Back in 2009, the government launched the Home Affordable Modification Program (HAMP) to help struggling homeowners keep up with their out-of-control mortgage payments.

The program offered all types of solutions to reduce borrowers’ monthly mortgage payments to 31% of their gross monthly income, including interest rate reductions (to as low as 2%), loan term extensions, and principal balance reductions.

But there was a caveat. Five years after the modification, homeowners who received reduced interest rates would face rate resets.

And seeing that it’s 2014, the very first batch of these rate resets is soon to go live.

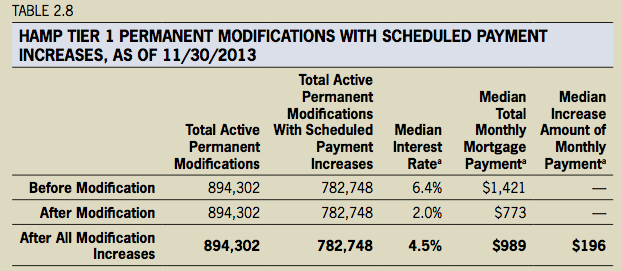

Of the 894,302 homeowners with active HAMP permanent modifications, an overwhelming 88% are scheduled to have mortgage rate increases, according to a new report from the Office of the Special Inspector General for the Troubled Asset Relief Program (SIGTARP).

The increases will take place between 2014 and 2021, and will rise incrementally by up to 1% each year until reaching the national average rate for a conforming 30-year fixed-rate mortgage on the date of the original modification.

The average 30-year fixed rate over the past five years has hovered between 4% and 5.4%, so those enjoying 2% mortgage rates will be in for quite a surprise.

Someone’s Monthly Mortgage Payment Will Go Up $1,724

- While HAMP was created to make monthly mortgage payments affordable

- The loan modifications came with rates that weren’t set in stone

- The good news is that the median payment increase is just $196

- Which when coupled with the savings the first several years should still be a net benefit to the homeowner

In fact, the maximum monthly payment increase after all the incremental increases will be $1,724 for an unlucky California homeowner.

But Hawaii boasts the highest monthly median payment increase after all rate adjustments at $356. California came in a close second at $297.

While that sounds pretty bad, the median payment increase after all adjustments will only be $196, which will typically take several years to achieve.

So it shouldn’t be a major payment shock for most homeowners, though it could lessen their incentive to stick around.

My guess is that some homeowners facing higher monthly payments will think about selling their properties, assuming they’ve appreciated enough.

And others will probably look to refinance their modified loans, though the modified rate should still be pretty favorable compared to the going market rate.

Apparently lenders are okay with refinancing modified loans so long as the borrower kept up with payments for the past two years. My guess is leniency will prevail in the face of lower mortgage application volume…

Four States Account for Half of HAMP Payment Increases

- Most of the homeowners affected by payment increases

- Reside in the states of California, Florida, Illinois, and New York

- This could dampen the housing recovery in those areas

- Especially for those seeing monthly payments jump $1,000+, though it could prompt more refinancing too

It won’t be much of a nationwide epidemic though. Just four states account for half of the homeowners with permanent HAMP modifications scheduled for interest rate increases.

They include California, Florida, Illinois, and New York.

This could dampen the recovery that has taken place in these states, especially with so many HAMP modifications performing poorly.

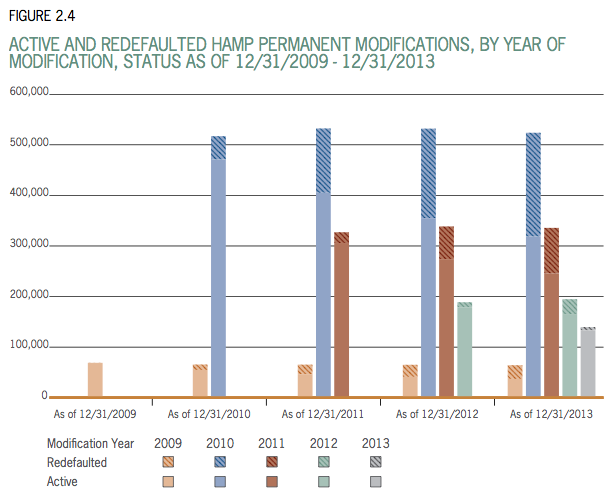

As of December 31, 2013, 359,072 homeowners, or 28% of all participants who received a permanent HMAP modification, fell three months behind on payments and thus redefaulted out of the program.

And the older HAMP modifications appear to be doing even worse. For HAMP modifications received in 2009, the redefault rate ranged from 43% to 49.6%.

For 2010 HAMP modifications, 32.4% to 41.9% had redefaulted as of November 30, 2013.

The largest HAMP payment increases will affect homeowners in California, Hawaii, Maryland, Massachusetts, Nevada, New Jersey, New York, Virginia, Utah, Washington, and Washington, DC.

And the highest mortgage payment any HAMP borrower will pay after all the interest rate increases will be a whopping $9,966.

- Rocket Mortgage Completes Redfin Takeover, Offers $6,000 Home Buyer Credit - July 1, 2025

- Mortgage Rates Quietly Fall to Lows of 2025 - June 30, 2025

- Trump Wants Interest Rates Cut to 1%. What Would That Mean for Mortgage Rates? - June 30, 2025

Colin Robertson:

We had a pick-a-pay mortgage since 2006 with Metrocities LLL DBA No Red Tap Mortgage.Can you help us.?The mortgage rates in 2008 went to 3.5% that Aurora Mortgage(our new servicer in 2008) reduced our principal balance every time we made an Interest Only Payment. The Adjustable Rate Note says on page 3 of 6 (H) Payment Options: (i) Interest Only Payment: the amount that would pay the interest portion of the monthly payment at the current interest rate.THE PRINCIPAL BALANCE WILL NOT BE DECREASED BY THIS PAYMENT OPTION.In my opinion our note was changed without our permission. Isn’t this a breach of contract? I talked with Aurora and was told that the interest rates are so low that they ,Aurora,decided to add the interest payment to the principal balance because they did not know what to do with the extra or surplus money and it caused our principal balance to go down.What action can we take? Now we have Nationstar Mortgage. And they continue to do the same thing.Am I complaining? Yes.We want our money back or what ever we can do.

Thanks,

To get this straight, you make interest-only payments each month and the bank pays DOWN your principal balance (what you owe)? If that’s the case, it’s a great deal. Why would you be upset with your loan balance dropping when it originally shouldn’t be with IO payments?

I refinanced back in 2010, and my economic situation has greatly changed since then, my current rate is now close 5.75 40 YEARS!, I wanted to see if I should be able to refinance now, I am not looking to decrease payment amount but term, perhaps a fixed 15 years. However, my bank was telling me that if part of my mortgage was forgiven, they won’t even consider a refi…..is this standard for all banks, as a family we now make double what we made in 2010, our credit is good, and have stable jobs, why would banks do this specially since amount forgive was only 40k, (that a very low reduction here in Northern California)

Karen,

Things can get tricky when attempting to refinance a modified loan with principal reduction. Most banks may have a waiting period after the modification, and there may also be issues with the forgiven amount vs. the outstanding amount and how it’s treated in the refi. You may want to shop around and see who offers what for your situation, as options may vary. If they say they can’t do it ask why.

Can you tell me the interests rates and schedule for interest rate changes for HAMP modifications that occurred in August 2010?

My wife received a HAMP modification with a Principal Reduction in May 2012 from Chase. The reduction was very significant (2/3 of the original loan) and the reduction period ends May 2016. The current rate is 2% but will increase after year 5. I have read the contract but it doesn’t state any where when the reduction becomes permanent. She would like to refinance near the five year mark but not certain if that is possible. Any suggestions other than calling the lender for this info?

Chad,

Probably best to speak with your servicer or Chase to get the right info instead of speculating.

If a person had a HAMP, done in 2009 (with terms of original mortgage kicking back in in 2014), and then that loan was modified (from original ARM terms to a FIXED rate), is that considered ‘forgiveness’? No late payments that were forgiven, no principal balance forgiven, rate was just permanently reduced. Fannie guides say any forgiveness of principal and/or INTEREST then requires a 2 year wait period. My argument is INTEREST was NOT forgiven, interest had not accrued and was not due. I get it if past due payments were forgiven, because that payment include principal AND interest, so if that interest was not collected, it was forgiven, but seems like a simple rate reduction should not be considered as forgiveness of interest.

Scott,

May want to shop around to see why it can’t be done or if it’s just the lender you’re speaking with that can’t help.

I moved out of my home in 2009.. (left the home with my ex) my name was still on the loan/deed.. he did a loan modification through HAMP.. he sold the house in 2011. I’m now trying to purchase a new home.. but the lender refused me.. because of the last mortgage is showing on my credit report as modified.. even though all payments showed as current and my credit score is 789.. I was under the impression once the property sold it wouldn’t affect any future mortgage loans? Is there a way around this? Has anyone else ran into this problem? I don’t have any paperwork from the modification..and I’m not sure who he went through because I had no idea my ex did this.. until afterwards! Anyone have contact information for HAMP?? Or should I contact GMAC? I don’t want to lose this home because I can’t get financed

Michelle,

Problem is the loan mod is on your credit report so the sale of the home doesn’t really change that. It sounds like it has been several years though so maybe determine the waiting period the lender after loan mod and find one that will help you.

We had a loan modification back in 2013, my documents state a rate reduction and a principal reduction amount, which was put into a subordinate mortgage and note. I’ve been doing some research and it appears after three years (which would be this February) that reduced amount is extinguished. Is this correct? I cannot seem to get an exact answer on if I have to pay it when/if I sell my house, or if after the three years, it is reduced permanently.

Stephanie,

It depends on the terms of your modification. Check the paperwork and/or call the servicer that offered it to see what the terms say.

I am modifying my loan, I was approved 4 month trial, and preservation specialist advised, my loan was extended for 30 years again and interest rate was reduced, does this sound correct?

Maria,

Not sure what you’re asking but it’s common for modifications to lower the interest rate and extend the loan term to reduce monthly payments.

I just sold my home and I have a HAMP borrower incentive accrued amount of $166.66. Will I receive that?

Thanks

Scott,

Not sure, probably best to reach out to whomever has been sending you checks.

in Oct 2013, we had a trial period for a loan modification and if we paid on time for 3 months, in January we would be approved for a loan modification. We got approve and in January 2014, we had a loan modification with principal reduction and non-interest bearing principal forbearance and interest reduction for the term of our existing loan. Our interest went down to 2.625% for the entire loan. We originally bought the house in 2006 and our maturity date on our loan is Nov 2036. From what our contract says, our deferred principal balance due will be $0 after 10/1/2016. They reduced the deferred principal balance by 1/3 each year. So now that my principal balance is lower and I have equity, am I able to get a Home Equity Loan or HELOC? Do you know if I sell my home, do I have to pay back the principal forbearance or does that only apply to the first three years? The contract is not clear on that.

Hi Dana,

I’m not sure, but a lender offering a HELOC may be able to provide guidance. Some banks may approve it while others may not depending on their guidelines. Also not sure what contract stipulates about a home sale and the forgiveness. Sorry I can’t be of much help.

Has anyone received their 5000.00 reduction off their principal yet?

Interesting question re: the promised $5000 reduction on principal. I am in a modification and am very nervous about the next increase. The $5000 will help should I be able to refinance to keep my home. I have not seen it yet but plan on calling them next week to inquire.

It worked for me. I just opened my March mortgage statement and saw that a $5,000 credit has been applied to my principal.

We to had our 2006 home loan modified under a HAMP modification. To a 2.0% fixed rate for the first 5 years then 3.0% for the next year. And then 4.0% for a year and caps out the following year at 4.5% or less if the interest rate is not at least 4.5% at that time for the remainder until 2036. We received the $1,000.00 off the principle of our loan at the end of each year for paying on time and then at the end of the first five years we received and additional $5,000. off of our principle in a lump sum equaling at total of $10,000.00 off our principle for paying on time. But ours had a extra incentive for we also paid every month and extra 5% on our principle of our loan that then gave us the $1,000. at the end of each year. Additionally if we continue our loan is gauge to reduce our principle faster with lump sum reductions at the end of each year. Sounds great but if we ever get behind all the extra after the first five year they then take back! We have never been behind on a house payment since our first home I’m now 53. With a little luck we never will be either. But Yes we received our $5,000. in a lump sum removed from our home loan, but as I wrote in our case after the first 5 years ours totaled $10,000. off our principle had been removed from the HAMP Mod. seems most peoples mods. are all a little different based on different factors. I myself became disabled from a Kidney disease in the early 2000’s also and on a very limited income since I’m to young to be allowed to touch my retirement or vested retirement and if I did Taxes & penalties would eat nearly 1/4 of it straight away any how. So trying to make it past 55 and at least to age 65 before touching that.

Sorry to clarify better the above should have started off saying our original 2006 home loan was modified 6 months after the HAMP program came out and we were accepted in 2009. I hope my gibberish made some sort of sense. Take care.