If you’re thinking about buying a home, or refinancing an existing home loan, mortgage rates are likely top of mind.

As you may or may not know, mortgage rates can change daily based on market conditions, similar to the stock market.

This means they can be higher one day and lower the next. Or they may do next to nothing at all from day to day, or even week to week.

But having an idea of which direction they’re going can be helpful, especially if you’re actively shopping your rate.

Let’s discuss a simple way to track mortgage rates using readily available economic data.

You Can Track Mortgage Rates Using the 10-Year Bond Yield

- Simply look up the 10-year bond yield on your favorite finance website

- Check the direction it’s going (like you would a stock ticker)

- If it’s up then mortgage rates will likely be higher than yesterday

- If it’s down then mortgage rates will likely be lower than yesterday

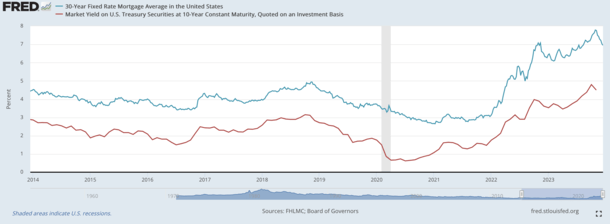

Hands down, the simplest way to track mortgage rates is the 10-year treasury bond yield.

Over time, mortgage rates and the 10-year yield have moved in near lockstep, as seen in the graph above from FRED.

In other words, when 10-year yields fall, so do mortgage rates. And when yields rise, mortgage rates climb higher.

As for why, many 30-year fixed mortgages are paid off in about a decade. This means the duration is similar to a 10-year bond.

But because mortgages have prepayment risk, there is a “spread,” or premium that is paid to investors of associated mortgage-backed securities (MBS), which are also bonds.

This spread is the difference between the going 30-year fixed mortgage rate and the 10-year yield.

For a long time, it hovered around 170 basis points. This meant if a 10-year bond was yielding 3.00%, a 30-year fixed mortgage might be priced around 4.70%. Or perhaps 4.75%.

So in order to track mortgage rates, you simply had to look up the 10-year yield and add this spread. Then you’d have a ballpark price for mortgage rates.

Tip: The Fed doesn’t control mortgage rates, so if they announce a rate cut it doesn’t mean mortgage rates will fall too.

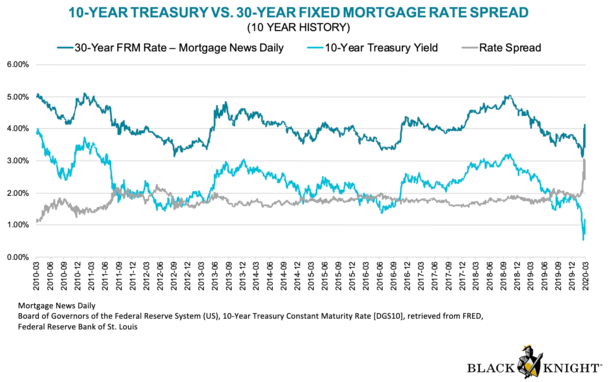

Mortgage Rate Spreads Have Widened, But the 10-Year Bond Yield Is Still Relevant for Tracking the Direction of Rates

Recently, mortgage rate spreads widened considerably due to economic uncertainty, heightened prepayment risk, out-of-control inflation, and other factors.

At one point, the spread was more than 300 basis points, or roughly double the norm, as seen in the chart above. This made tracking a bit more difficult, but the direction of yields and rates was still relevant.

So even though the spreads were wider, if the 10-year yield went up on a given day, mortgage rates likely increased as well. Or vice versa.

This means you can still look up the 10-year bond yield and determine which way mortgage rates will go that day.

If yields are up, mortgage rates will likely be up too. If yields are down, there’s a good chance mortgage rates will be down also.

The same goes for magnitude of change. If yields plummet, mortgage rates should also improve a lot. But if yields surge higher, watch out for much higher rates.

Now back to those wide spreads. Over the past 18 months or so, the Fed has been battling inflation with 11 rate hikes via their own federal funds rate.

But now that the Fed has indicated that their next move could be a rate cut, and that inflation may have peaked, there’s a lot more calm in the markets.

As such, spreads have come back down to around 270 basis points. While still ~100 bps higher than normal, it’s moderating.

And again, we can still guess direction regardless of the spread being wider than usual.

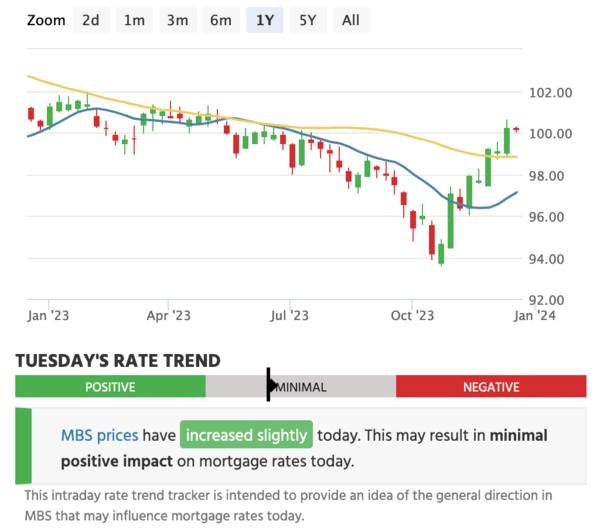

MBS Prices Are Even More Accurate Than 10-Year Bond Yields When Tracking Mortgage Rates

A mortgage rate purist will tell you that the 10-year bond is a great benchmark to track mortgage rates. But that looking at actual MBS prices is better.

This is true because MBS prices directly impact mortgage rate movement. So if MBS prices fall on a given day, mortgage rates will rise.

Remember, when the price of a mortgage bond falls, due to less demand, its yield, aka interest rate, increases.

As such, if you want mortgage rates to go down, you’ll be rooting for MBS prices to increase. And they’ll increase if demand is strong, thereby pushing yields down.

Now the question is how do you go about tracking MBS prices?

While you can track the 10-year bond yield on Yahoo Finance (as seen above), Google Finance, Marketwatch, CNBC, you name it, MBS price data isn’t as readily available.

However, Mortgage News Daily does a good job of posting daily MBS prices on its website.

They list both UMBS for Fannie Mae and Freddie Mac (conforming mortgages) and Ginnie Mae (GNMA) MBS for FHA loans and VA loans.

If you’re curious if mortgage rates are up or down on a given day, head over there and look at MBS prices.

Remember, if MBS prices are down, mortgage rates will be higher. And if MBS prices are up, mortgage rates will be lower.

To sum things up, tracking mortgage rates isn’t too difficult. Simply look up the 10-year yield each morning and also check out MBS prices.

From there you’ll have a pretty good idea of whether they’re going to be higher or lower than the previous day.

Now when it comes to predicting them, that’s another story altogether…

Read more: 2026 Mortgage Rate Predictions

(Photo: fdecomite)

- Are Mortgage Rates Finally Poised to Start Falling Again? - June 25, 2026

- Mortgage Rates Are Having a Good Day as Oil Prices Fall to Pre-War Levels - June 24, 2026

- You Can Still Get a Sub-6% Mortgage Rate, But Is It Worth It? - June 23, 2026