Over the past few years, it’s gotten a lot easier to get a mortgage as technology has evolved.

Today, when a mortgage lender asks for your financials, you may be given the option to grant digital access to things like your credit history, income, and assets using your login credentials.

There’s much less of a need to collect, scan, and fax documents, or even upload them anymore.

Yes, that too is becoming passé, thanks to single source validation and real-time income and asset reports.

Unfortunately, one area that continues to be problematic is mortgages for self-employed borrowers, who often have more complicated financial situations that can’t be run through an automated underwriting system.

That’s beginning to change as well, but if you’re self-employed and in need of a home loan, there’s a good chance the process is going to be more challenging than you expect.

In fact, Fannie Mae’s automated underwriting system used to explicitly view self-employment as representing increased risk.

But going forward, now evaluates the composition of a borrower’s income instead.

So borrowers whose total annual income consists of a higher percentage of variable income, such as bonus pay, overtime, and commissions, will be seen as higher risk.

You may also be restricted in how much you can borrow thanks to lender overlays, so be sure to take the time to shop around as requirements can vary by bank.

Self-Employed vs. Salaried Borrowers

- If you are a W-2 employee you are considered salaried

- If you run your own business or receive 1099s you may be considered self-employed

- Both types of borrowers must be fully underwritten in order to get approved for a mortgage

- But documentation requests are generally more involved for self-employed borrowers

There are two main types of borrowers – those who are salaried and those who are self-employed.

As alluded to above, salaried borrowers, otherwise known as W-2 borrowers, are pretty easy to underwrite.

These individuals work at a company, get paid a salary (that often doesn’t change much from year to year), and can easily provide consistent pay stubs and W-2s to determine affordability.

For example, if you make $75,000 working at Corporation X, and have been working there for three years, you’d simply furnish your W-2s and some recent pay stubs. Simple as that on the income front.

But what if you own a small business? Or you’re part of the gig economy? That’s where things can get complicated in a hurry.

After all, there’s a good chance you didn’t make the same amount last year as you did in the year prior. In fact, you might have experienced massive swings in profitability over recent years.

There are also your business expenses that need to be considered, relative to what you brought in, how long you’ve been in business, the viability of your business, and so on.

Self-employed borrowers tend to write off a ton of expenses, which while tax-beneficial, may make it appear like you make less money.

An underwriter has to look at your business along with you as a borrower, so their work is at least two-fold.

All of these factors make it more difficult for a mortgage lender to sufficiently underwrite your loan file, and explain why stated income loans came to be.

Ultimately, things probably aren’t as cut and dry as they’d be for a salaried borrower, but they still need to ensure they’re originating sound loans, especially if they sell them off shortly after funding.

As a result, you should anticipate more documentation requests and letters of explanation to get to the finish line.

So yes, you can still get a mortgage if you’re self-employed, just expect it to take a little longer and be more involved.

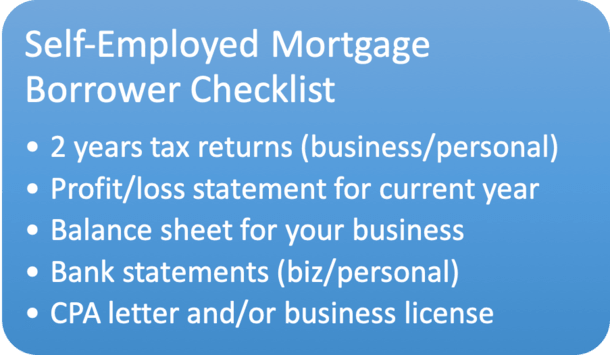

Self-Employed Mortgage Requirements

- 2 years of tax returns

- 2 years of business tax returns (if applicable)

- Profit and loss statement for current year

- Balance sheet

- Individual and business bank statements

- CPA letter and/or business license

Whether you’re a salaried employee or self-employed, you’ll need to provide various financial documentation to the lender to qualify for the loan.

For self-employed borrowers, this list is a bit more exhaustive, and may depend somewhat on the nature of your business.

Like salaried borrowers, mortgage lenders will ask for a two-year history of earnings to ensure your income is stable and likely to continue.

You can expect to be asked to provide the most recent two years of tax returns, and two years of business tax returns if applicable (assuming you aren’t a sole proprietor).

This may include things like a Schedule K-1 if you’re involved in a partnership, S corporation, or LLC.

It can also be a lot less complicated if you simply run your numbers through Schedule C as a sole proprietor.

How Underwriters Look at Self-Employed Borrowers

- Unlike a W-2 employee whose job security is assumed to be safe

- You’ll need to prove you can go it alone and continue to earn on your own

- It’s helpful to have been self-employed in the same line of business for several years

- You can bolster your chances of approval by having more assets and fewer write-offs that cut into your take home income

Regardless of how you file, while your business might make X, you may only take home part of that money, which is then used to determine mortgage affordability.

This is where things get murky as there may be a large divergence in earnings from year to year as a business owner.

For example, say you made $80,000 two years ago, but only $45,000 in the past tax year.

The underwriter will average income over the two years, meaning only about $5,200 in income can be used to offset your proposed monthly housing payment.

Secondly, the declining income will raise serious red flags, and require a letter of explanation on your part.

If you can explain it and it’s not a sign of worse things to come, it might be fine. But again, you’ll have less income to use toward mortgage qualification, which could jeopardize your loan as well.

Generally, you’ll want your annual income to be steady or rising to avoid any additional scrutiny.

This is one downside to self-employment that often isn’t an issue for salaried borrowers, who tend to take home consistent paychecks.

Underwriters also need to determine that any money taken away from the business won’t negatively impact its operation going forward.

So they’ve got a lot of work to do, and as such patience is paramount.

Additionally, you’ll likely be asked to provide a profit and loss statement for the current year, along with a balance sheet, to tie up the loose ends.

Sure, your last two years may have been stellar, but the underwriter will also want to know what you’ve done for them lately.

These can be pretty easy to complete, or quite complex, depending on the type and size of your business.

A sole proprietor may have no trouble whipping these up in a few hours or less, whereas someone with a large business may need days.

Finally, you’ll need to provide a business license (if you have one) and/or a CPA letter from the individual who prepared your taxes.

If you have neither, perhaps because you run a simple business and like to complete your taxes on your own via Turbo Tax, you might receive some additional scrutiny.

Make Your Business Easy to Understand for the Underwriter

Similar to salaried borrowers, life can be easier if your loan file makes sense, and you’ve demonstrated the ability to make money, save it, and continue to grow your business.

This can put the underwriter at ease, and may even reduce documentation requests.

For example, if you have enough of your own money (not business funds) to fund the down payment and closing costs, you’ll get a leg up.

Same goes for those who have been self-employed in the same line of business for at least five years, with growing income.

If this is the case, the lender may be able to waive the need for business tax returns, which is certainly a plus.

And you may only need one year of tax returns if your borrower profile is particularly strong.

Getting a Mortgage If Self-Employed Less Than Two Years

- You typically need at least two years tax returns to get approved for a mortgage as a self-employed individual

- There are exceptions to the rule if you’ve been self-employed between 12-24 months

- But your new gig must be in the same line of business as your old job, and you must make the same income (or more)

- If you satisfy these requirements one year of tax returns may suffice

You may be wondering if it’s possible to get a mortgage if self-employed for less than two years.

The good news is yes, it is possible. The bad news is that it depends on the situation, and more conditions must be met.

Again, like a salaried borrower, a self-employed borrower must show a two-year history of earnings to demonstrate their ability to meet their obligations.

It’s possible to satisfy this condition if you worked in a similar line of work before making the jump to self-employment.

For example, if you worked as a hair stylist for five years, then purchased your own hair salon 18 months ago, the lender may be okay with it.

From their perspective, you’re working in the same industry, and even moving up the ladder by starting your own business.

Just note that you will need a signed federal income tax return for the prior year, and the income must be equal to or greater than what you previously made.

Conversely, if you went from being a nurse to running a dog toy startup, one year of tax returns probably won’t cut it.

In this case, you might need to enlist the services of a mortgage broker to shop your loan scenario around, or search for a portfolio lender willing to underwrite you a different way.

Just note that mortgage rates may be less attractive as a result.

You may also be able to get a mortgage if self-employed less than one year, but again, it could be slim pickings and higher-than-market interest rates.

Tips for Self-Employed Borrowers

- Get pre-approved for a mortgage early to avoid any surprises and resolve any issues

- Speak to a knowledgeable mortgage broker to better understand your options

- Make sure your taxes are filed on time so you can use the returns

- Stay organized and keep good business records

- Think about timing of mortgage application if you anticipate changes in your business or employment

- Watch out for lender overlays that limit how much you can borrow

In summary, it’s generally harder to obtain a mortgage if you’re self-employed, but by no means a roadblock.

Lots and lots of self-employed individuals are homeowners, even real estate investors (and agents) who happen to run their own business.

Sure, you might have to provide additional paperwork, and your purchasing power may be more limited based on write-offs and income calculations.

But if you’re financially responsible and keep good records, you shouldn’t have too many issues. Things are getting easier too thanks to technology.

Freddie Mac recently launched its asset and income modeler (AIM) for self-employed borrowers that extracts key income data from a borrower’s tax returns, then plugs it into their automated underwriting system (AUS).

That might lighten the workload, but remember the fundamentals will be the same no matter what.

Strive for excellent credit, set aside money for a healthy down payment, closing costs and reserves, and do your best to earn steadily and dependably.

One last thought. If you’re salaried and thinking about doing the self-employment thing, it might be wise to consider if/when you’ll need a mortgage in the future.

If you’re thinking about refinancing your mortgage or purchasing a property, it might be better to do it sooner rather than later.

Like W-2 borrowers, it’s not wise to jump around to new positions if you know you’ll be applying for a mortgage anytime soon.

- How Mortgage Rates Avoid a Return to 7% - July 24, 2026

- Mortgage Rates Hit New 52-Week High - July 23, 2026

- Light Data Week Means Mortgage Rates Will Be Dictated by Middle East - July 20, 2026