It’s time for another mortgage match-up, the latest installment “mortgage rates vs. recessions.”

This is a timely post seeing that mortgage rates have gone absolutely bonkers lately and talks of another recession are heating up.

The Fed created a very accommodative monetary policy over the past decade via Quantitative Easing (QE), which pushed mortgage rates to record lows.

But that (combined with COVID-19 and war-related supply chain issues) eventually triggered troubling inflation, forcing the Fed to act aggressively the other way, which could result in a recession sometime soon.

The question is does a recession portend lower mortgage rates, higher mortgage rates, or nothing at all?

Mortgage Rates Typically Fall During Recessions

First off, a recession is defined as “a significant decline in economic activity that is spread across the economy and that lasts more than a few months,” per the National Bureau of Economic Research (NBER).

In simple terms, this means a receding economy as opposed to a growing economy for a sustained period of time.

This could be evidenced by a contraction in the gross domestic product (GDP) over consecutive quarters.

Basically, consumers curb spending, companies output less product, layoffs happen, and so on. The dynamic shifts from easy money spenders to stingy savers.

As noted, the Fed engineered low interest rates via QE. They purchased hundreds of billions in Treasuries and agency mortgage-backed securities (MBS) to boost liquidity and encourage lending.

This turned out to be great for the mortgage industry, as interest rates fell to the lowest levels on record.

The 30-year fixed hit a mouthwatering low of 2.65% in early 2021, while the 15-year fixed dropped to 2.10% later that year.

We know good things never last and must eventually come to an end. And now we might be paying the price for all those good years.

[Does the Fed Control Mortgage Rates?]

The Fed Is Raising Rates to Combat Inflation, But May Have to Lower Them Soon After

All the easy money over the last several years led to major inflation and the Fed is now on the offensive, even though it might be too late to avoid a major downturn.

They’ve been hard at work fighting inflation by raising the target federal funds rate and reducing their swollen balance sheet.

Instead of buying Treasuries and MBS, they’re now letting them run off. And they could eventually sell MBS outright, which could flood the already weak market.

Simply put, with the Fed not a buyer, and worse a seller, supply goes up.

Unless demand rises somehow, the price of the bonds goes down and the yield must come up.

This translates to higher interest rates for consumers on things like home loans, auto loans, and so forth.

This is made even worse when inflation expectations are high, delivering a one-two punch to mortgage rates.

Now if the Fed keeps raising rates and unloading its balance sheet, there’s a chance of a recession.

It’s not clear when this would happen, though 2023 could be the year.

If it transpires, the Fed could be forced to lower its target fed funds rate to stimulate growth and get the economy chugging again.

Could that finally be the reprieve the mortgage industry would be waiting for?

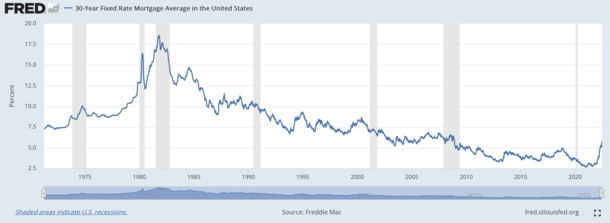

A Look at Mortgage Rates During Past Recessions

The chart above shows the average 30-year fixed-rate mortgage based on Freddie Mac data, retrieved from FRED, Federal Reserve Bank of St. Louis. The shaded portions are U.S. recessions.

The most recent recession was the COVID-19 recession that lasted from February to April of 2020.

It was very short-lived, but during that time the 30-year fixed mortgage still fell from 3.45% to 3.23%, per Freddie Mac’s weekly survey.

Rates continued to fall after that and eventually hit record lows in January 2021.

During the Great Recession, which spanned from December 2007 to June 2009, 30-year fixed mortgage rates started around 6.10% and fell to roughly 5.42%.

That recession was caused by the mortgage crisis, whereby loose home loan lending collapsed the global financial system.

In the early 2000s recession, from March 2001 to November 2001, mortgage rates began at 6.95% and fell to 6.66%.

In the early 1990s recession, from July 1990 to March 1991, mortgage rates fell from around 10% to 9.5%.

The prior recession, from July 1981 to November 1982, saw rates plummet from 16.83% to 13.82%.

And the 1980 recession from January 1980 to July 1980 saw rates move lower from 12.88% to 12.19%.

In all instances, mortgage rates went down during a recession. Of course, the decline ranged from as little as 0.22% to as large as about 3%.

The only exception was the 1973-1975 recession, triggered by the 1973 oil crisis, in which rates climbed from 8.58% to 8.89%.

That was a period of so-called stagflation, which some pundits believe is happening again. That remains to be seen.

Obviously, homeowners, prospective home buyers, and the mortgage industry will all be hoping for that latter, big decline.

When you look at those time periods, many economists compare the 1980s to today, so it’s possible we could see big relief, eventually.

The problem is how much more do mortgage rates go up in the meantime, before a recession happens, if it even happens at all?

Will the 30-year fixed keep rising and hit 7 or 8% by late 2022 and early 2023, then fall to 6%?

If that’s the case, any decline related to a recession would just get us back to the heightened level where rates sit now.

In other words, prepare for worse as the Fed tries its darndest to stem inflation and hope things settle back down quickly thereafter.

Either way, you may want to kiss the 3-4% mortgage rates goodbye, at least for the foreseeable future.

See also: Home Prices vs. Recessions

- Mortgage Rates Catch a Break as Job Growth Goes Negative - August 7, 2026

- Mortgage Rates Move Higher on Jobs Report Defense - August 6, 2026

- Mortgage Rates Are Now Higher Than They Were a Year Ago - August 5, 2026