I’ve already covered the mortgage underwriter’s role, so let’s take a look at what mortgage loan processors do too.

After you speak to a mortgage broker or loan officer and agree to move forward with a loan application, a processor may reach out to gather required paperwork.

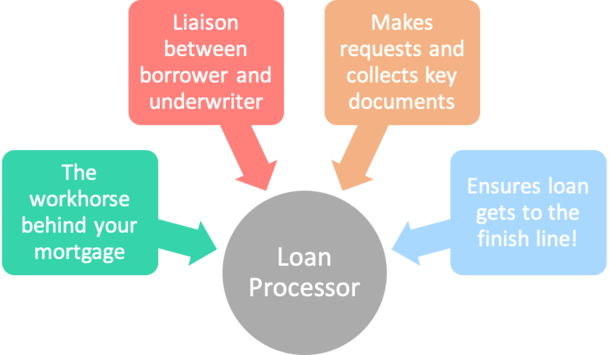

This individual is responsible for prepping and organizing your loan file and getting it over to the underwriting department for approval.

Other than that, they can also answer questions, provide status updates, and guide you through the loan process from start to finish.

In that sense, they play an integral role in getting your loan funded while acting as a liaison between you and all parties to the loan.

Loan Processors Are the Workhorse Behind Your Mortgage

- A loan processor’s main function is to assist mortgage brokers and loan officers from application to funding

- They compile and review important paperwork from the borrower like pay stubs and bank statements

- And look out for any red flags along the way that could create issues or headaches

- They also communicate with all parties to the loan from start to finish to ensure everything goes smoothly

Loan processors, also known as loan coordinators, are very important figures in the home loan process, and often quite knowledgeable about mortgages as well.

They are the loan officer’s right-hand man/woman that assists with loan prep and all the day-to-day stuff that happens from loan origination to loan funding.

This includes gathering paperwork from the borrower, determining loan eligibility, reviewing loan files, submitting documents to the underwriter, helping you write a letter of explanation, answering questions, and communicating with all parties along the way.

They don’t just grab the loan file from the salesperson and submit it; they go over everything like debt-to-income ratios, bank statements, and employment history to ensure the file will actually be approved.

Simply put, their role in the loan approval process is a critical one, as mistakes made by the loan originator could be caught and corrected before the file lands in the unforgiving hands of an underwriter.

And once it gets to the underwriter’s desk, there’s typically no going back.

Assuming the loan is approved, the processor will also receive a list of prior-to-document conditions (PTDs) that must be met before the borrower can sign loan documents and fund their loan.

It is the processor’s job to work with the loan originator, title and escrow companies, and various others to get all the necessary paperwork to fulfill those conditions.

And with so many people involved in the mortgage process, things can get very complicated in no time at all.

The good news is they handle numerous loan files each month and have likely seen it all. This means aside from pushing paper from point A to point B, they can solve problems and put out fires.

You May Spend More Time Working with the Processor Than Anyone Else

- It’s common to talk more with the processor than with the loan officer

- Once you submit your loan application they may be your main point of contact

- Since LOs/brokers main focus is to spend more time selling and finding new prospects

- The good news is loan processors are often very knowledgeable and hardworking individuals

While the loan officer or broker may be the person who “got you the loan” to begin with, it’s the processor that will likely take over once you’ve been “sold” on which company to work with.

That sold part is pretty important because loan processors aren’t supposed to offer or negotiate mortgage rates or discuss the terms of your loan.

Their role is to assist the loan originator, whose job it is to sell you on the rate/product.

However, some processors are actually more knowledgeable than their sales colleagues because they handle more volume and may have many years of mortgage experience under their belt.

And while it might sound odd, you could wind up spending more time on the phone with the loan processor than the loan officer.

After all, the LO will want to get back to finding additional clients, while the processor will be focused on getting your loan closed.

But it’s essentially a team effort, with everyone working together to get you to the finish line with as few hiccups as possible.

In a nutshell, the loan originator hustles to bring in new borrowers and the loan processor hustles to get the loans funded, while both may irritate the underwriter in the process. : )

Loan Processor Job Description

- An individual who prepares and manages the home loan from start to finish

- Acts as an assistant to the originating loan officer or mortgage broker

- Sends out disclosures, collects paperwork from the borrower, reviews documents, and facilitates loan submission

- Creates checklists and sends verification requests to the borrower for needed items

- May order the home appraisal, credit report, HOA documents, and collect insurance information

- Communicates with the loan officer, underwriter, and borrower to ensure conditions are fulfilled once the loan is approved

- Acts as a liaison between all parties, including third-party escrow/title/insurance companies

- Makes sure all tasks are completed and all deadlines met throughout the loan process

Loan Processor vs. Account Manager

If the mortgage is obtained via the wholesale channel (from a mortgage broker), there are essentially two loan processors working together on a single file.

One who works on behalf of the mortgage broker, discussed above. And one who works at the wholesale bank/lender, typically referred to as an Account Manager (AM).

This AM assists an Account Executive (AE), who is essentially the salesperson on the wholesale side of things.

Like a loan processor, the AM will request and review documents from the broker and various third party vendors to ensure the loan closes in a timely fashion.

The AM also acts as a liaison, but between the AE and underwriter. And what they communicate with the AE can be passed along to the broker.

Loan Processor FAQ

Do loan processors need to be licensed?

Some independent processors might need licenses, but those working for licensed mortgage lenders or under the direction of licensed mortgage originators may be exempt. This can vary from company to company and by state.

Do loan processors make commission?

They certainly can and often do. It depends how they set up their pay structure with their employer. They may get paid per loan file funded or a base salary AND a bonus for a certain volume of funded loans each month.

How much do loan processors make per loan?

Again, it depends on the company and perhaps on what their base salary is. If their base is low or nil, they’ll probably make a lot more per loan via commission. The downside is they are then working a performance-based job.

Do loan processors work weekends?

The job might require work on the weekend if a particular lender or broker is busy, or has busy periods. However, many processors just work Monday through Friday like most other bankers.

Do loan processors work from home?

They can work remotely or from home depending on the preferences of their lender or broker. Or if they’re independent they can run their own home office and work with multiple brokers/banks.

What are loan processing fees?

These are very real fees for the loan processor’s hard work. As I mentioned, loan processors might do more of the work once the saleswoman (or man) gets you in the door. This fee could be anywhere from $200 to $700 or more.

Some may refer to it as a junk fee but only if it’s charged on top of a hefty origination fee. Sometimes the latter includes the processor’s work and isn’t a separate line item.

(photo: kozumel)

- Mortgage Rates Could Drop as Much as Half a Percent with Basel Re-Proposal - June 30, 2026

- Mortgage Rates Face Big Week of Jobs Data - June 29, 2026

- Are Mortgage Rates Finally Poised to Start Falling Again? - June 25, 2026

As someone who is versed in the industry. Would you be able to recommend a class/training method for someone who is looking to get into mortgage underwriting? thanks in advance.

TU,

Typically whatever company hires you will have you go through a training course over the course of a few weeks. However, the best way to learn quickly is when you are truly hands-on. Generally you work under a more seasoned individual first, assisting them while learning about the processes involved.

I just passed the test. Now, should I apply for Loan Officer or Processor. Which one is of “new comer”? And how do you get paid commission as realtor? Please help.

Lydia,

A loan processor deals with lots of paperwork and basically assists the loan officer in closing the loan. Conversely, both loan officer and real estate agent jobs are sales job that require selling and finding clients. So it depends where you personality puts you. Real estate agents get a portion of the sales price, say 3%, but have to give some of it their listing brokerage. LOs also get paid commission for closing loans and processors may get an hourly and also bonuses for closings lots of loans each month.

Found a job posting for “Mortgage Loan Processor Trainee” and mentions no real estate experience needed. They only really require you have a high school diploma. Is this position really something one can pick up without any mortgage/real estate experience?

Liz,

You can learn pretty quick on the job, like most jobs. You’d probably shadow someone experienced and help them out with basics (doing as they say, getting them X paperwork, etc.) and learn along the way.

I am a real estate agent that is thinking about becoming a Mortgage Loan Originator. I work with a brokerage that does strictly real estate no loans. Can I work both in my real estate office and for a mortgage broker?

Ty,

Best to check your state licensing rules and speak with your company assuming you are sharing these details with them.

Hi. Am trying to get my mortgage license and I also wanted to know what is the different between mortgage license and mortgage processor. Can I work independently or can I work with a company ie: bank, real estate or mortgage company and how do I start.

Jenney,

You may need to check the requirements for the state you live in and the company you plan to work for.

I’m a licensed loan originator and want to only process loans for the brokerage company where I’m at currently. If I work for the broker as a contract processor and receive a 1099 do I need to have my own company? Will the broker have to pay me from his origination fee or can it be charged separately? What if I don’t receive a 1099, will I need a company? Any help would be greatly appreciated.

Teri,

Not really my field of expertise, perhaps someone else can chime in.

Hi, I have on going trainee for the position of Loans processor at the bank here in my country. if I start as a loans processor would there be chances that i’ll be paying for penalties? about my work if ever there are problems.

Charisse,

I doubt it, but then again I don’t know what the work contract stipulates. Typically companies are on the hook for mistakes their employees make, assuming they aren’t intentional and illegal.

What is the difference between Loan Assistant and Loan Processor?

You don’t need a license to become a loan processor. The license you possess is probably for a Loan Originator. Being a Loan Processor, LO, or RE Agent are 3 different jobs and I’m sure you’ve figured it out by now since you question was dated 2015. As a loan processor you have to be very OCD and meticulous on everything from loan opening to loan closing.

The division of duties between LOA and LP vary from company to company and even branch to branch within a company. Some LOAs nearly fully process a loan before submitting it to processing. Some LOs don’t have assistants and can use the Processor as an LOA, although this is frowned upon unless the LP is compensated accordingly. When they are not, it’s called a poor submission and the Processor is covering for the LO in ways they shouldn’t have to and are not compensated for.

I am checking to see what the average contract loan processor makes.

I had to create and register my own company.

I had to get a mortgage broker license

I also had to get a LO license.

I do not intend to originate but feel that my fee is too low for each loan processed. I want to increase my fee but don’t want to price myself out of the market.

I have been in the mortgage Business since 1986.

Hi Collin:

Very insightful post. It seems like the loan processor has a fair amount of paperwork to do, especially the ones at a brokerage, since they liaison with the account managers at the banks. Just out of curiosity – in the 10 years since this post appeared, has that changed ?

The AUS seems to have a lot of new integrations for income verification, employment verification, background etc; and yet, loan processing fees being quoted on loan estimates are the same.

Karan,

That’s a good point, though technology is only as good as the person using it. And it’s still in its infancy. There are newer lenders that don’t charge any lender fees, on the basis that their proprietary tech platforms are doing away with some of these tasks, but a human touch is still very much needed in most cases. That may change as widespread adoption takes place and users become better at utilizing the tech, but until then expect the fees. Lastly, processing fees are easy to tack on and substantiate, even with tech, so it might be hard for companies to give up a profit center.

Loan processing fee is our pocket money to keep?

Jon,

If the lender is charging a loan processing fee, it should mean it’s coming out of your pocket, though it might be covered by a lender credit.

What is an average charge per file for a Loan Processor? Is there a standard fee or percentage that most use?

Tyler,

It depends if they’re an internal loan processor or a third-party, and also how their pay is structured. It can vary widely, and often borrowers aren’t charge loan processing fees directly. But if I had to guess I’d say a couple hundred per file maybe, and typically not a percentage-based fee. Any loan processors out there want to chime in?

If I am borrowing funds from family and have drawn up a mortgage contract with them, should we use a loan processor or other professional? They are concerned that they may not be able to get tax write-offs for the loan without this formality. Any advice appreciated.

Eli,

Not sure a loan processor is the appropriate person for this type of thing. But it may be wise to have a professional of some kind oversee the contract, including a notary. You may want to consult the IRS website regarding seller financing to ensure all conditions are met for tax deductibility.

Does a processor still get paid if the loan does not close or get another house and has to start the loan over?

Sally,

Good question – it would likely depend on if they work for a company or are self-employed, and if they earn a salary and/or commission/bonuses. In other words, compensation may vary from processor to processor. Some may earn base pay while others get paid per closed loan.