On a day when mortgage rates are officially close to hitting 8%, I decided to write a post about why they might be a lot lower in 2024.

Call me a contrarian. Or an optimist. Or perhaps just an individual that is looking at data and drawing some conclusions.

While the trend for mortgage rates lately has undoubtedly been higher, higher, higher, we could be close to hitting a peak. I know, I’ve said that before…so much for the mortgage rate plunge.

But maybe we just need to cross that psychological 8% threshold before things can turnaround.

Sometimes you need to see/experience the worst before a recovery can take place.

Here Come the 8% Mortgage Rates…

The threat of 8% mortgage rates might last longer than the 8% mortgage rates themselves, assuming they actually materialize.

This isn’t a new threat. I wrote all the way back in September 2022 to watch out for 8% mortgage rates. At that time, we inched closer to those levels before rates pulled back.

More recently, Shark Tank’s Mr. Wonderful called for the same, arguing that the Fed wasn’t messing around when it came to its inflation fight.

And now it appears he might be right, with the 30-year fixed averaging 7.92%, at least by MND’s daily survey.

But despite higher and higher mortgage rates over the past month and a half, the Fed has become more and more dovish.

There have countless comments of late from Fed speakers essentially signaling a pause in rate hikes. Basically arguing that no further tightening is necessary.

That doesn’t mean 10-year bond yields can’t keep rising, nor does it mean mortgage rates can’t also increase.

While the Fed is saying one thing, everyone else is looking at the data, which continues to come in hotter than expected.

About 10 days ago, it was a big jobs report print, and today it was retail sales coming in much higher than forecast.

Per the Commerce Department, retail sales increased 0.7% in September, more than double the 0.3% Dow Jones estimate.

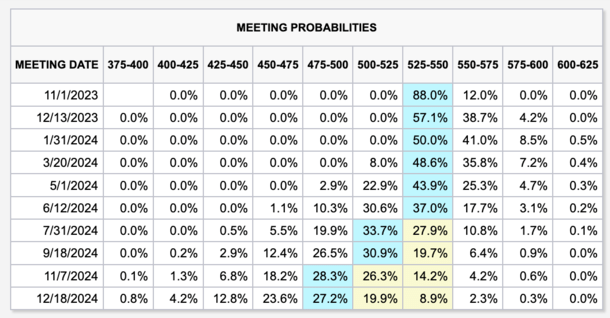

This has pushed the odds of another Fed rate hike up for the December meeting to near parity with a pause.

Per the CME FedWatch Tool, chances of a rate hike at the December 13th meeting are now at 41.9%. That’s up from 32.7% yesterday and 25% a week ago.

Should We Listen to the Fed or the Data?

It’s been a strange contrast lately, with the Fed becoming more dovish as hot data continues to come down the pipe.

But ultimately it appears as if the interest rate traders are more focused on the data than they are what Fed speakers have to say.

Even so, the odds remain ever so slightly in favor of a pause, which is good news for the time being.

Of course, those numbers can change quickly, as evidenced in the daily and weekly movement highlighted above.

And if consumers keep spending, despite economic headwinds and higher prices, it might be difficult to see the cooler economic reports the Fed wants.

However, the Fed may still stand pat at these levels and wait for conditions to deteriorate, as would be expected after 11 rate hikes.

Today, Richmond Fed President Thomas Barkin said the hot data “doesn’t match with his on-the-ground observations that demand seems to be slowing.”

So perhaps we just need more time to let the restrictive monetary policy do its thing. It’s not as if consumers immediately stop spending just because costs are higher.

People still need to buy things, especially gas, groceries, clothing, and other essentials.

And thanks to all the credit floating around, whether it’s 0% APR credits cards or buy now, pay later platforms, the party can continue for a lot longer.

The 10-Year Yield Is Forecast to Fall in 2024, Pushing Mortgage Rates Down with It

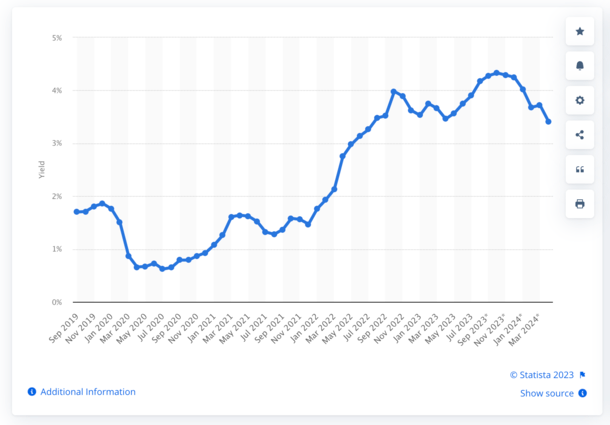

At last glance, the 10-year bond yield, which tracks 30-year fixed mortgage rates pretty well, was a sky-high 4.86%.

Meanwhile, the mortgage rate spread was over 300 basis points, when it’s typically closer to 170.

Combined, that means a yield of 5% would signal 8% mortgage rates. In normal times, it would translate to a rate of say 6.75%. But these are not normal times.

Mortgage rates keep rising and mortgage lenders continue to price defensively as the threat of more inflation and Fed rate hikes remains.

But maybe, just maybe, we are approaching the worst of it, as consumers teeter on the brink of a possible recession.

And perhaps 8% mortgage rates will signal a peak and possible turning point.

After all, the 10-year treasury yield is expected to fall to 3.41% by April 2024, per a September 27th note from Statista.

Meanwhile, Capital Economics market economist Hubert de Barochez predicts the 10-year yield will fall about 80 basis points by the end of the year thanks to slowing growth and the possibility of a mild recession.

De Barochez says this would allow the Fed to cut rates sooner, ideally leading to lower mortgage rates in the process.

Yes, such forecasts are subject to change (or can be completely wrong), but the general consensus is that we’ll be lower by mid-2024 or earlier. Just maybe not that low.

If we take a lower 10-year yield and sprinkle in a more traditional mortgage rate spread, say just 200 basis points, that puts mortgage rates back in the 6% range.

Mortgage rates in the 6s, or even high-5s if paying discount points at closing, would usher in some normalcy to the housing market when it’s rarely been a worse time to buy a home.

If accompanied by a mild recession and some job losses, it could also mean slightly lower home prices as well, instead of a return to bidding wars.

And that could be good for the long-term health of the housing market, which is clearly broken right now.

(photo: Eli Duke)

- Mortgage Rates Could Drop as Much as Half a Percent with Basel Re-Proposal - June 30, 2026

- Mortgage Rates Face Big Week of Jobs Data - June 29, 2026

- Are Mortgage Rates Finally Poised to Start Falling Again? - June 25, 2026