If you’ve been keeping track lately, you might be wondering why mortgage rates plunged this week.

Last week was a totally different story, with a hotter-than-expected jobs report almost enough to push the 30-year fixed across the daunting 8% threshold.

But then the unexpected happened over the weekend, as is often the case with geopolitical events.

In times of uncertainty, bonds are typically a safe haven, and when demand for them rises, their associated yields (or interest rates) fall.

This, coupled with some more dovish talk from Fed speakers, might explain the recent pullback in rates.

How Much Have Mortgage Rates Plunged?

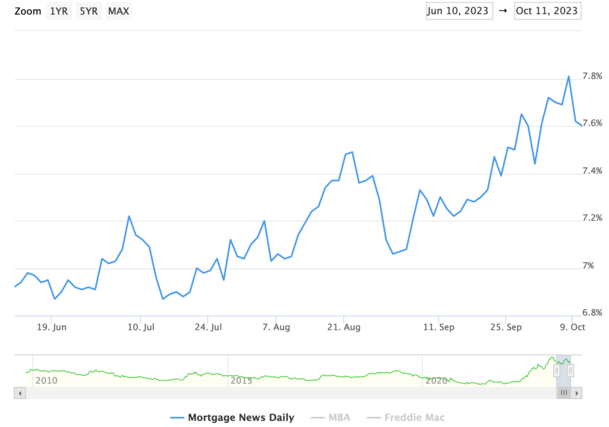

First off, the word “plunge” might be a strong one given how much mortgage rates have climbed over the past 18 months.

While mortgage rates have indeed fallen all week, they remain well above recent lows. And even much higher than levels seen this summer.

If we want to use MND’s widely cited daily rate survey as the measure, the 30-year fixed now stands at 7.60%.

That’s down from 7.81% on Friday October 6th. So basically mortgage rates have improved by about 20 basis points, or perhaps .25% depending on the lender.

It also reduced the year-over-year change in rates from 0.77% to 0.46%, providing a glimmer of hope that the worst could be behind us.

And better yet, perhaps mortgage rates have peaked. While that remains to be seen, it’s been hard to get any meaningful relief lately.

Typically, any pullback or improvement in rates has been met with further increases. And the wins are generally short-lived.

Will that be the case again this time or is there finally light at the end of the tunnel?

Mortgage Rates Helped by New Geopolitical Risks

As for why mortgage rates improved this week, one would be quick to point to the events that took place in Israel (and continue to unfold).

Generally, mortgage rates tend to go down if there is the threat of war or similar tension in the air.

The reason is uncertainty, which is a friend to bonds because of their relative certainty.

In short, investors will flee riskier markets like equities and pile into bonds, which is known as the flight to safety.

If more investors are buying bonds, the price goes up and the yield drops. Since Friday, the 10-year bond yield has fallen from 4.84 to about 4.61 today.

Of course, this could prove to be a short-term reaction to what has been a clear move higher for bond yields lately.

So it’s entirely possible that the 10-year yield marches on back to those recent levels (and beyond) depending on what transpires.

And the conflict in the Middle East could actually exacerbate inflation if oil prices (and gas prices) rise.

No More Fed Rate Hikes Could Take Pressure Off Mortgage Rates

Another factor related to the recent mortgage rate plunge has been some dovish talk from Fed officials.

Atlanta Fed President Raphael Bostic came out this week and basically said no more interest rate hikes were needed.

The Fed has already raised its key policy rate 11 times since early 2022, pushing mortgage rates up along with it.

But Bostic “told the American Bankers Association that Fed policy is sufficiently restrictive.”

Additionally, he said rate cuts could even be in the cards “if things get ugly in the Middle East.”

“You can pretty much count on the Fed taking that into its world view and that’s only going to be lower rates.”

Earlier in the week, Dallas Fed President Lorie Logan said higher bond yields could do the heavy lifting for the Fed, requiring no additional tightening on their part.

And Fed Vice Chair Jefferson made comments that suggested he was in favor of pausing the fed rate hikes.

Interest rate traders have taken that to mean that the Fed rate hikes could be over, and the next move might be lower.

Per the CME FedWatch Tool, that cut could come by the June meeting, based on the current odds.

Though if the situation worsens in the Middle East, cuts could materialize even earlier in 2024.

As it stands now, another rate hike looks exceedingly unlikely, while a rate cut appears to be coming sooner-than-expected.

Now it’s important to note that the Fed doesn’t control mortgage rates, but their long-term outlook can have an effect on mortgage rates.

Fed Clarity Can Lower Bond Yields and Narrow the Spread

Additionally, more clarity from the Fed could go a long way in fixing the spread between 10-year bond yields and mortgage rates.

It’s currently about double its usual amount, at around 300 bps vs. 170. Knowing the Fed’s position on monetary policy could normalize spreads.

If we assume the 10-year bond yield settles in at current levels of say 4.50%, adding a more typical spread of 200 bps puts the 30-year fixed back to 6.50%.

That would spell relief for many prospective home buyers, who might be facing mortgage rates as high as 8% depending on their individual loan attributes.

Factor in paying mortgage points at closing, and it’s possible home buyers could obtain mortgage rates back in the high-5% range.

That would likely be good enough for now to get transactions flowing again, and potentially unlock some existing homeowners trapped by so-called mortgage rate lock-in.

Just beware that the trend has not been friendly to mortgage rates for a long time, and things can easily reverse course again depending on what transpires.

While it might signal a turning point, mortgage rates can also remain stubborn at these levels without significant economic data pointing to lower inflation.

And tomorrow’s CPI report alone could completely reverse the big move lower over the past couple days.

So while we’ve gotten some relief over the past few days, this so-called mortgage rate plunge may easily unwind if more hot economic data comes in. Or if global tensions ease.

(photo: Pussreboots)

- Mortgage Rates Catch a Break as Job Growth Goes Negative - August 7, 2026

- Mortgage Rates Move Higher on Jobs Report Defense - August 6, 2026

- Mortgage Rates Are Now Higher Than They Were a Year Ago - August 5, 2026