Ever wonder how the economy goes ’round? Or how inflation is controlled and recessions are avoided? Or at least attempted to be avoided.

Much of it has to do with the Federal Reserve and its tight control of the money supply.

Whenever the Fed gets together and makes a so-called announcement, a lot can change that directly affects your pocketbook. So it’s important to have some idea of what it all means.

Let’s take a closer look to better understand how it works. And how it affects mortgage rates.

(Latest rate movement DOWN 0.25% on 12/18/24)

Discount Rate (Currently 4.50%)

- The discount rate is the interest rate the Fed explicitly sets

- Money can be borrowed overnight via the “discount window”

- By member banks and thrifts that are in need of funds

- Used to prevent their reserves from falling below mandated levels

The “discount rate” or “primary credit rate” is the interest rate the Federal Reserve sets and offers to member banks and thrifts that need to borrow money in order to prevent their reserves from dipping below the legally required minimum.

This situation can arise if a bank lends too much and/or has too many withdrawals on a given day. Money is borrowed overnight via the “discount window.”

As a rule of thumb, the higher the discount rate, the higher mortgage interest rates will be. The two tend to correlate over time, though not as strongly as the 10-year bond yield due to its longer maturity.

When the discount rate goes up, the prime rate goes up as well, which can slow the demand for new loans and cool the housing market.

The opposite is also true. If the Fed lowers the discount rate, the prime rate will come down and mortgage interest rates may dip to more favorable levels.

This can boost a slumping housing market, though the decision to purchase a home doesn’t always come down to the level of interest rates, as some buyers purchase with cash, and a stronger economy leads to higher home prices.

[Home prices vs. mortgage rates]

Prime Rate (Currently 7.50%)

- The prime rate is used as a base interest rate

- Applies to all types of consumer loans including HELOCs and credit cards

- Typically with some margin added to prime for the fully-indexed rate

- The fed funds rate dictates the direction of the prime rate

The “prime rate” is the interest rate offered by commercial banks to its most valued corporate customers. But in reality, it just serves as a benchmark for lending rates.

The prime rate always adjusts based on how the Fed moves the discount rate. If the discount rate is increased, the prime rate will follow suit. And vice versa.

The prime rate is the basis for certain home loan programs, including widely issued HELOCs (Home Equity Line of Credit).

Many banks offer these loans to homeowners at prime plus “X” amount, prime minus “X” amount, or simply prime plus zero.

Lenders come up with HELOC rates by adding a margin on top of the prime rate (or sometimes subtracting a number if you’re lucky!)

When shopping for a HELOC, pay close attention to the HELOC margin as prime will be the same across all banks.

To sum it up, HELOCs are essentially adjustable-rate mortgages because they’re variable based on the Fed’s monetary policy action.

Of course, there have been and will be long periods where the prime rate doesn’t change much or at all.

Federal Funds Rate (Currently 4.25% – 4.50%)

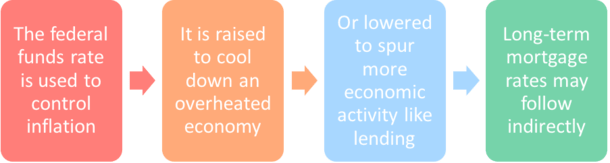

- The fed funds rate is a tool to control inflation

- It’s what banks charge one another for the use of their excess reserves

- The Fed sets a a target rate (range) by buying or selling government bonds

- It drives all other interest rates including long-term mortgage rates

The “federal funds rate” is the interest rate banks charge one another for overnight use of excess reserves. Put simply, banks can avoid borrowing directly from the Federal Reserve (via the discount window) by borrowing from one another instead.

The Federal Reserve doesn’t actually set the federal funds rate, but rather sets a “target rate” and works to keep it in a given range by buying or selling government bonds.

The Fed uses the federal funds rate to control the supply of available funds, essentially managing inflation. If the federal funds rate is low, banks will be keen to borrow from one another, using the reserves to grant more loans, which in turn feeds the economy.

If the Fed feels the need to slow things down, they will simply raise the target for the federal funds rate, which will curtail borrowing among banks and reduce the amount of new loans issued to businesses and consumers. This can cool off an overheated economy.

Either way, the Fed doesn’t control mortgage rates, nor does it set them. Its policies simply impact the economy, which can have indirect effects that trickle down to the interest rate you might be offered on a home loan.

Keep in mind that these key rates are just one of the many factors that determine the direction of mortgage rates. So don’t assume mortgage rates will be lower (or higher) just because these rates are.

If you’re currently in a fixed-rate mortgage, the Fed’s action won’t matter. Your interest rate stays the same unless you refinance your mortgage.

Conversely, if you’ve got an ARM, it could push the related mortgage index higher or lower depending upon the action taken, which would alter your fully-indexed rate and corresponding monthly payment.

If you’re shopping mortgage rates, Fed action can make a meaningful impact, so always pay attention to what’s going on in the economy!

Read more: Mortgage rates vs. the stock market.

Here’s a perfect example of how the Fed rates don’t necessarily affect mortgage rates. The Fed hasn’t touched the Fed funds rate (it’s still rockbottom), yet mortgage rates have increased about 1% or more in the past month or two. This means home equity lines, which rely on the Prime Rate, are still dirt cheap.

i think this website is very important.