The Federal Housing Administration (FHA) finally announced a new policy, which is temporary, to endorse mortgages where the borrower has requested or obtained COVID-19 forbearance.

Mortgagee Letter 2020-16 temporarily reverses the FHA’s existing policy that doesn’t permit FHA insurance for mortgages in forbearance.

The agency said the policy ensures “the safeguards of the FHA program continue to work for new homeowners facing a financial hardship due to COVID-19.”

Now before mortgage lenders get too excited about this, there is a major hitch. They must sign an indemnification agreement with the FHA that leaves them on the hook for 20% of the original loan amount if it goes bad.

What Are the Requirements for Insuring FHA Loans in Forbearance?

- Borrower must be experiencing a financial hardship due directly or indirectly to COVID-19

- Mortgage must have been current at time of request for forbearance

- Mortgage must satisfy all requirements for FHA insurance at time of closing

- Mortgagee must execute a two-year partial indemnification agreement

Aside from that pretty significant piece about lenders being liable for 20% of the original loan amount, there are also some general requirements that must be met.

First off, the borrower must be experiencing a financial hardship directly or indirectly related to COVID-19 and in a forbearance plan.

Additionally, they must have been current on the mortgage at the time they requested the forbearance.

In the letter, the FHA says “forbearance provided to borrowers experiencing a financial hardship due, directly or indirectly, to COVID-19 is not considered the provision of funds by a Mortgagee to bring and/or keep the mortgage current or to provide the appearance of an acceptable payment history.”

In other words, the loan won’t be insurable if the borrower was already behind on the mortgage before asking for a break on payments.

Like any other FHA loan, it must satisfy all requirements for FHA insurance at the time of closing.

And as mentioned, the originating lender must execute a two-year partial indemnification agreement for 20% of the original loan amount.

The somewhat good news for lenders is that they’re only on the hook for that 20% if the mortgage goes into foreclosure and results in a claim to the FHA’s Mutual Mortgage Insurance (MMI) Fund.

But it could lead to lender overlays, like higher credit scores or a max number of forborne payments, to limit the likelihood of these loans going sour.

May Have Been an Alternative to Raising Mortgage Insurance Premiums

HUD Deputy Secretary Brian Montgomery said, “This policy helps address current and future capital issues for all lenders, including those who are not equipped to hold mortgages on their balance sheets for extended lengths of time.”

While maybe true, it doesn’t explain how they’ll pay those claims if lots of homes go into foreclosure in the two-year indemnification period.

However, the FHA did add that it won’t require upfront payments by lenders or an adjustment to FHA mortgage insurance premiums for such loans.

And added that it would “generally result in a reduction of the claim amount FHA would need to pay to the lender for defaulted mortgages.”

Lenders might have time on their side since the housing market is on pretty good footing and mortgage rates are super cheap, meaning housing payments should be more or less affordable.

Foreclosures also take quite a bit of time these days, so depending on when that clock starts ticking, there may not be too many claims.

Of course, I don’t know how comfortable lenders are sitting around and wondering if a home loan will go bad at some point. And it’s a two-year period to sit around and wait.

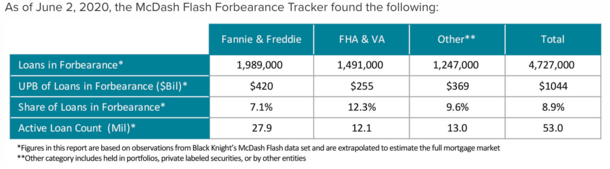

Earlier this week, the MBA said 11.82% of outstanding Ginnie Mae-backed loans (FHA/USDA/VA) loans were in forbearance, while Black Knight reported today that 12.3% of FHA/VA mortgages are now in forbearance.

But the number of homeowners in forbearance plans decreased for the first time since the crisis began, with 34,000 fewer homeowners in forbearance as of June 2nd thanks to a 43,000 decline among government-backed mortgages.

Read more: Fannie and Freddie Will Buy Loans in Forbearance

- Despite Headwinds, Odds of a 7% 30-Year Fixed in 2026 Are Super Low - July 9, 2026

- Just When You Thought 7% Mortgage Rates Were Off the Table - July 8, 2026

- Light Week for Economic Data Means Flat Mortgage Rates Likely - July 6, 2026