Just when it appeared that the recent rally was running out of steam, mortgage rates sunk even lower.

Despite a lackluster CPI report yesterday that merely met expectations, an updated dot plot and dovish comments from Fed chairman Jerome Powell seemed to do the trick.

That resulted in a big move downward for mortgage rates, which are now the lowest they’ve been since May.

The 30-year fixed is now priced at around 6.75%, or even lower if you pay points.

Ironically, home buyers weren’t thrilled with those rates back then, but they might be moving forward. Thank human psychology.

Why Did Mortgage Rates Fall So Much Today?

The Fed left the federal funds rate unchanged, as was widely expected. So that wasn’t it.

And remember, the Fed doesn’t control mortgage rates anyway.

But along with that announcement, they released an updated dot plot and Fed chair Jerome Powell held a press conference.

In prepared remarks he said, “While we believe that our policy rate is likely at or near its peak for this tightening cycle, the economy has surprised forecasters in many ways since the pandemic, and ongoing progress toward our 2 percent inflation objective is not assured.”

Powell essentially confirmed that the rate hike in July was likely the last for this economic cycle.

He added that, “If the economy evolves as projected, the median participant projects that the appropriate level of the federal funds rate will be 4.6 percent at the end of 2024, 3.6 percent at the end of 2025, and 2.9 percent at the end of 2026, still above the median longer-term rate.”

The federal funds rate is currently 5.25% to 5.50%, so this represents about a one percentage point decrease within a year.

In other words, rate cuts are now in view and not just speculation. Though as Powell said, the economy has to cooperate.

But seeing that inflation has cooled significantly and Fed policy remains restrictive, an easing in rates is possible while continuing the fight toward its two percent goal.

Taken together, rates have likely peaked and cuts are now the next most likely outcome.

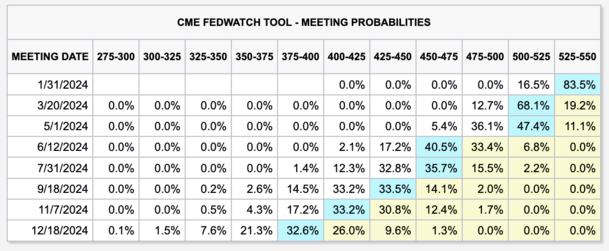

In fact, we could see the first rate cut as soon as January, with the CME FedWatch Tool now giving a quarter-percent cut at the next Fed meeting a 16.5% chance.

It’s more likely that cuts will begin in March though. And by December, the odds are now on a fed funds rate between 3.75% and 4%.

Bond Yields Plummeted After Fed’s Latest Summary of Economic Projections

The Fed’s latest Summary of Economic Projections (SEP) includes the all-important dot plot mentioned by Powell.

That revealed a more dovish outlook from the 12 FOMC participants and that rate cuts are likely in the cards for 2024.

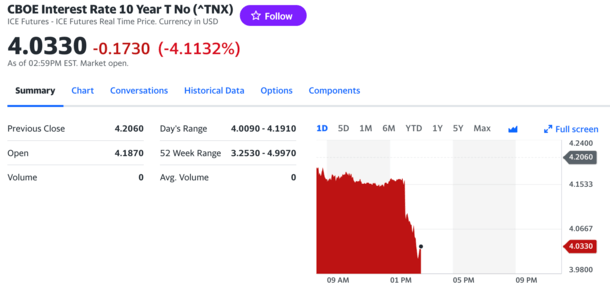

Shortly after the Fed released their statement and updated SEP, the 10-year bond yield dropped about 17 basis points.

It’s now around 4%, well below the near-5% levels seen in late October when mortgage rates peaked.

Simply put, bonds rallied because the economy is no longer overheating, which means the Fed can ease rates.

Mortgage rates tend to follow bond yields. So this rosier outlook resulted in a midday reprice, with many lenders slashing rates by about 0.25%.

The 30-year fixed is now back in the high 6% range, with rates as low as the high 5s if it’s a vanilla scenario and discount points are paid at closing.

Aren’t Mortgage Rates Still Pretty High Though?

Here’s the funny part. While mortgage rates have rallied since late October, they’re still quite high relative to recent levels.

In fact, the 30-year fixed was in the low-to-mid 6% range for much of early 2023. Yes, this year.

And in early 2022, rates were still being quoted in the 3% range, even if it feels like forever ago.

They remained below 6% all the way until the fall of 2022, at which point they began to ascend toward 7% and beyond.

The mortgage rate picture got really bad this past August to October, before they appeared to finally peak.

Rates have since staged a huge rally, dropping from around 8% to 6.75% today. While that’s a big move in a short time span, it really only gets us back to levels seen in late spring.

They remain markedly higher than they were, though due to human psychology, an interest rate starting with a 5 or 6 is going to look (and maybe even feel) good.

After all, if you were used to seeing 7s and 8s, it’s a big improvement, even if it’s not a 3 or a 4 again.

Read more: 2024 Mortgage Rate Predictions from Top Economists

- Are Mortgage Rates Finally Poised to Start Falling Again? - June 25, 2026

- Mortgage Rates Are Having a Good Day as Oil Prices Fall to Pre-War Levels - June 24, 2026

- You Can Still Get a Sub-6% Mortgage Rate, But Is It Worth It? - June 23, 2026