Mortgage Q&A: “Why are mortgage payments mostly interest?”

Here’s an interesting mortgage question – pun sadly intended because I couldn’t help it.

Lots of folks are obsessed with how much interest is paid on a mortgage, often citing the total interest paid over 30 years.

This counters the argument that mortgages are the cheapest debt you can own, which they basically are.

Let’s discuss what they’re getting at to see what all the fuss is about.

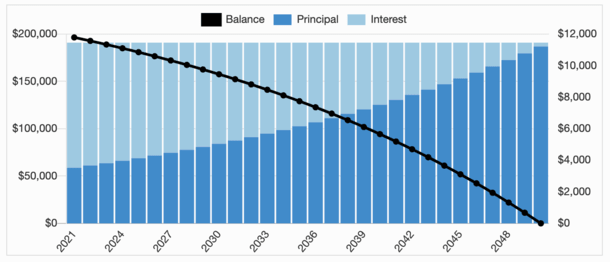

Payment Composition Over Time

- Most homeowners tend to take out fixed-rate mortgages

- The monthly payments on these types of loans don’t change during the full 15- or 30-year terms

- But while the mortgage payment remains constant throughout the life of the loan

- The amount that is allocated to principal and interest changes monthly as the loan is paid off

The way mortgages are set up here in the United States, each monthly payment is the same amount, assuming it’s a fully amortizing fixed-rate mortgage, which most tend to be.

The payment amount after month one is the same as it is during month 360, assuming you take out a 30-year fixed and keep it until maturity.

This makes housing payments more affordable (and predictable) because the balance is paid off evenly over a long period of time, such as 30 years.

However, even though the payment amount is fixed, the composition of the payment will change monthly until the loan term ends.

Just check out the chart above – the light blue interest portion of the payment declines over time as the dark blue principal portion goes up.

Let’s take a look at an example to illustrate:

Loan type: 30-year fixed mortgage

Loan amount: $200,000

Mortgage interest rate: 4%

In this common scenario, the monthly mortgage payment would be $954.83 for 360 months in a row. Ouch. That’s a long time.

Each month, the borrower would need to make the same payment to their lender or loan servicer in order to satisfy the entire balance in 30 years.

The amount would never change, though as mentioned, the composition would. In fact, it would change every single month during the loan term.

How Much Goes Where Each Month?

- During the early years of a home loan most of the payment goes toward interest

- This is the result of a large outstanding balance at the outset of the loan

- Over time more money shifts toward principal as the loan balance shrinks

- Unfortunately, most borrowers don’t keep their loans long enough to see this happen

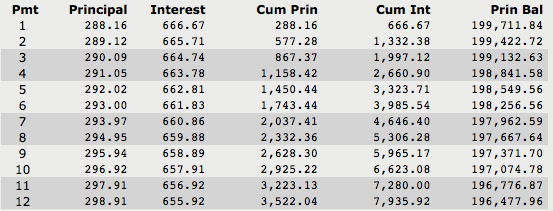

As you can see from this image of the amortization schedule, the first monthly mortgage payment consists of $288.16 in principal and $666.67 in interest.

In short, the first payment on a mortgage is “mostly interest.” In fact, interest accounts for nearly 70% of the first payment. Boohoo.

In the second month, the total payment amount is still $954.83, but the composition of the payment changes slightly.

The principal portion increases to $289.12, while the interest portion drops to $665.71.

Why is this? Well, remember the first month’s principal payment of $288.16? That lowered the outstanding principal balance from $200,000 to $199,711.84.

As a result, the interest due on the second monthly payment dropped, and the principal increased, because as noted earlier, the payment amount stays constant.

Over time, this trend continues. The principal portion of the monthly mortgage payment increases while the interest portion drops.

It’s pretty minimal in the beginning because little principal is paid each month with such a large balance demanding so much interest each month.

This is the “front loaded” argument you hear about – how interest makes up the lion’s share of early payments. It’s not a gimmick, just the way math works.

Principal Surpasses Interest!

- It takes nearly half the loan term for principal payments to exceed interest payments

- But once this finally happens payments become very principal-heavy

- This means more of your dollars are actually going toward paying off your home loan

- And in a few short years the loan balance is paid down pretty fast

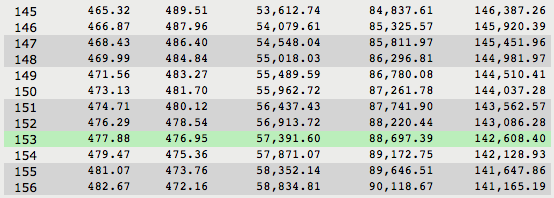

In month 153, or nearly 13 years into a 30-year mortgage, the principal portion of the mortgage payment finally surpasses the interest portion.

As seen in the screenshot above, the principal portion of the monthly payment is $477.88, while the interest portion is $476.95, which still equals the original payment amount of $954.83.

Interestingly, the outstanding loan balance remains a hefty $142,608.40, or 71% of the original balance.

It’s not until month 231, or nearly 20 years into the loan term, that the outstanding balance falls below $100,000, or less than half of the original loan amount.

In other words, the bank still very much owns your home, even though you think you’re the king or queen of your castle.

However, this is where the principal really starts to get paid down, as interest finally takes a back seat.

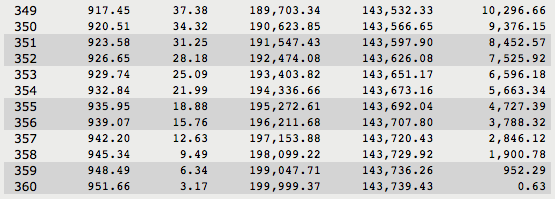

Barely Any Interest Is Paid During the Final Year of the Loan

During the final year of the loan term, each monthly payment is more than 96% principal, with very little interest due because the outstanding balance is so low.

A small outstanding balance coupled with a low mortgage rate means associated interest will be pretty insignificant, as seen in the image above.

We’re talking $37 bucks one month, $19 in another, and just over $3 in the final month!

Assuming the loan is paid off in full, as scheduled, a borrower would pay a total of $343,739.21, of which $143,739.21 would be interest.

So it’s not mostly interest, rather, it’s mostly principal.

The Real World Scenario

- Most homeowners sell their homes or refinance in less than 10 years

- For these borrowers their cumulative payments will be mostly interest

- But technically you should pay more principal than interest on a home loan

- You just need to hold it for a very long period of time to see that happen

In reality, many homeowners don’t hold their mortgages for the full term. In fact, most are said to hold their loans for a fraction of the loan term, such as seven or eight years.

That’s right – plenty of borrowers refinance, pay off the mortgage earlier, or simply sell their home and move on to another mortgage.

So it’s kind of misleading to look at mortgages as if they’re going to last the full term. But it’s for this very reason that mortgage payments tend to be mostly interest.

Because many borrowers never get to the point where the principal actually surpasses the interest.

When borrowers do refinance, critics will argue that they’re “resetting the clock,” which refers to extending the loan term and starting the process all over again.

For example, if you paid down your existing 30-year loan for 10 years, then refinanced into another 30-year loan, you’d extend the length of your mortgage.

Same loan amount, but longer time period to pay it off, even if your mortgage rate is lower.

As a result, your balance would be paid off over 40 years, as opposed to 30. That’s 10 years from the first loan and 30 years for the refinance loan, meaning it could result in more interest paid.

Again, most borrowers don’t hold their loans that long, so again this fear is overstated and sometimes not even relevant.

However, if you are deep into a 30-year mortgage and looking to take advantage of a lower mortgage rate, consider a shorter term as well, such as a 20-year or 15-year mortgage.

That way you’ll avoid paying extra interest and stay on track to be free and clear on your home as originally intended, assuming that’s your intention.

Read more: Should I Prepay the Mortgage or Invest Instead?

- Are Mortgage Rates Finally Poised to Start Falling Again? - June 25, 2026

- Mortgage Rates Are Having a Good Day as Oil Prices Fall to Pre-War Levels - June 24, 2026

- You Can Still Get a Sub-6% Mortgage Rate, But Is It Worth It? - June 23, 2026

So over 30 years, on a loan of $200,000 with a fixed interest rate of 4%, you will have paid nearly 75% extra just in interest. I don’t even know where to start understanding that math. Wouldn’t it drastically reduce the amount of interest you pay in the end if you just started off paying mostly towards your principal? I don’t think it’s simply “just how math works” but more just how banks work because they want your money.

Dave,

Ultimately, you pay a good chunk of interest when you have a very large loan amount, such as a mortgage, even if the interest rate is a relatively low 3% or 4%. This is compounded by the very long loan term, e.g. 30 years. It’s not a scam, it’s just how borrowing works with large amounts of money over long periods of time. And this is how home buying is kept affordable. Otherwise most wouldn’t be able to purchase homes, or prices would need to come way down.

Disgusting. Paying almost $150,000 in interest into the banker’s pockets. And that’s even with the outrageously low numbers quoted in this article. Try buying a home for $200k in most areas of the country. Ha! That’s money I could be spending on my family. Food, groceries, home repairs. I could be spending it at local stores, boosting the economy. Or putting it towards my retirement (as if we will ever be able to afford to retire). Instead it’s just going to make the rich richer. My wife and I weren’t able to afford our first home until our mid-40’s. We won’t have it paid off until we’re 80. If we even live that long. Home ownership is a scam. So much for “the American dream”. 😡

have a 3-year arm and i was told i can’t make more than 2 months ahead in payments. how is the interest figured? I have made payments since October and all of it is going to interest. I have a 975 month payment that includes escrow been paid 2 months ahead. I started making payments in January for the Feb 1 due date and all of it is going to interest my balance has not changed since i was 2 months ahead in Oct.

Shannon,

Instead of making payments ahead of time, you might be able to make additional payments to the principal balance, which will lower the amount of interest due, but won’t change future monthly payments. This will result in a mortgage paid off ahead of schedule.

How in the absolute f%ck is this still legal? I bought a house in 2007 for $141,000. I have paid just shy of $230,000 to date and still owe $112,000. I have not missed a payment. Money isn’t free but my God, how much do you need to profit from my loan? Gouging the entirety of the middle class over a basic NEED is the greatest gift my father’s generation has given us.

Jeremy,

Your numbers don’t make any sense. I think you are leaving something out of your scenario. If you have paid almost $230,000 over 16 years, your principal + interest payment would have to be almost $1,200 per month. That’s almost 80% higher than what a loan payment for $141,000 amortized over 30 years at 2007 interest rates would be. Some of the numbers in your post are not correct.

Amortization is the name of the game and why big banking is so profitable. The banks aren’t stupid and definitely aren’t in business to help people buy homes, they are in business to make money! Lenders could easily structure loans and payments so from each monthly payment would be split 50/50 between interest and principal but that would mean home owners would build equity a lot faster and the banks would make less money. Wouldn’t it be more fair to charge a 20% fee on a loan (borrow $500K, pay back $600K)? Of course it would! But then again the bank makes more money by charging 5% amortized over 30 years…so the banks and their underwriters choose the math that benefits them the most. That’s why they are creditors while the rest of us are forever debtors :)

Jimmy,

There are lots of mortgage options available, including 15-year fixed, 10-year fixed, and even shorter terms. Also, most mortgages don’t have a prepayment penalty so you can pay it off as quickly as you’d like. The reason most are 30-year fixed is because they wouldn’t be affordable to most home buyers otherwise.