The latest Mortgage Monitor report from Black Knight reveals that many homeowners in forbearance plans are sitting on a healthy amount of home equity, meaning if they’re forced to sell banks may not lose out.

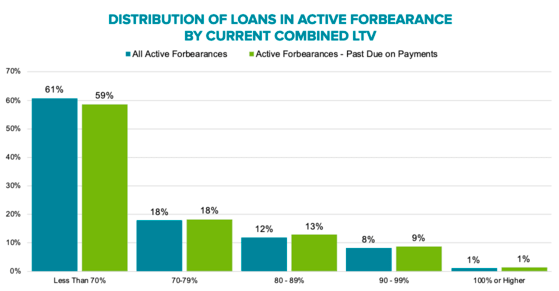

Per the data analytics company, fewer than one in 10 homeowners (9%) in forbearance have 10% or less home equity in their property, which the company believes is “typically enough to cover the costs of selling the property.”

Additionally, just one percent of homeowners in forbearance are currently underwater on their mortgages, surely a bad sign if they stop making monthly payments too.

Overall, 80% of the 4.76 million homeowners in active forbearance plans have 20% or more equity in their homes, meaning they’ve got options and loan servicers do too.

This should reduce the number of foreclosures that hit the housing market and also keep default-related losses in check, a good sign for the housing market and the borrowers at risk of losing their homes.

Home Equity the Difference This Time Around

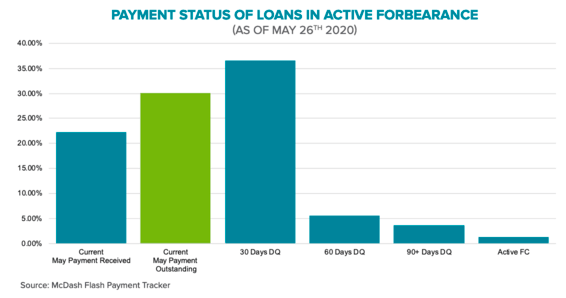

- 4.76 million homeowners in active forbearance as of May 26th

- 46% of homeowners in forbearance made their April mortgage payment as of April 30th

- 22% of those in forbearance have made their May payments as of May 26th

- Forbearance volume declined for the first time since the COVID-19 pandemic began

The last mortgage crisis was marked by toxic mortgages and a lack of home equity, a one-two punch that sent to the housing market to its knees. Or whatever’s worse than that.

Today, homeowners are flush with equity, thanks to years of home price appreciation and an abundance of boring old fixed-rate mortgages that do nothing but pay down the outstanding principal balance.

At the same time, home equity extraction has been uncommon, with cash out refinance volume a fraction of what it was leading up the crisis in the early 2000s.

This puts borrowers in a much better position, along with loan servicers, and means the housing inventory shortage likely won’t see any relief due to COVID-19-related foreclosures.

While nearly five million American homeowners have paused mortgage payments, most will likely retain their properties through the crisis because only 446,000 have combined loan-to-value (CLTV) ratios of 90% or higher.

That could keep home prices elevated as fewer properties hit the market amid an ongoing supply shortage.

Borrowers with FHA and VA Loans the Most Equity Poor

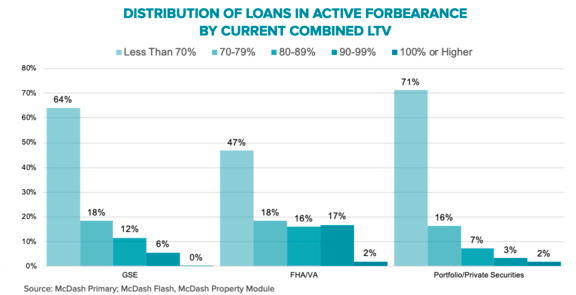

- FHA/VA loans only make up about one-third of all active forbearances

- But 19% of FHA/VA loans in forbearance (285k) have less than 10% equity

- This represents nearly two-thirds of all low-equity loans in forbearance

- Just 6% of GSE and 5% of portfolio loans in forbearance have less than 10% equity

Before we get too optimistic here, there’s one segment of the mortgage population that isn’t in as good of shape.

I’m referring to the holders of FHA loans and VA loans, which have continued to exhibit the highest rate of forbearance among homeowners.

To make matters worse, some 19% of such homeowners hold 10% or less equity in their homes, which could be a problem if they’re unable to resume regular mortgage payments.

This is of particular concern to lenders that originate FHA loans seeing that the agency just released guidance about mortgages in forbearance, which puts them on the hook for 20% of the original loan amount if the borrower forecloses within two years.

It also speaks to the issue of offering low-down payment mortgages to borrowers with equally low FICO scores.

Yes, Fannie Mae and Freddie Mac offer mortgages with just 3% down versus 3.5% with the FHA, but they require a 620 FICO score vs. a 580 FICO with the FHA. And the VA doesn’t even require a down payment.

While access to credit is key, there needs to be a balancing of risk as well to avoid another housing crisis.

Lastly, Black Knight noted that with 30-year fixed mortgage rates at 3.15%, roughly 14 million homeowners could save at least 0.75% on their current interest rate via a mortgage refinance.

- Mortgage Rates Get Much Needed Relief Thanks to a Taco? - August 3, 2026

- Mortgage Rates Narrowly Avoid New 52-Week Highs as Bond Yields Surge Higher - July 31, 2026

- Trump Says Warsh Wants Lower Interest Rates, But Has a Political Board - July 30, 2026