Recently, a friend of mine with an adjustable-rate mortgage told me his rate was set to adjust significantly higher.

His current loan, a 7/1 ARM, has an interest rate of 3.25%, but that’s only good for the first 84 months.

After that, the loan becomes annually adjustable, and the rate is determined by the index and margin.

In case you hadn’t noticed, 30-year fixed mortgage rates have skyrocketed over the past 18 months, climbing from around 3% to 7.5% today.

At the same time, mortgage indexes have also surged from near-zero to over 5%, meaning the loan will adjust much higher if kept long enough.

First Look at Your Paperwork and Check the Caps

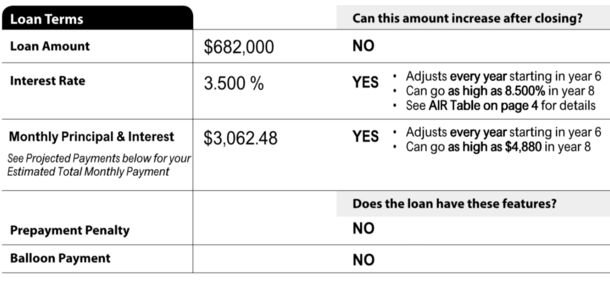

When you took out your adjustable-rate mortgage (ARM) or any home loan for that matter, you were given a Closing Disclosure (CD).

It lists all the crucial details of your loan, including the interest rate, loan amount, monthly payment, loan type, and whether or not it can adjust.

If it’s an ARM, it will indicate that the monthly payment can increase after closing. It will also detail when it can increase and by how much.

There will be a section on page 4 called the “Adjustable Interest Rate (AIR) Table” that provides additional information.

This is probably the first place you should look if you’re unsure of when your ARM is set to adjust, and how much it might rise when it does.

You’ll also find the mortgage index it’s tied to, along with the margin. Together, these two items make up your fully-indexed rate once the loan becomes adjustable.

Let’s Check Out at an Example of an ARM Resetting Higher

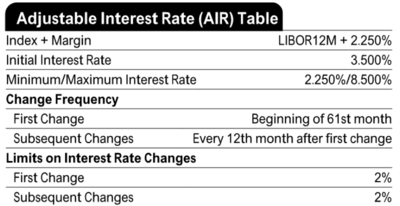

In the AIR Table pictured above, we have a 5/1 ARM with an initial interest rate of 3.5%.

The first adjustment comes after 60 months, meaning the borrower gets to enjoy a low rate of 3.5% for sixty months.

While that sounds like a long time, it can creep up on you faster than you may realize.

After those five years are up, assuming you still hold the mortgage, it becomes adjustable beginning in month 61.

The new rate will be whatever the index is + a 2.25 margin. This CD used the old LIBOR index, which has since been replaced with the Secured Overnight Financing Rate (SOFR).

At last glance, the 12-month SOFR is priced around 5.5%, which combined with 2.25 would result in a rate of 7.75%.

That’s quite the jump from 3.5%. However, there are caps in place to prevent such a massive payment shock.

If we look closely at the AIR Table, we’ll see that the First Change is limited to 2%. This means the rate can only rise to 5.5% in year six.

That’s quite the difference compared to a fully-indexed rate of 7.75%.

And each subsequent increase, such as in year seven, can only be another 2%. So for year seven, the max rate would be capped at 7.5%.

There is also a lifetime cap of 8.5%, meaning no matter what the index does, the rate can’t exceed that level.

Given mortgage rates are already close to those levels, the argument could be made to just keep the original loan, especially when the rate is 5.5%.

The hope is rates improve from these levels at some point within the year and a refinance becomes more attractive.

There’s no guarantee, but there isn’t a ton of downside if the worst your rate will be is 8.5%.

When a Big Adjustment Could Signal the Need to Refinance

But not all caps are created equal. The example above is from a conforming loan with relatively friendly adjustments.

My friend’s caps, which are tied to a jumbo home loan, allow the rate to adjust to the ceiling at the first adjustment.

So there isn’t a gradual step up in rates like there is on the example above. This means the mortgage rate can go straight to the fully-indexed rate, which is the margin + index.

If we assume a margin of 2.25 and an index of 5.5%, that’s 7.5% right off the bat, unlike the lower 5.5% in the prior example.

In this case, a mortgage refinance might make sense, even if the rate is relatively similar. After all, you can get into a fixed-rate mortgage at those prices.

Or pay a discount point and get a rate even lower, hopefully.

And if you’re concerned mortgage rates could go even higher, you’d be protected from additional payment shock.

At the same time, you could still make the argument of taking the 7.5% if refinance rates aren’t much better and hope for improvements in the future.

But you’d have to look at the ceiling rate, which in his case is in the 9% range.

By the way, adjustments can happen in the opposite direction too if the associated index decreases.

To summarize, take a good look at your disclosures so you know all the details of your adjustable-rate mortgage long before it is scheduled to adjust.

That way you can avoid any unnecessary surprises and plan accordingly, ideally before mortgage rates double.

- Can You Get a 4% Mortgage Rate Still? - August 10, 2026

- Mortgage Rates Catch a Break as Job Growth Goes Negative - August 7, 2026

- Mortgage Rates Move Higher on Jobs Report Defense - August 6, 2026