There have been three recessions since the 1990s, including the Great Recession, which took place from 2007 and 2009 and lasted about a year and a half.

Earlier, a recession took place in 1990 thanks to growing inflation and debt, followed by the Iraqi invasion of Kuwait, which exacerbated oil prices.

Just about everyone knows what happened a decade later, the infamous dot-com bubble, where any old (actually very new) tech company was valued at billions of dollars, despite failing to turn a profit. Or even having a business to speak of.

Feels Kind of Like the Year 2000 Again…

- Your electric scooter company is worth how much? What’s a unicorn?

- Why does every new company use a single word for its name?

- This is starting to feel a little bit fishy

- Reminds me of when every website was worth a billion dollars

Interestingly, it’s beginning to feel a lot like the year 2000 when you look at the many tech companies raising millions of dollars and grabbing billion-dollar valuations.

Just look at those ubiquitous scooter companies, which are somehow worth billions…I anticipate those things being obsolete in 10 years, or at least relegated to bike paths at popular tourist attractions.

Remember Segway? Ironically, they do the tech on some of these very scooters.

Anyway, it’s clear that we seem to be heading back down a dark path, with fears of another recession right around the corner.

So much so that there’s talk the Fed might stop raising rates, especially if we see a sustained inverted yield curve, where rates on long-term bonds like the 10-year fall below those on short-term bonds, like the two-year.

Assuming this all plays out and we enter another recession, which wouldn’t be all that surprising given their fairly cyclical pattern, what would happen to the housing market?

The Housing Market May Be Just Fine in the Face of a Recession

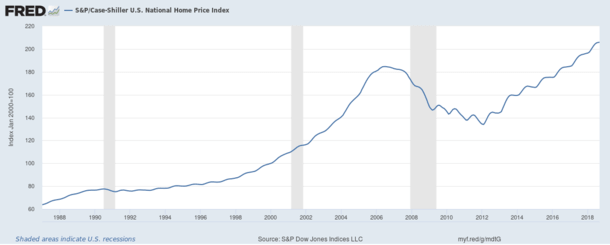

If we consider those last three recessions again with respect to the housing market, in the first, home prices went down slightly for a short period of time before gradually climbing.

During the second recession around the time of dot-com bubble bust, home prices actually increased nationally.

Sure, there were probably areas that experienced pullbacks, namely San Francisco, but overall, if we look at the chart, home prices kept marching higher.

In other words, housing wasn’t to blame for the recession, and thus home prices did just fine.

However, during the third and most recent Great Recession, home prices tanked. And they fell hard for many years thereafter.

Lots of folks lost their homes via short sales and foreclosures, and some who kept them still remain underwater on their mortgages, amazingly.

But home prices have since bounced back in major fashion, and are at new all-time highs, at least nominally (not inflation-adjusted).

Does that mean we can look at a basic pattern and say home prices fell, then went up, then fell, and thus will go up this time?

It’s probably not so cut and dry, but we can at least say with some level of certainty that this next recession, assuming it comes, will have nothing to do with the housing market.

Why? Because today’s homeowner has a boring 30-year fixed mortgage (or even 15-year fixed!) in the 3%-range, with lots of home equity to cushion any decline in prices. They aren’t the highly-leveraged homeowners of a decade ago, not even close.

At the same time, inventory remains below long-term averages, so supply isn’t an issue either, even if it does begin to creep up to more normal levels.

That means banking on a home price sale once the recession strikes might be a bad move.

Homeowners May Hunker Down During a Recession

- Sure, home sales might drop if a recession hits

- But a recession could lead to reduced inventory and lower interest rates

- As homeowners stay put and inflation concerns wane

- That could actually propel the housing market even higher, though inflated real estate prices could eventually be to blame for a subsequent recession

If anything, a recession might actually lead to an even tighter supply of for-sale homes as more folks just decide to stay put.

After all, if you’re not so confident about your job, you might simply opt to stay in a holding pattern until prospects improve.

As such, home sales may falter, which would be a blow to both real estate agents and mortgage lenders.

But less inventory could temper any expected home price declines. Additionally, a recession could push mortgage rates lower, strengthening the refinance market and also increasing demand for real estate.

If anything, it bolsters the argument to park money in real estate as opposed to the risky stock market or some low-yielding investment like a savings account.

Remember, homes aren’t just an investment, they are shelter. And existing homeowners will continue to live in them and new buyers will keep buying them as needed, regardless of what’s happening in the economy at large.

There are a lot of Millennials coming of age that will start families, regardless of what’s happening out there.

And if they can snag a lower interest rate and possibly a slightly discounted home price in the process, the housing market may not miss a beat.

The takeaway I suppose it that today’s homeowners can stomach a recession, whereas the same couldn’t be said a decade ago.

That gives me hope that home prices will hold up well in the face of an economic downturn.

The caveat being that you do have to look locally at specific metros. For example, if tech does crash again, Bay Area home prices and surrounding areas may get hit too.

Same goes for any other industry impacted by the next recession – it could put some downward pressure on home prices in those specific regions, at least until things turn around.

Read more: The relationship between home prices and mortgage rates.