Mortgage Q&A: “What are mortgage points?”

The mortgage process can be pretty stressful and hard to make sense of at times, what with all the crazy terminology and stacks of paperwork.

Further complicating matters is the fact that banks and lenders do things differently. Some charge so-called loan application fees while others ask that you pay points. Then there are those that tack on lender fees and points.

While shopping for a home loan, you’ll likely hear the term “mortgage point” on more than one occasion.

Jump to mortgage point topics:

– How Much Is a Mortgage Point

– How Do You Calculate Points on a Mortgage?

– There Are Two Types of Mortgage Points

– Paying Mortgage Points for a Lower Interest Rate

– How Do Negative Points Work on a Mortgage?

– Mortgage Point Examples

– Mortgage Points Cost Chart

Be sure to pay special attention to how many points are being charged (if any), as it will greatly affect the true cost of your loan.

How Much Is a Mortgage Point?

- It’s just another way of saying 1% of the loan amount

- So for a $100,000 loan one point equals $1,000

- And for a $200,000 loan one point equals $2,000

- The higher the loan amount, the more expensive a point becomes

Wondering how mortgage points are calculated? Don’t worry, it’s actually really easy. You don’t even need a mortgage calculator! Or a so-called mortgage points calculator, though I’ve got one to make your life that little bit easier…especially for the break-even calculation!

When it comes down to it, a mortgage point is just a fancy way of saying a percentage point of the loan amount.

Essentially, when a mortgage broker or mortgage lender says they’re charging you one point, they simply mean 1% of your loan amount, whatever that might be.

How do you calculate points on a mortgage?

So if your loan amount is $400,000, one mortgage point would be equal to $4,000. If they decide to charge two points, the cost would be $8,000. And so on.

If your loan amount is $100,000, it’s simply $1,000 per point. It’s a really easy calculation. Just multiply the number of points (or fraction thereof) times the loan amount.

If it’s one point, take a calculator and input .01 multiplied by the loan amount. If it’s 1.5 points, input .015 multiplied by the loan amount.

Using $300,000 as the loan amount in the above equation, we’d come up with a cost of $3,000 and $4,500, respectively.

Assuming you’re being charged less than a point, we have to consider “basis points,” which are one one-hundredth of a percentage point (0.01%). Put another way, 100 basis points, or bps as they’re known, equals one percent.

For example, if you’re only being charged half a point, or 50 basis points, you’d calculate it by inputting 0.005 into a calculator and multiplying it by the loan amount.

Again, no basis points calculator needed here if you can manage basic math.

Using our loan amount of $100,000 example, a half point would equate to $500. If you were charged 25 basis points (0.25%), it’d be $250, and you’d calculate it by entering 0.0025.

Don’t get thrown off if the loan officer or lender uses basis points to describe what you’re being charged. It’s just a fancy way of saying a percentage of a point, and could actually be used to fool you.

As you can see, the cost of a mortgage point can vary greatly based on the loan amount, so not all points are created equal folks.

Tip: The larger your loan amount, the more expensive mortgage points become, so points may be more plentiful on smaller mortgages if they’re being used for commission.

There Are Two Types of Mortgage Points

- The word “points” can be used to refer to two completely different things

- Either the loan officer or mortgage broker’s commission for providing you with the loan

- Or discount points, which are entirely optional and can lower your interest rate

- Know what they’re actually charging you for to ensure you make the correct decision

There are two types of mortgage points you could be charged when obtaining a mortgage.

A mortgage broker or bank may charge mortgage points simply for originating your loan, known as the loan origination fee. This fee may be in addition to other lender costs, or a lump sum that covers all of their costs and commission.

For example, you might be charged one mortgage point plus a loan application and processing fee, or simply charged two mortgage points and no other lender fees.

Additionally, you also have the choice to pay mortgage discount points, which are a form of prepaid interest paid at closing in exchange for a lower interest rate and cheaper monthly payments.

They are used to buy down your interest rate, assuming you want a lower rate than what is being offered. Generally, you should only pay these types of points if you plan to hold the loan long enough to recoup the upfront costs via the lower rate.

You can use a mortgage calculator to determine how many monthly mortgage payments it’ll take for buying points to make sense. This is essentially how long you need to keep the home loan to come out ahead.

Paying Mortgage Points for a Lower Interest Rate

- It’s important to consider both the loan type your expected tenure

- To determine if paying points upfront is a good deal

- Generally worth looking into if you plan to stick with your mortgage/property for a long time

- And if you want an even lower fixed rate you’ll actually benefit from for years to come

It would probably make more sense to pay mortgage points on a 30-year fixed as opposed to an adjustable-rate mortgage, seeing that you could benefit for many more months, though both situations could make sense depending on the price and associated discount.

Same goes for the homeowner who plans to stay in the property for years to come. Seeing that you’d save money each month via a lower housing payment, the more you stay the more you save.

Another plus is that these types of points are tax deductible, seeing that they are straight-up interest. And that tax benefit should be factored into the equation

*The loan origination fee may also be tax deductible if it’s expressed as a percentage of the loan amount and certain other IRS conditions are met.

If you aren’t being charged mortgage points directly (no cost refi), it doesn’t necessarily mean you’re getting a better deal.

All it means is that the mortgage broker or lender is charging you on the back-end of the deal. There is no free lunch.

In other words, the lender is simply offering you an interest rate that exceeds the par rate, or market rate you would typically qualify for.

So if your particular loan scenario had a par rate of say 4.25%, but the mortgage broker or bank could earn two mortgage points on the “back” if he/she convinced you to take a rate of 4.875%, that would be their yield-spread-premium (YSP), or commission.

Before this practice was outlawed, it was a common way for a broker to earn a commission without charging the borrower directly. Nowadays, brokers can still be compensated by lenders, but it works a bit differently.

They have to select a compensation package with each lender they work with beforehand so all borrowers are charged the same flat percentage rate.

Of course, they can still partner with three different wholesale banks and select varying compensation packages, then attempt to send borrowers to the one that pays the most. Yet another reason to be sure you negotiate!

Banks can offer mortgages without points as well because of the “service release premium†(their form of YSP), which is a fee they earn when they sell their loans to other companies on the secondary market.

Sure, you might not pay any mortgage points out-of-pocket, but you may pay the price by agreeing to a higher mortgage rate than necessary, which equates to a lot more interest paid throughout the life of the loan assuming you keep it for a while.

How do negative points work on a mortgage?

- Some lenders may offer so-called negative points

- Which is just another way of saying a lender credit

- These points raise your interest rate instead of lowering it

- But result in a credit that can cover closing costs so you don’t pay them out-of-pocket

If points are involved and you are offered a higher rate, the mortgage points act as a lender credit toward your closing costs. These are known as “negative points” because they actually raise your interest rate.

Now you might be wondering why on earth you would accept a higher rate than what you qualify for?

Well, the trade-off is that you don’t have to pay for your closing costs out-of-pocket. The money generated from the higher interest rate will cover those fees.

Of course, your monthly mortgage payment will be higher as a result. How much higher depends on the size of your loan amount and the points involved.

This works in the exact opposite way as traditional mortgage points in that you get a higher rate, but instead of paying for it, the lender gives you money to pay for your fees.

Both methods can work for a borrower in a given situation. The positive points are good for those looking to lower their mortgage rate even more, whereas the negative points are good for a homeowner short on cash who doesn’t want to spend it all at closing.

Let’s look at some examples of mortgage points in action:

Say you’ve got a $100,000 loan amount and you’re using a broker. If the broker is being paid two mortgage points from the lender at par to the borrower, it will show up as a $2,000 origination charge (line 801) and a $2,000 credit (line 802) on the HUD-1 settlement statement.

It is awash because you don’t pay the points, the lender does. However, a higher mortgage rate is built in as a result of that compensation to the broker.

Now let’s assume you’re just paying two points out of your own pocket to compensate the broker. It would simply show up as a $2,000 origination charge, with no credit or charge for points, since the rate itself doesn’t involve any points.

You may also see nothing in the way of points and instead an administration fee or similar vaguely named charge.

This could be the lender’s commission bundled up into one charge that covers things like underwriting, processing, and so on.

It could represent a certain percentage of the loan amount, but have nothing to do with raising or lowering your rate.

Regardless of the number of mortgage points you’re ultimately charged, you’ll be able to see all the figures by reviewing the HUD-1 (lines 801-803), which details both loan origination fees and discount points and the total cost combined.

*These fees will now show up on the Loan Estimate (LE) and Closing Disclosure (CD) under the Loan Costs section.

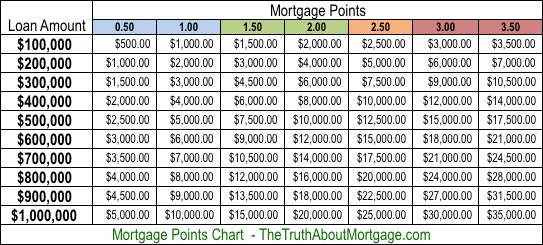

Mortgage Points Cost Chart

Above is a handy little chart I made that displays the cost of mortgage points for different loans amounts, ranging from $100,000 to $1 million.

As you can see, a mortgage point is only equal to $1,000 at the $100,000 loan amount level. So you might be charged several points if you’ve got a smaller loan amount (they need to make money somehow).

At $1 million, you’re looking at $10,000 for just one mortgage point. And you wonder why loan officers want to originate the largest loans possible…

Generally, it’s the same amount of work for a much bigger payday if they can get their hands on the super jumbo loans out there.

Be sure to compare the cost of the loan with and without mortgage points included, across different loan programs such as conventional offerings and FHA loans.

And remember that points can be paid out-of-pocket or priced into the interest rate of the loan.

Also note that not every bank and broker charges mortgage points, so if you take the time to shop around, you may be able to avoid points entirely while securing the lowest mortgage rate possible.

Read more: Are mortgage points worth paying?

- Do Mortgage Rates Need a Hike to Move Lower? - July 28, 2026

- How Mortgage Rates Avoid a Return to 7% - July 24, 2026

- Mortgage Rates Hit New 52-Week High - July 23, 2026

I recently purchased my first home and on the HUD-1 form there is nothing on line 802 with and origination fee listed on 801 and 803 (identical). However, I did receive a 1098 from the lender list a point paid for the purchase, so do you know what is doing on here? Am I getting changed points first in the origination fee and then again on a deal with the lender?

Phil, line 801 is the origination charge, and line 803 is your adjusted origination charge. They were the same, not double, because you didn’t pay discount points or receive a lender credit, which is why line 802 is blank.

Thanks for breaking it down. I thought you always had to pay points out of pocket no matter what.

It seems to me that paying a mortgage point does very little to actually lower your interest rate. My broker told me I had to pay a full point just to lower the rate .25%. Doesn’t seem to be a very good deal.

I recently purchased a home and received a lender credit of approx. 10K. They charged an orig. fee of $6400, leaving me with an adjusted orig fee of -approx $3600 (credit). I am allowed to claim reimbursement for my move for “expenses actually incurred” to include orig. fee. I’m told this fee is not going to be allowed since I got a credit and did not incur the expense. Although I am allowed to be reimbursed commision on the sale of a property (because it “affected my bottom line”) I was told. Didn’t the orig fee also affect my bottom line using this line of thinking? I know I didn’t write a check at closing, but didn’t I still get charged $6400? Thanks for helping me understand if my though process is crooked.

Bob,

Yes, it sounds like you were charged $6,400 for taking out the loan, though you didn’t actually pay it out-of-pocket. It was covered via the lender credit, and the presence of the credit resulted in a higher-than-market interest rate in return. However, I’m not sure how the military defines “expenses actually incurred,” or reimbursements for that matter.

I was recently charged 2.5 points for my refinance, so it pays to read your loan paperwork and comparison shop. I think I could have done a lot better. Note: They didn’t charge me any other fees, so I guess that was the tradeoff.

Is there a customary number of mortgage points one should pay when taking out a mortgage? Like an average? Thanks.

If you’re talking about mortgage points for commission, many banks will charge 1 point. However, as noted in the post, depending on the size of the loan, lenders may need to charge more or less to cover their costs and make money. And some may charge no points directly to the borrower. So it really depends. Just look for the best combination of points, rate, and fees to ensure you’re getting the best deal.

My broker said he wasn’t charging me any points, but I still see loan origination charges and a negative number in the adjusted charges section of the Good Faith Estimate.

It appears as if you were charged points, but they’re covered by credits, meaning you didn’t pay for them out of pocket. But again, took a higher interest rate to compensate.

Line 801 lists an origination charge of 13650

Line 802 lists a credit of 12510

Line 803 lists adjusted origination charge of 1140

What can I write off the full 13650 or only what the adjusted origination charge lists?

No one seems to have a straight answer on this, but hopefully a tax expert or your CPA can provide a definitive answer. Some say you can use adjusted origination, but if that figure includes things like processing and underwriting fees, those aren’t really points. For the record, the credit results in a higher interest rate, meaning more interest will be paid by you over the life of the loan and potentially deductible each year you pay your mortgage. There’s a lot of confusion about this from what I’ve seen and even the IRS doesn’t seem to explain it very well.

Colin,

If we refuse the credit does that require the bank/lender to reduce the interest rate and disclose the reduced rate? We applied for a refinance 4 months ago with our current bank/lender and the credit was higher when we received the original GFE but were told that because the extended duration (not because of the borrower; both have excellent credit and bank with the lender) that the rate and amounts changed and the credit is less. The interest rate remains 4%/3.956% APR.

Original:

801: $955

802: $2,718.24

803: $1,763.24

New:

801: $955

802: $2,431.71

803: $1,476.71

Hey Willie,

That’s normal. Rates and credits can change day to day as the market dictates. You can ask what your interest rate would be without the credit. But if it doesn’t lower your rate, or it only does so marginally, you might also consider using it to offset closing costs. Ask them to present a few scenarios with and without the credit and go from there.

Can you make sense of this? We’re refinancing — getting a lower rate and shorter payoff time — and hitting the fee questions. “Locked in” at 3.125 percent APR, supposedly, a week or more ago.

We were told: “We can renegotiate rates, but only when they drop by a full point”

I asked what that meant:

“Can you clarify what a “point” is, for “drop by a full point” and where I can see that?

Is that a percent of the loan amount, or a percent of the APR, or something else?

I see a “basis point” published — quoted below — that’s something different?

Do we need to watch the point rate and alert you if there is that much change? Or will you be watching for us and revise the rate if that “full point” change occurs?”

The reply I got was utterly vague:

“Sorry of the “mortgage speak”

I can watch for the change for you.

Rates have not changed that dramatically since we locked you in.

— Loan Officer

Hank,

1 percentage point = 100 basis points. Put another way, a basis point is 0.01. A mortgage point is 1% of the loan amount. Then there are mortgage rates, such as 3.125%, which could rise to 4.125% or fall to 2.125%.

People generally lock when they are happy with the offered rate. They don’t lock only to renegotiate later, otherwise they’d probably float and lock later. However, there are sometimes float downs offered that allow borrowers to take advantage of pricing improvements, though I don’t know if that is what is being offered to you. And those still tend to come with a cost. Ask for clarification.

I was just given a quote from a lender that included points but he told me the lender credit would cover the points. I have another lender I am working with and he told me that it was illegal to give a lender credit for points. I can’t find anything to prove one way or another. Any advice?

Kristin,

What exactly is illegal? Ask for clarification. They probably just mean an originator can’t be paid by both the lender and the borrower.

Kristin,

Technically, an originator cannot be paid by both the lender and the borrower but lender credit is common practice. Lenders give credits to offset the closing costs and this comes with higher rates.

Was told by my lender that they don’t control points but are set by Fannie Mae. Said they don’t charge points on loans they keep in-house. True?

Jared,

The prices for certain rates may be determined by an investor but they can control what they charge the customer in the way of points.

I was quoted on a 248.000 home loan a rate of 4.375 and 2 points. This was on an estimated closing statement. I feel that 2 points is high.

Steven,

Options are to shop around or try to negotiate lower cost.

I broker told me that when buying points, the 1st point will reduce the rate by 1/4, but additional points purchased will reduce the rate by 1/8, or less? Does this make sense? He told me that if i bought 3 points on a 388,000 mortgage it would reduce the rate 3/8. They are only charging total origination fees of $1,390 after they waived the application fees of $300 and funding fee of $250, which seems very low. I was told I was given a discount on the fees because the firm I work for sends him a lot of business. Thanks for your help.

Jim,

Not sure it’s an exact science…depends on the interest rate you’re looking to buy down to, the lender you’re working with, etc…he may be ballparking and kind of nudging you that’s it not worth paying at a certain point. Ultimately, it’s your decision in terms of what you feel is worth buying down down to if at all and you need to do the math to see the break-even periods for certain buy downs.

We purchased a home June 2015, our loan company did not list “points” on our documents but there is a closing fee, loan processing fee, underwriting fee and upfront MIP. Are these amounts tax deductible?

Rachel,

Generally only prepaid interest (discount points) are tax deductible. As far as upfront MIP, I believe there is an 84-month formula to deduct the cost assuming you qualify/itemize. Probably best to consult a tax specialist.

We recently purchased a new house. Our lender said that she would “watch” the rates and if a lower one came up with in the next 6 months, she would automatically drop us to that rate. However, they sold our loan, so how would she be able to lower our rate if the loan is no longer with her company? Did she lie?

Suzy,

Just means they’ll refinance you again if rates are favorable, doesn’t matter that the current loan was sold…once six months have passed her commission is likely secure and she can refi you again regardless of what company now owns the loan.

We are refinancing our home and signed papers for percentage lock and fees. The points charged first was 0.5 points for 218,000 loan. Now we receive the paper work again because our payoff is lower and noticed the points were upated to 2.5 without letting us know. Is this allowed or legal?

Martha,

Have you asked why the points jumped up from 0.5 to 2.5? It might depend on if material changes took place, such as higher loan-to-value, etc.

I am considering purchase of a new home that falls into the “super conforming” jumbo category here in Suffolk, NY ($615,000…). One bank offered several mortgage point options in a personal online quote but during our in-person meeting indicated that there is a Federal or State maximum amount the bank is allowed to charge to buy back points (in this case 2.5 points for this loan amount).

I couldn’t find that regulation anywhere and am wondering if its just a specific bank policy or this particular mortgage agents policy!!!

Ken,

I’m assuming it’s to do with the Qualified Mortgage rule to ensure the loan doesn’t wind up being high cost.

I have been working with Citizens Bank for seven months to get to closing on a refinance of mortgage plus home equity loan totaling $325,000. After my banker rationalized the delay by saying that was looking for the “best rate,” I was quoted a rate of 3.875 two months ago. On Friday, I received loan documentation adding 5.875 in points ($19,094), with total closing costs of $25,725. When he quoted the rate, he said nothing about points, so I assumed there were none. I mean, why would claim you were shopping for the best rate, when the quoted rate is shot to hell by nearly six points (5.875). This is either gross incompetence or sleezy banking practice. I don’t have that kind of money for closing costs, so I am in a quandary about what to do next. Should I attempt to negotiate a deal with fewer points, even if raises the rate, or should I walk away.

Ken,

Wow, that’s a lot of points. Not sure why they quoted you that way, perhaps to offer you the lowest rate possible, even though it costs an arm and a leg to actually obtain it. And I doubt anyone would pay that much in real life. It may have been close to free to obtain that rate seven months ago, but now that rates have jumped, it costs several points to secure the same low rate. May want to check other options to see what else is out there. Probably a middle ground where you can pay a point or so and get a relatively low rate.

Very useful page, great conversation. Thanks Colin. Question :

Since points are loan officer’s compensation, are they negotiable? I am being offered 1.5 points on a $1M loan which means $15k. She is not going to work 3 times more than a loan in which she would get $5k, right? Is it customary to cut a deal to either get a $10k credit back or simply reduce the points from 1.5 to 0.5? Can a broker do that if she agrees to? Wouldn’t this be in her interest instead of seeing me checking elsewhere and eventually walking away?

Kevin,

Absolutely. You have every right to negotiate and I’m sure she doesn’t want to lose a million-dollar deal. Typically, a smaller loan amount will come with more points because they’re worth less at that loan amount. For example, a $500k loan would require 3 points to generate $15k in commission. You wouldn’t get a credit (unless you wanted it to cover closing costs), they’d just reduce their fee or give you a lower rate. Good luck!

Hi Colin,

Can you clarify a bit more on federal regulations re: Qualified Mortgage? I’m currently in loan process (a refi) with a lender who is discouraging us from buying our rate (4.125) down by 2 points, stating caution regarding “high balance loan†and speaking of government regulations after the crash/predatory lending, etc.

I’m not clear – if government regulates us not to buy points to lower our rate/monthly payments over the life of loan, why is it even an option for borrowers to buy points? Isnt is basically interest we pay up front which goes to lender’s commission? Why discourage it?

I cant find where these regulations are listed and want to be aure that this isnt just the bank preferring us to have a higher rate for higher interest for their longterm benefit. I really have to think about what works for me and my family.

G,

Up to two bona fide discount points can be excluded from from the Qualified Mortgage (QM) points and fees cap. This is part of the Ability-to-Repay and QM rule. Bona fide means they actually result in an interest rate reduction for the borrower and reduce the rate by an amount within typical industry norms.

Hi Colin,

We are refinancing our home. Original quote was $323k at 3.25% for 30 years. I was able to negotiate and received 3.125% with a point ($3k fee) but I also got $4k lender credit, the loan amount got reduced to $321k (negotiated to reduced loan amount) for 30 years and we will get our old escrow as a refund. With the lender credit, closing cost is now $5,200 (include prepaid, escrow, loan cost). We want to make sure the lender is actual giving us a deal as they claim or are they playing us. Is this a good deal?

NM,

I don’t know what the closing costs were at 3.25%, so it’s hard to know if it’s any better. But if the lower rate costs you $1,000 less net thanks to the credit, it’s apparently the better deal. Maybe the rate is lower because your lower loan amount resulted in a lower LTV? Not sure why it’d be cheaper unless market pricing improved during negotiations. Either way, consider how much you’re actually saving with a .125% in rate improvement. It’s probably only $25 a month.