Here’s an interesting one. Is it possible to obtain a lower mortgage rate without refinancing?

While it’s not all that difficult to refinance a home loan, it does take a bit of time and energy, and you generally need to qualify for the thing!

Not everyone qualifies for a mortgage for one reason or another, and the same goes for refinancing an existing loan.

For example, if your credit score isn’t quite up to snuff, or you don’t have the required income to keep your DTI below key levels, you may not get approved.

This means you might be locked out when it comes to obtaining a lower mortgage interest rate in times when rates are favorable.

There are also times when it just doesn’t make much sense to refinance because rates are higher or similar to what you’ve already got.

So what are you to do if you can’t or simply don’t want to refinance, but still want a lower rate? Well, there are some options to consider.

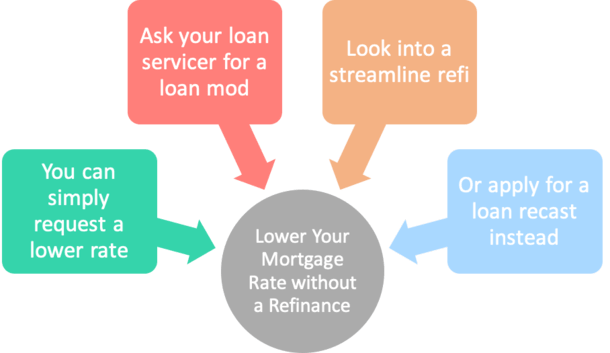

Just Call and Request a Lower Mortgage Rate

While perhaps not conventional or all that common, some folks have obtained lower interest rates simply by calling up their mortgage lender and requesting one.

This is formally known as a mortgage rate modification and offered with some credit unions and depository banks.

You need to indicate that you have no interest in refinancing with them because otherwise they’ll just take you down that route.

It’s kind of similar to the old credit card trick where you phone up and say, “Hey, I’m sick and tired of paying 20% APR!”

Then they put you on hold and come back and tell you congratulations, your rate is now 12%. Still bad, but lower!

Perhaps it won’t be that easy, or anywhere close to it, but sometimes it’s just a matter of being the squeaky wheel if you want a lower interest rate.

Your chances might be better if the originating lender also services your loan (collects your payments each month). And if your existing rate is significantly higher than current rates.

If they believe you’re going to take your business elsewhere, they might be willing to help you out.

Of course, at that point you could be asking yourself why not just refinance to an even lower rate, assuming you’re able to.

Tip: Third Federal’s Rate Relock feature allows its ARM borrowers to relock their rate without refinancing at any time for a small fee.

Negotiate Directly with Your Loan Servicer or Lender

There are also a number of programs geared toward those who are having trouble making payments each month, or difficulty refinancing via traditional means.

The two notable ones over the past several years have been HAMP and HARP, both of which allowed homeowners to obtain lower mortgage rates via special government programs.

These have been phased out, but replaced by permanent high LTV refinance programs set up by the likes of Fannie Mae and Freddie Mac.

There are also proprietary loan modification programs available (guidelines vary by individual lender) that may provide lower interest rates to existing customers.

Similarly, options have been rolled out to help homeowners affected by COVID-19, which include interest rate reductions.

Again, if you don’t take the time to contact your lender/loan servicer, you won’t know about them.

Take Advantage of a Mortgage Settlement

Thanks to some questionable practices by the big banks and loan servicers during the housing crisis, some lucky homeowners were offered lower mortgage rates as restitution.

A notable mortgage settlement between Bank of America and the U.S. Department of Justice resulted in 2% fixed mortgage rates for some fortunate borrowers.

Of course, they probably went through a lot to get that point. But one common theme is that not all homeowners pay attention to or take advantage of these things, and as such aren’t duly compensated.

Keep an eye out for legacy claims, and if they apply to you, it might be possible to save some money or secure a better rate in the process, all without refinancing.

Streamline Refinances Can Be a Lot Easier

Even if you’re not eligible for these programs or able to negotiate a lower rate, it might be possible to execute a streamline refinance.

As the name implies, it’s a faster and easier way to refinance a home loan for the express purpose of securing a lower interest rate.

This option allows you to refinance without the typical requirements like a minimum credit score or maximum LTV, and with limited paperwork. You might be able to skip the appraisal too!

Even though it’s technically still a refinance, it should prove to be a lot easier to qualify, and it shouldn’t be as painstaking of a process.

Look Into a Recast Instead of a Refinance

There’s also the lesser-known loan recast, which like a refinance, can lower the monthly payments on your mortgage.

The difference is you’re simply adjusting the amortization schedule of the loan.

Let’s assume you’ve been paying extra each month to lower your outstanding balance, which is great for saving money long-term, but does nothing to lower subsequent monthly payments.

If you want your lower balance to be reflected in your remaining payments, you can request a recast from your lender or servicer, which will re-amortize the loan.

Then you should have lower monthly payments going forward, without a refinance or the closing costs that come with it. There may be a small recast fee though.

The beauty of the non-refinance route is that you also don’t reset the clock on your mortgage. In other words, you don’t extend the term with a fresh loan.

Pay More Each Month and Enjoy the Same Interest Savings

Another thing you can do to save money without a mortgage refinance is to simply pay more each month, assuming you’ve got the cash on hand to do so.

This is yet another reason to set aside cash for a rainy day, or simply to better manage your debt when it’s favorable to do so.

The more you pay above what you owe each month, the more you’ll save over the course of your mortgage term, regardless of your interest rate.

In short, extra payments, such as biweekly ones or simply an additional payment each year, lower the amount of interest you pay.

While your mortgage rate won’t change, nor your minimum monthly payment, the amount of interest paid will, which is basically the same deal as a refinance without all the paperwork and qualifying.

Go with an ARM and Hope for the Best

If you want a self-service mortgage, you could also just go with an adjustable-rate mortgage straight from the get-go, which rise and fall over time as the economy does its thing.

While this might sound silly, tons of homeowners who took out ARMs prior to the recent housing crisis actually wound up with rock-bottom interest rates without lifting a finger.

They actually benefited tremendously as mortgage indexes hit all-time lows, assuming they kept their homes and their original mortgages.

Of course, this isn’t for the faint of heart, and the way things are looking at the moment, interest rates seem unlikely to go a lot lower.

Still, this is one way to potentially lower your interest rate without refinancing. Or doing anything at all.

Use a Second Mortgage to Pay Off the First

One final trick some folks use to reduce their mortgage interest expense is opening a second mortgage to pay off the first.

This way they don’t need to refinance, which can be a bit more involved than taking out a second.

It’s basically a form of arbitrage where interest rates are lower on the second than the first for one reason or another.

For example, if the interest rate on your first mortgage is well above going rates today, it could make sense.

This can be done with either a fixed-rate home equity loan or adjustable-rate HELOC. But it takes a bit (sometimes a lot!) of tinkering and money management skills to get it done.

So in the end, you might just be better off refinancing your mortgage or sticking to some of the alternatives discussed above.

Can You Switch Mortgage Companies Without Refinancing?

Lastly, you might be wondering if it’s possible to switch mortgage companies without applying for a refinance.

For example, if you really dislike the loan servicer you’re currently assigned to, can you request a switch? The answer is essentially “no” because you don’t get to choose your servicer.

Sure, you can pick the company that originates your home loan, but it will likely be transferred to a different company shortly after. And you won’t have any say.

Most mortgage companies don’t keep the loans they fund – they transfer them to third-party servicers that collect your payments year after year.

So you should really only concern yourself with pricing and customer service during the loan process. After that it’ll be out of your control.

If you truly can’t stand your servicer, a refinance would be one way to get a new one, but you could potentially wind up with the same company all over again once it’s transferred!

Read more: How soon can I refinance my home?

- Mortgage Rates Narrowly Avoid New 52-Week Highs as Bond Yields Surge Higher - July 31, 2026

- Trump Says Warsh Wants Lower Interest Rates, But Has a Political Board - July 30, 2026

- Do Mortgage Rates Need a Hike to Move Lower? - July 28, 2026