It’s been a rough week for mortgage rates, which are reeling thanks to new aggressions in the Middle East.

The ceasefire that began on June 17th is apparently no more, with major strikes exchanged between the U.S. and Iran over the past couple days.

That’s putting renewed pressure on oil prices, bond yields, and of course mortgage rates.

But despite all that, the odds of the 30-year fixed rising significantly higher from here remains pretty low.

That’s if you believe the odds…

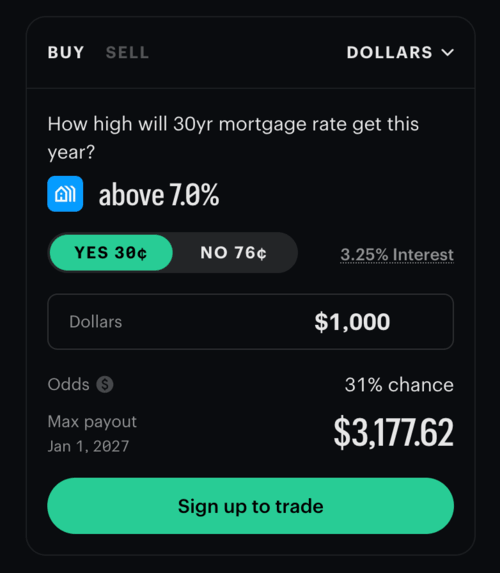

Only a 28% Chance the 30-Year Fixed Rises Above 7%?

The latest odds from prediction market Kalshi reveal there’s only a 28% “chance” that the 30-year fixed climbs above 7.0% at some point this year.

For reference, the 30-year fixed is currently averaging 6.43%, based on Freddie Mac’s weekly mortgage rate survey.

That number is sure to climb when they release their update today, but it’s only about 50 basis points away from being in the money.

Meanwhile, all I hear is people saying mortgage rates are going back to 10% or higher!

Or that they’ll be in the double-digits soon enough. Blah blah blah.

Then I think to myself, we can’t even break 7% and you’re telling me they’re going to 10%?

It seems that the high interest rate predictors are driven more by emotion than actual logic.

They want higher interest rates because they think it will fix things and stop prices from going higher and higher.

Perhaps, but are such rates actually warranted? It’s not the 1980s all over again.

Yes, we have an energy shock of sorts, but we are also a lot more energy independent today than back then.

The Fed also knows how to manage inflation a lot better today versus that time thanks to mistakes learned along the way.

So to think interest rates are going to rival those seen in the 1980s when the 30-year fixed briefly spiked to 18% might be a bit silly.

And it might also explain why even the odds to creep up even another 50 bps remains a long shot.

How Could Mortgage Rates Get Back to 7% or Higher?

Now just because the odds are low doesn’t mean it can’t happen.

There have been plenty of instances where the unexpected has happened and underdogs have cashed.

Kalshi uses Freddie Mac’s Primary Mortgage Market Survey (PMMS) to determine the outcome and as noted, it’s currently around 6.50%.

In order for mortgage rates to climb another 50 bps this year, we’d need a lot of sustained hot economic data to come through.

The two key drivers of mortgage rates are inflation and labor data.

That means we’d need hot CPI, PPI, and PCE prints along with hot jobs reports for the next few months, perhaps with no let up.

Last month, inflation rose above 4% for the first time in three years, per the Bureau of Labor Statistics (BLS), but it was mostly tied to volatile energy prices related to the Iranian conflict.

Once energy and food were stripped out, core CPI was up just 2.9% from a year earlier.

Still elevated and above the Fed’s 2% target and possibly enough to entertain some rate hikes later this year if it doesn’t improve.

However, there’s also the labor market, and that hasn’t been so hot lately. The most recent reports weren’t ice cold by any stretch, but the Fed still has to balance inflation and jobs.

And if jobs remain weak, they might be limited in how much they can hike, meaning one or two 25-bp hikes could be it, despite inflation concerns.

The takeaway here is despite inflationary headwinds, much of it recently tied to the war, the economy doesn’t look so strong.

So even if there’s some upward pressure on interest rates, it could prove to be short-lived and also offset by rising unemployment.

Lastly, let’s not forget that mortgage rates are up nearly 0.75% since the end of February when the conflict began, so a lot of risk is already baked in.

That’s why a 7% mortgage rate, which doesn’t even sound all that unlikely, could remain elusive.

- Despite Headwinds, Odds of a 7% 30-Year Fixed in 2026 Are Super Low - July 9, 2026

- Just When You Thought 7% Mortgage Rates Were Off the Table - July 8, 2026

- Light Week for Economic Data Means Flat Mortgage Rates Likely - July 6, 2026