You may have heard the phrase “payment shock” get thrown around by your loan officer or mortgage broker, and for good reason.

It plays an important role in the underwriting and eventual outcome of your mortgage application, and can sometimes even make or break your chances of approval.

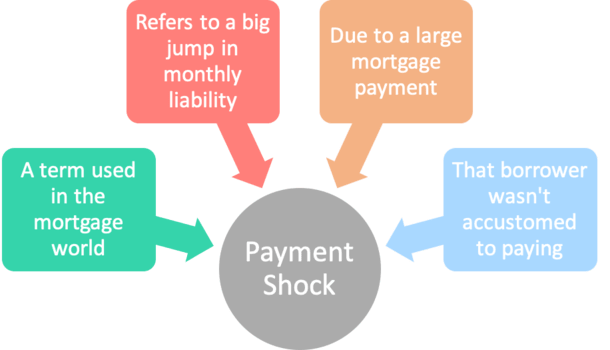

Payment shock can be defined in a number of ways, but it is essentially any significant increase in monthly liability that heightens the risk of loan default.

In simple terms, the more you need to pay out each month to creditors, the higher the chance you’ll be unable to make a payment, especially if you’re not used to making large payments to begin with.

Payment Shock Example

Let’s assume your only history of carrying debt involves a car lease payment of $199 per month and rent of $1,000.

Over the past few years, you got used to paying roughly $1,200 per month, plus other minor expenses.

If you later applied for a home loan that carried a monthly payment of $4,000, payment shock would occur as you wouldn’t be used to shelling out such a large amount of money each month.

Would you be able to handle paying $4,000 per month when you were only accustomed to paying $1,200? This is what the loan underwriter will want to figure out.

This jump in monthly outlay could be reason enough to get denied that mortgage you’ve got your eye on.

Payment Shock Threshold

- Might be a set payment increase

- Such as 200% of current housing payment

- Meaning if your proposed payment more than doubles

- You could be ineligible without an exception

Some banks and mortgage lenders have a certain payment shock threshold that they allow, which can be dependent on things like credit score, documentation type, and other factors.

Typically, max payment shock may be set at 200%, meaning your monthly mortgage payment can be no more than double your current housing payment.

So if you currently pay $1,000 in rent each month, your max mortgage payment cannot exceed $2,000, or it may be subject to review or denial.

This is why credit history (and housing payment history) is so important, as it proves your ability to repay loans and carry large amounts of debt over time.

To those with little established credit will often face a series of hurdles when looking to get approved for a home loan (or any other type of loan) because they haven’t demonstrated the ability to handle large monthly payments.

This can be especially true for those living at home with mom and dad who have no prior rental history.

ARM Payment Shock

- It’s also possible to experience payment shock on an adjustable-rate mortgage

- ARMs mostly adjust higher once the fixed period ends

- You may need to qualify at a higher interest rate than the start rate if you take out an ARM

- This shows the underwriter/bank you’re able to absorb higher payments if and when your loan adjusts

Payment shock can also apply to specific home loan programs, such as hybrid adjustable-rate mortgages that start with a low initial teaser rate and have the potential to reset to much higher rates once the fixed period ends.

A perfect example of this was the once popular option arm, which typically began with a 1% start rate that could quickly jump up to a mortgage rate of 8% or higher.

In this case, the borrower would experience payment shock for the sheer fact that the minimum monthly payment would increase exponentially.

Nowadays, a Fannie Mae requirement calls for borrowers with ARMs that have an initial fixed-rate period of five years or less to be qualified at the greater of the start rate plus 2%, or the fully indexed rate.

For example, if a 5/1 ARM is priced at 2.5%, the borrower will have to qualify at a rate of at least 4.5%. In other words, you can’t use the ARM’s lower start rate to your advantage when it comes to your debt-to-income ratio.

Individual lenders may also have their own minimum qualifying guidelines that are applied depending on the loan type. I’ve seen 3/1 ARMs that call for a qualifying rate of 6% above the start rate…ouch!

Can You Qualify at the Fully Indexed Rate?

- ARMs are no longer for those struggling to make payments

- It might be tougher to qualify vs. a fixed-rate mortgage

- So make sure you can handle the fully-indexed rate

- Or you might have to go with a different loan program

At minimum, mortgage underwriters typically qualify borrowers at the higher fully-indexed rate to determine if they can actually handle those mortgage payments once the loan resets.

Most borrowers can afford the ultra-low 1% start rate, but not everyone may be able to keep up with the housing payment associated with an interest rate of 7-8%.

So it’s important to ensure that applicants are qualified for both housing payments.

That being said, not everyone will be declined for a mortgage simply because of payment shock. If you can prove that you’re a sound borrower on other fronts, such as by demonstrating the ability to save money, you might get a pass.

Same goes for those who are able to establish a solid credit history early on, which will prove both their ability to make on-time payments and carry large amounts of debt.

[What credit score do I need to get a mortgage?]

Conversely, if you have poor credit, you may need to come up with strong compensating factors, such as the ability to put more money down or document substantial income and assets that prove you’re a worthy borrower regardless of any increase in payment.

Tip: Make sure you can document at least 12 months of housing payment history made prior to your mortgage application. It can eliminate some of the uncertainty on the proposed housing payment front.

- Mortgage Rates Could Drop as Much as Half a Percent with Basel Re-Proposal - June 30, 2026

- Mortgage Rates Face Big Week of Jobs Data - June 29, 2026

- Are Mortgage Rates Finally Poised to Start Falling Again? - June 25, 2026