Over the past year and change, mortgage refinance applications have fallen off a cliff.

We had some of the biggest refi years in 2020 and 2021, followed by the worst year for mortgage applications this century.

And it’s all because mortgage rates hit all-time lows, then abruptly surged to around 8% in just over 12 months.

Rates on the 30-year fixed have since settled in around 7%, and there’s hope they’ll continue to drop into 2024.

If so, we might see a return to rate and term refinancing as recent home buyers seek out payment relief.

Does Anyone Refinance Their Mortgage Anymore?

As noted, mortgage refinancing hasn’t been very popular in 2023. After a few banner years, the low-rate mortgage party came to an end.

After all, most homeowners already took advantage when rates were low. And very few are forgoing their 2-4% mortgage rate to tap into their home equity.

Instead, they’re opting for a second mortgage if they need money, such as a home equity loan or HELOC.

This allows them to retain their low-rate first mortgage while still accessing their equity.

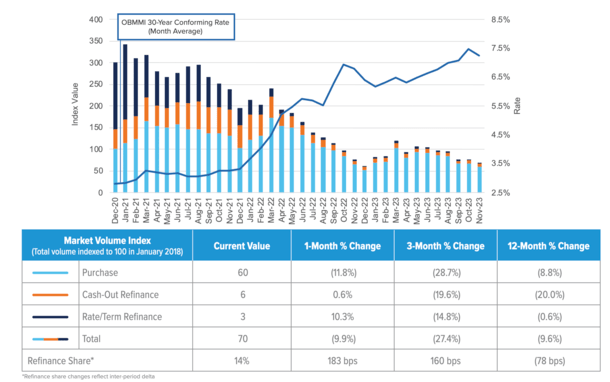

But because mortgage rates have hovered in the 6-8% range for much of the past year, and rates have since improved a bit, the refi applications are beginning to trickle in.

Per the latest Originations Market Monitor report from Optimal Blue, the 30-year fixed improved by 67 basis points during the month of November.

For some lenders, we’re talking a rate drop from around 8% to 7%. This resulted in a 10% month-over-month increase in rate and term refinance applications.

If rates continue to move lower, we might see apps rise even more in 2024.

And because many recent mortgage holders have very high rates, payment relief will actually be easier to come by. Allow me to illustrate.

Refinancing an 8% Mortgage Rate to a 7% Rate

$500k loan amount @8% = $3,668.82

$500k loan amount @7% = $3,326.51

Monthly savings: $342

Let’s imagine a recent home buyer purchased a property when mortgage rates peaked at around 8%.

We’ll pretend they purchased a home for roughly $556,000 with a 10% down payment, leaving them with a $500,000 loan amount.

This would result in a monthly principal and interest payment of $3,668.82, assuming it was a 30-year fixed mortgage.

Now if they were to refinance to a 7% rate, the monthly P&I would drop to $3,326.51. That’s a $342 reduction in monthly payment.

Not too shabby, right? Sure, the rate is still a far cry from the 3% mortgage rates on offer in 2021, but the savings are solid.

Refinancing a 5% Mortgage Rate to a 4% Rate

$500k loan amount @5% = $2,684.11

$500k loan amount @4% = $2,387.08

Monthly savings: $297

Consider the same loan scenario, but with a 5% mortgage rate. That puts the monthly P&I at $2,684.11.

That’s about $1,000 lower each month than the 8% mortgage rate, which explains the affordability crisis currently taking place.

Again, let’s pretend mortgage rates fall by one percentage point and the homeowner looks into a refinance.

If they could exchange their 5% rate for a 4% rate, they’d see a monthly payment of $2,387.08.

That’s only $297 in savings in each month, about $45 less than the homeowner who refinanced from 8% to 7%.

In other words, the borrower who refinanced from one high rate to a slightly lower high rate saved more.

Refinancing an 8% Mortgage Rate to a 6% Rate

$500k loan amount @8% = $3,668.82

$500k loan amount @6% = $2,997.75

Monthly savings: $671

Now let’s assume mortgage rates continue to fall throughout 2024 and hit 6%. This is actually in line with some 2024 mortgage rate predictions.

Again, we’ll use our 8% mortgage rate borrower and their $500,000 loan amount to illustrate.

They’d see their monthly P&I fall to $2,997.75, which would represent about $671 in monthly savings.

That’s a pretty big win for someone looking to reduce their monthly housing expense. I can’t think of many other ways to lower your costs.

This is that date the rate, marry the house argument in action.

Refinancing a 5% Mortgage Rate to a 3% Rate

$500k loan amount @5% = $2,684.11

$500k loan amount @3% = $2,108.02

Monthly savings: $576

Remember those 3% mortgage rates that were available in 2021? Well, lots of homeowners with higher-rate mortgages took advantage.

Many were able to reduce their rate from 5% to 3%, saving hundreds per month in the process.

Using our same $500,000 loan amount, the monthly P&I would drop from $2,684.11 to $2,108.02.

That’d represent a monthly savings of $576. While still a big reduction in payment, it’s about $100 less than the prior scenario of going from an 8% mortgage rate to a 6% mortgage rate.

This is why I don’t subscribe to a certain refinance rule of thumb, such as the 1% rule or some other fixed number.

There are countless scenarios, and what works for one borrower may not work for another.

As you can see, it’s easier to save money when refinancing a high-rate mortgage than it is a low-rate mortgage.

Simply put, there’s more room to save if your home loan has a higher interest rate.

Conversely, if you already have a low-rate mortgage, the savings are diminished because your interest expense is small to begin with.

What this means is as mortgage rates improve, borrowers with high-rate loans will find themselves “in the money” for a refinance more easily.

After all, if you can save more money each month, offsetting any upfront costs associated with the refinance will be less of a task. You’ll be able to break even quicker.

And you’ll enjoy more payment relief.

Lastly, your overall interest savings will be greater. We’re talking $242,000 in savings going from 8% to 6% versus $207,000 when going from 5% to 3%.

Total interest paid during 30-year loan term:

3% rate: $258,887.20

4% rate: $359,348.80

5% rate: $466,279.60

6% rate: $579,190.00

7% rate: $697,543.60

8% rate: $820,775.20

Read more: How does mortgage refinancing work?

- Are Mortgage Rates Finally Poised to Start Falling Again? - June 25, 2026

- Mortgage Rates Are Having a Good Day as Oil Prices Fall to Pre-War Levels - June 24, 2026

- You Can Still Get a Sub-6% Mortgage Rate, But Is It Worth It? - June 23, 2026