The latest buzzword on the street is “shutdown,” and apart from being buzzworthy, it’s actually very real.

National parks are closed and hundreds of thousands of government workers have been told to stay at home.

Fortunately, active military continues to serve and air traffic controllers, prison guards, and border patrol agents remain on the job.

But how does the shutdown affect the mortgage industry?

Well, it depends on the type of loan involved, though just about everything will be impacted to some degree. So the name of the game might just be patience.

FHA Loans

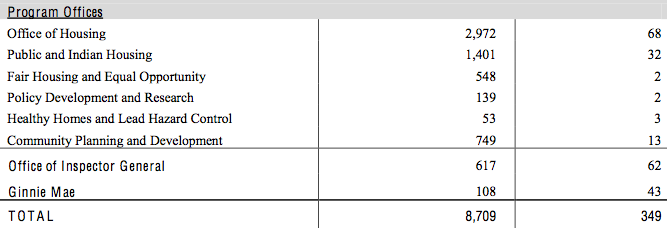

The most popular government loans are insured by the Federal Housing Authority (FHA), which operates under the Department of Housing and Urban Development (HUD).

HUD noted that it has 8,709 employees “on board as of pay period ending September 7, 2013.”

In the event of a shutdown, limited staff will remain on hand to handle certain business activities, including FHA loan processing.

Take a look at the chart above to see how few employees would be working during a shutdown…not very many.

In other words, while FHA loans will still continue be processed, there will definitely be delays.

Fortunately, FHA lending has become a lot less popular due to higher premiums, which should offset some of the carnage.

Also note that Ginnie Mae, which guarantees mortgage-backed securities (MBS) backed by federally insured or guaranteed loans, will see its staff slashed, though it said it will “continue to perform its critical and essential functions.”

Here’s an updated notice for the potential 2023 government shutdown, which says HECM loans and Title I loans can’t be insured.

VA Loans

Despite the U.S Department of Veteran Affairs (VA) being very much a government agency, it will continue to operate many of its operations, including its core medical facilities and home loan processing.

So borrowers looking to obtain a VA loan should expect business as usual, barring any delays that result from the overall shutdown.

If you’re attempting to get a VA loan, patience should probably be exercised as precautionary measure.

Here is an update for September 2023 regarding the potential shutdown.

USDA Loans

The USDA, while seemingly an agency dedicated to agriculture, also operates a popular zero down home loan program reserved for rural locations.

As a result of the shutdown, the entire USDA website is currently down. Well, there’s a nice little message about the shutdown, but you can’t access any key information.

Additionally, the USDA Rural Development Guaranteed Housing Loan Program appears to be on hold during the shutdown. In other words, nothing is doing at the USDA until politicians learn to get along.

However, the USDA will continue to handle existing customers funds, such as processing escrow accounts to avoid tax penalties.

Fannie Mae and Freddie Mac

While Fannie and Freddie aren’t technically government entities, despite being in government conservatorship (don’t ask), these conventional loans are also being impacted by the shutdown.

First off, government workers whose employment is directly affected by the shutdown could run into snags during the loan underwriting process, seeing that lenders need to verify employment in order to sell their loans to Fannie and Freddie.

As a result, Fannie Mae released guidance on a few workarounds, advising lenders that they can obtain verification of employment (VOE) after the loan closes, but before it is sold. This is actually already permitted, so perhaps just a reminder.

The pair also require lenders to complete requests for borrower tax returns (IRS) and social security numbers, both of which will be difficult to obtain in light of the government shutdown.

Fannie is revising its policies temporarily to allow lenders to obtain the transcripts and complete validation after loan closing, but before loan delivery. In other words, buying some time.

So the hope is that lenders who sell their loans off to Fannie and Freddie will continue to underwrite and process loans on the basis that the shutdown won’t last long enough for them to be stuck with the loans.

Additionally, loan servicers have been advised to waive late payment fees if the borrower’s mortgage payment is late because of a government furlough.

Servicers are also being encouraged to offer Unemployment Forbearance to employees affected by the shutdown, assuming they’re unable to make housing payments.

For the record, even non-conforming loans and jumbo loans will be affected by the shutdown, seeing that lenders may still need to call on government agencies for certain information, so no loans are entirely exempt.

At the end of the day, patience is the name of the game here. Ideally, the shutdown won’t last too long and none of this will matter. But in the meantime, expect delays if you’re attempting to get a mortgage. And pray mortgage rates don’t spike in the process.

Read more: What Happens to Mortgage Rates During a Government Shutdown?

- Trump Says Warsh Wants Lower Interest Rates, But Has a Political Board - July 30, 2026

- Do Mortgage Rates Need a Hike to Move Lower? - July 28, 2026

- How Mortgage Rates Avoid a Return to 7% - July 24, 2026

During the last shutdown in the brutal winter of 1995-1996, I was living and working in Metro DC but unemployed for part of the time and it was brutal beyond the weather. Unless resolved within two weeks, the damage to that local economy and well beyond, given the networked nature of the US economy on a far more global basis now, is going to be far greater let alone going into another winter up there. Hold onto your hats or you seats depending where you live folks, and the Obamacare transition costs make the coming season even worse.

One thing I forgot to mention is that the government shutdown will delay the mortgage market during a critical interest rate environment post-taper, meaning the lower mortgage rates on offer are unobtainable if loans can’t close.

government shutdowns wreak havoc and politicians do not care