Quick mortgage tip: “How do I know if Fannie Mae or Freddie Mac owns my mortgage?”

One of the key requirements to getting approved under the CARES Act to receive mortgage forbearance is ensuring that your loan is indeed owned or guaranteed by Fannie Mae or Freddie Mac.

If it isn’t, you might still be eligible for mortgage relief as long as your loan is backed by the FHA, USDA, or VA. For those explicit government loans, it’s a little more straightforward.

Knowing who owns your loan can also be helpful to determine if you’re eligible for a particular loan modification, or if you can pursue certain foreclosure prevention options via each agency.

Fortunately, the pair has made it very simple to find out if your mortgage is owned or backed by either.

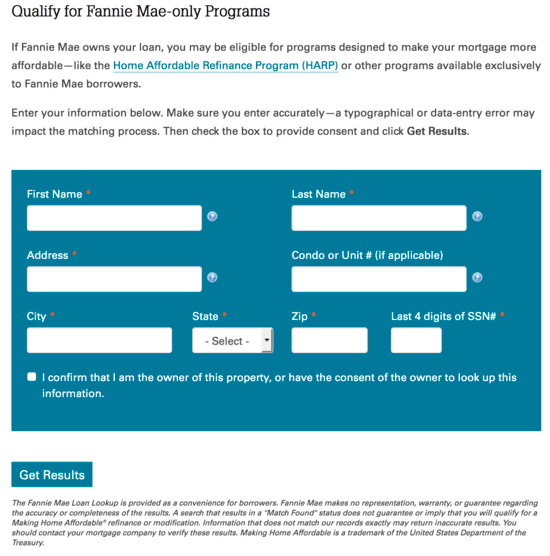

Fill Out the Short Form

- To find out if Fannie Mae or Freddie Mac own your mortgage

- All you have to do is fill out a short form on their website

- You will be notified immediately if they do or do not own it

- If they do you’ll be directed to options for assistance

All you have to do is fill out a short form with your name, last four of your social, and property address, and they’ll let you know immediately if they own your home loan.

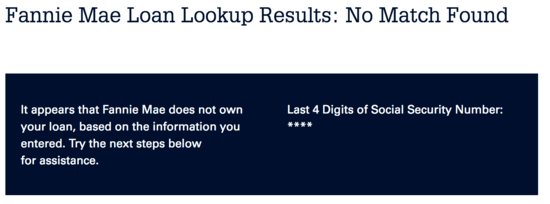

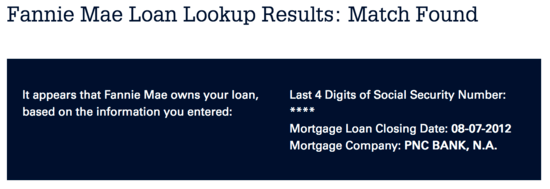

You will receive one of two status messages. Either that no matches were found, or that a match was indeed found. If it’s the latter, you may be eligible for help.

For Freddie Mac inquiries, click here, and for Fannie Mae inquiries, click here.

No Matches?

Match Found!

Assuming a match is found, it will list the mortgage company that owns your loan (or that originated it before transferring it to a new loan servicer) and the mortgage loan closing date, which I believe is the day it funded.

You will also see some questions at the bottom of the page, including if you’ve been delinquent on your mortgage in the past 12 months, and if you anticipate being late in the near future (next 2-3 months).

These are basically next steps if you’re looking up loan ownership in order to apply for mortgage assistance.

Watch Out for Address Errors

Note: If you own a condo or townhome, the search feature will often say there is no match if you put your street address and unit number in the separate boxes.

Instead, try putting it all in the street address box if you’re pretty certain Fannie/Freddie owns your loan, but it’s not showing up as a match.

For example, put in 123 Fake St. Apt. A all in the “address” box as opposed to broken up in the “condo or unit #” box.

It might also be possible to get a match without even inputting your unit number. Just make sure it lists your name and everything looks right on the results page.

Also notice that you’re required to check a box that says you are the owner of the property or you have the consent of the property owner to look up the information.

What to Do Once You Know Your Loan Is Owned by Fannie or Freddie?

- Take note of the lender or loan servicer listed on the results page

- If you make payments to that company still, reach out to them for help

- If you pay a different company due to a servicing transfer, call them instead

- Generate a mortgage forbearance letter so you can send it to them to get the ball rolling

In terms of qualifying for mortgage forbearance via the CARES Act, it appears to pretty straightforward, with very little paperwork needed.

There is even a free tool that helps you generate a mortgage forbearance letter in minutes.

However, it’s also a brand new program, so loan servicers and lenders are probably still figuring it all out themselves.

Once you know that Fannie Mae or Freddie Mac own your mortgage, you should contact your loan servicer (the company you make your mortgage payments to each month).

Let them know your loan is owned by Fannie or Freddie, and that you need assistance due to the COVID-19 epidemic. Mention the CARES Act and have that letter ready to send their way.

Lastly, keep in mind that there are also loss mitigation programs available with individual banks and mortgage lenders if you don’t qualify for government assistance.

I have a list of mortgage assistance options for coronavirus-related loss of income that you can peruse as well.

Basically, everyone is providing some form of relief, though the government program appears to be the best, with waived payments for 6-12 months without any extra cost.

Read more: How is mortgage forbearance paid back?

- Mortgage Rates Could Drop as Much as Half a Percent with Basel Re-Proposal - June 30, 2026

- Mortgage Rates Face Big Week of Jobs Data - June 29, 2026

- Are Mortgage Rates Finally Poised to Start Falling Again? - June 25, 2026