Two new credit scores will be used if and when you apply for a mortgage backed by Fannie Mae or Freddie Mac in the near future.

On October 24th, 2022, the Federal Housing Finance Agency (FHFA) announced the validation and approval of both “FICO 10 T” and “VantageScore 4.0.”

These new credit scoring models will replace legacy credit scores that the Enterprises have relied upon for almost 20 years.

The FHFA notes that they “improve accuracy” through the capture of new payment histories including rent, utility, and telecom payments.

They also ignore paid off collections, and reduce the impact of unpaid medical debt, meaning credit scores of prospective home buyers might rise.

What Are FICO 10 T and VantageScore 4.0?

In short, FICO 10 T and VantageScore 4.0 are the latest credit score models available.

FICO 10 T is issued by FICO (formerly Fair Isaac), while VantageScore 4.0 is the latest iteration of the credit score model developed jointly by the three main credit bureaus, Equifax, Experian, and TransUnion.

These newer scoring models include payment history for things like rent, utilities, and cell phone payments.

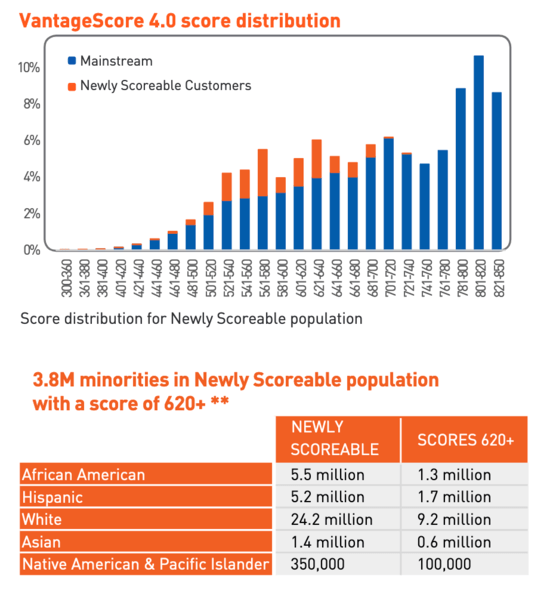

Often, consumers with “thin credit files” don’t have enough history to generate a traditional credit score.

Generally, this is referred to as having fewer than five accounts, typically because the individual doesn’t have credit cards, auto loans, or mortgages on their credit report.

This creates a catch-22 situation where the applicant is unable to get approved for a new loan due to their lack of loan history.

These new credit scoring models address that by including non-traditional credit like rent and utilities, which can also demonstrate a history of on-time payments.

The table above shows how many more consumers will have useable credit scores.

Additionally, they reduce the impact of unpaid medical collections, and ignore paid off collection debt.

That type of debt tends to disproportionately affect Black and Hispanic consumers, making it more difficult for them to qualify for a mortgage.

Those are the potential benefits of using FICO 10 T and VantageScore 4.0, which VantageScore believes could increase annual mortgage production by $1 trillion.

FICO 10 T Credit Scores Will Be Even Higher (or Lower)

While it’s mostly good news that mortgage lenders will begin using more updated credit scoring models, there is a caveat.

If you already had a good credit score under the old scoring models, it will likely be even higher via the new models.

In other words, you’ll get rewarded even more for good credit habits via the new models.

But if you had poor credit under the old models, your scores may drop even more under the new models.

Per Experian, things like missed payments, outstanding credit card debt, and even personal loans can hurt credit scores more under new models like FICO 10 T.

So not all folks will see improvement here, despite the mostly positive changes.

All the more reason to manage your credit better, whether it’s paying off balances more aggressively, avoiding late payments, and applying for new credit sparingly.

Additionally, you’ll still be able to use things like Experian Boost to potentially raise your credit scores.

FICO 10 T and VantageScore 4.0 also use trended data (that’s what the T stands for), which looks at a consumer’s credit behavior over time, instead of simply a snapshot in time.

This means credit bureaus can go back 24 months to see how you manage your credit card debt, and determine whether you’re a “transactor” who pays it off in full, or a revolver who carries a balance.

They can also see if you are lowering these balances over time, or increasing them.

You want to be the consumer who pays your revolving balances in full each month to generate a higher credit score.

A Tri-Merge Credit Report Will No Longer Be Required to Get a Mortgage

The FHFA also announced that a tri-merge credit report will no longer be required to obtain a home loan backed by Fannie Mae or Freddie Mac.

Instead, a bi-merge credit report will be required, one that is backed by just two of three major credit reporting agencies.

In other words, a credit report that incorporates data from just TransUnion and Experian, or just Experian and Equifax.

Currently, you generally need a tri-merge report with three credit scores, and mortgage lender uses the mid-score as the qualifying score.

If only two reports and scores are used, my assumption is the lower of the two scores would still be used for qualifying.

Either way, the FHFA believes this could reduce costs and “encourage innovation,” though I don’t know if savings will be substantial for consumers.

It should be noted that these changes will take time to implement, and likely won’t happen overnight.

Additionally, mortgage lenders will be required to deliver loans with both types of scores when available.

It’s not clear if that means one VantageScore and one FICO score, or two of both.

But hopefully if and when the changes are incorporated, credit becomes less of a roadblock to homeownership.