Assuming you want to become a homeowner, it’s probably best to go to college, even if you have to take out costly student loans in the process.

You may have read articles over the past several years that talk about snowballing student loan debt and the inability to afford a mortgage as a result.

While this might be true in some cases, it turns out you’re still more likely to buy a home if you obtain at least a bachelor’s degree.

The Benefits Outweigh the Costs

A commentary (since removed) from mortgage financier Fannie Mae revealed that those who go to college are more likely to become homeowners than those who simply graduate from high school.

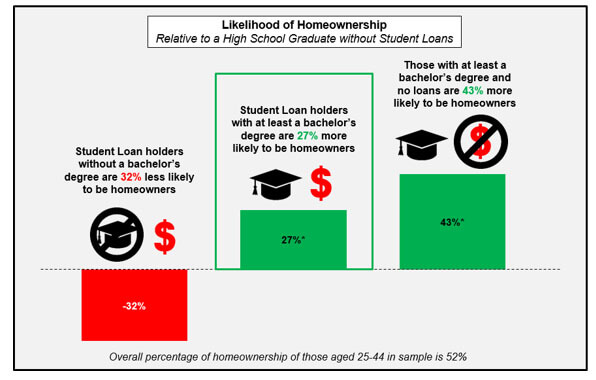

The most probable homeowners are those with a college education and no student loans, with a likelihood of homeownership that is 43% higher than high school graduates without student loans.

Meanwhile, student loan holders with bachelor’s degrees are still 27% more likely to become homeowners relative to those debt-free high school graduates.

There is a catch though – if you don’t actually complete your bachelor’s degree and simply wind up with student loans, you’re actually worse off than those who simply called it quits after high school.

This last group is 32% less likely to own a home than a debt-free high school graduate. They’re also more likely to be behind on student loan payments, which isn’t very surprising.

The takeaway here is that it pays to go to college, even if it costs and arm and a leg.

The idea being that college grads get paid more and are eventually able to qualify for mortgages to purchase homes.

Don’t Be Discouraged If You Have Student Loans and Need a Mortgage

As noted, student loan debt has increased substantially in recent years and its effects may not yet be evident in the homeownership numbers.

Additionally, the majority of those surveyed by Fannie Mae had student loan debt that accounted for 10% or less of their monthly income. Others might not be so lucky.

If you have outstanding student loans, you can still get approved for a mortgage. It just might affect how much you can afford because it will be factored into your DTI ratio.

Many student loans are deferred to help recent graduates get up and running before they are gainfully employed. However, mortgage lenders know these individuals will eventually have to repay their loans.

As a result, lenders must still account for the student loan repayment when qualifying you for a mortgage to ensure your home loan is actually affordable.

Of course, it depends on the type of mortgage you apply for.

Fannie Mae Student Loan Guidelines

When it comes to Fannie Mae (conforming loans), if the student loan payment amount is listed on the credit report, it can be used for qualifying purposes. End of story.

If the payment isn’t listed on the credit report, or shows $0, or is deferred, different rules apply.

For those in an income-driven payment plan, and documentation shows the actual monthly payment is zero, the lender may qualify the borrower with a $0 payment.

For student loans that are deferred or in forbearance, a payment equal to 1% of the outstanding balance can be used to determine the monthly payment.

So if there’s a $25,000 student loan, $250 is added to your monthly liabilities to calculate your DTI, even if it’s lower than the actual fully-amortizing payment.

Lenders are also able to calculate a payment that will fully amortize the loan based on the documented loan repayment terms, which may result in a lower monthly liability.

While this may seem harsh, it used to be 2%, or $500 in our example above.

But Fannie determined that actual monthly payments were generally less than 2% of the total balance.

The old policy also required lenders to use the greater of the actual monthly payment or 1% of the balance, unless the payment was fully-amortized and not subject to any future adjustments. But this made no sense either.

Freddie Mac Student Loan Rules

If the student loan(s) is in repayment, deferment, or forbearance, Freddie Mac breaks it down into two options.

For loans with a monthly payment greater than zero, the actual payment amount found on the credit report or other file documentation can be used.

If the monthly payment amount reported on the credit report is $0, the lender must use 0.5% of the outstanding loan balance as the payment for qualifying purposes.

So using our same example from above, a $125 payment would be factored into your DTI to determine if you qualify.

This could make it easier to qualify for a Freddie Mac-backed mortgage versus a Fannie Mae loan.

Additionally, it might be possible to exclude the student loan payment from your DTI ratio if there are 10 or less monthly payments remaining.

FHA Student Loan Guidelines

HUD just announced new changes on June 18th, 2021 that may make it easier to qualify for an FHA loan if you have student loan debt.

Regardless of payment status, when the payment is above $0 the lender must use the payment amount reported on the credit report or the actual documented payment.

If the payment amount listed is zero, 0.5% of the outstanding loan balance is used to calculate the payment, similar to Freddie Mac.

So again, it’d be a payment of $125 using our example of $25,000 in debt.

Prior to this change, the FHA used 1% of the balance, so the $25,000 loan would have resulted in a $250 per month liability for your DTI ratio.

Obviously this can have a huge effect on what you can afford. And apparently more than 80% of FHA-insured mortgages are for first-time home buyers.

Additionally, the FHA estimates that nearly half (45%) of these borrowers have student loan debt, with people of color the most impacted.

This explains the easing of the rule, and pales in comparison to the old requirement of 2% of the outstanding balance if no payment was found!

VA Student Loan Rules

When it comes to VA loans, student loan payments can be ignored if payments won’t begin for more than 12 months from loan closing.

This can be a huge advantage if your liabilities would push you over the allowable max DTI ratio.

But if student loan repayment has started or is scheduled to begin within 12 months from the date of the VA loan closing, the lender must count the actual or anticipated monthly payment.

They use a formula that calculates each loan at a rate of five percent of the outstanding balance divided by 12 (months).

So using our $25,000 example, it’d be $104.17. However, if a higher payment amount is listed on the credit report, such as $150, it must be used.

If the payment listed on the credit report is lower than the threshold payment calculation above, a statement from the student loan servicer that reflects the actual payment may be permitted.

USDA Student Loan Guidelines

For USDA loans, the actual student loan payment can be used if it’s fixed (and has a fixed term) without future payment adjustments.

If no payment is reported or it is deferred, 0.5% of the loan balance is used unless there is evidence that it’s a fixed payment.

Using our $25,000 example, it’d be $125, similar to the other loan types listed above.

If you’re close to maxing out with regard to DTI, an experienced mortgage broker or lender might be able to get you approved using a mortgage that has a more forgiving policy with regard to student loan debt.

Don’t give up until you consider several scenarios and exhaust all your options.

But also make sure you factor in any student loan debt early on in the mortgage discovery process so you don’t overlook this key qualification aspect.

A good rule of thumb might be to calculate your DTI using 1% of your student loan balance for the monthly payment, even if it turns out you can use a lower documented payment. This way you’ll still qualify in the worst-case scenario.

Also watch out for lender overlays that call for higher minimum monthly payments than the guidelines actually require.

- Mortgage Rates Are Now Higher Than They Were a Year Ago - August 5, 2026

- Chase Is Advertising Mortgage Rates With Nearly Two Discount Points to Keep Them Looking Attractive - August 4, 2026

- War De-escalation = Lower Mortgage Rates - August 4, 2026