part – inventory of unsold existing homes was 980,000 at the end of January, or the equivalent of 2.9 months’ supply at the current sales pace.

To put it in perspective, back in early 2009 housing inventory was at 9.6 months’ supply, per NAR.

There were 3.6 million unsold homes, which was actually an improvement from the 4.5 million a year earlier.

Today, there are less than a million, despite a 15.3% increase from a year ago (850,000).

The Double-Edged Sword of Low Mortgage Rates

While the low mortgage rates were a boon to homeowners over the past decade, they’re coming back to bite now.

First American economists refer to them as “golden handcuffs” because of the associated rate lock-in effect.

They inhibit movement for existing homeowners, and also restrict prospective home buyers at the same time.

And the higher rates go, the worse it gets. As the spread widens, existing owners have less incentive to sell.

That further reduces supply, which keeps property values inflated. But the combination of a high asking price and 7% mortgage rate doesn’t work for most.

While this may prove temporary, if mortgage rates eventually come back to 5%, what do buyers do in the meantime?

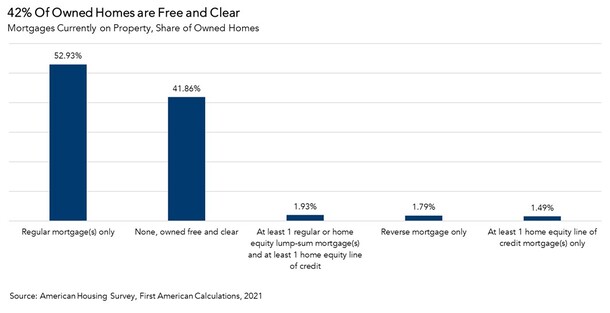

Can Free and Clear Homeowners Improve the Inventory Situation?

One place to look could be free and clear homeowners, those who owe nothing in the way of a mortgage.

Per First American, as of 2021 roughly 42% of American homeowners did not have a home loan. As such, they are unaffected by mortgage rate lock-in.

And nearly 78% of these free and clear owners were aged 55 or older. So if they were to move, there’s a good chance they’d downsize and buy with cash (using sale proceeds).

That means current mortgage rates aren’t a factor for them either. The only issue is many Baby Boomers are aging in place, aka not leaving.

So banking of them to improve the housing inventory problem might be a shot in the dark.

The takeaway is that there are too few existing homes on the market, and the higher mortgage rates go, the worse it will get.

This also explains why home prices are holding up okay, despite pulling back from their ridiculous COVID highs.

And why that 2008-esque housing market crash might prove to be elusive.

- Mortgage Rates Saved by Coolest Inflation Report Since 2020 - July 14, 2026

- Mortgage Rates Look Headed Back to War Time Highs - July 13, 2026

- Despite Headwinds, Odds of a 7% 30-Year Fixed in 2026 Are Super Low - July 9, 2026