Fannie Mae has rolled out a new version of its automated writing system, known as Desktop Underwriter® (DU®) Version 10.0.

The new version has a number of important changes, two involving consumer credit scores.

Firstly, this release will use trended credit data, which I wrote about back when it was initially announced about a year ago.

This basically allow mortgage lenders to see your balance history on revolving accounts for the past two years, not just the minimum payment and credit limit.

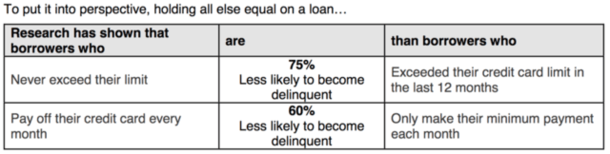

There’s a correlation between carrying a balance and becoming delinquent on the mortgage.

Specifically, borrowers who pay off their credit card debt in full every month are 60% less likely to fall behind on the mortgage versus the borrowers who only make the minimum payment.

That being said, I don’t know how mortgage lenders will view those who revolve their balances. Will they just be further scrutinized, or face some sort of pricing hit that leads to a higher mortgage rate?

I suppose time will tell, but we do know it’s a big deal that it’s being included, with Equifax saying consumers will “see significant update to mortgage decisioning process” after the first tri-merge credit report update in 30 years.

They further note that the inclusion of this new data will “more accurately identify and potentially reward responsible credit behavior,” meaning it could help too.

However, per Fannie Mae, so-called “classic credit scores models” don’t actually use trended data, and these scores can continue to be used by lenders, so at the moment it shouldn’t affect the LLPAs passed onto borrowers.

Eventually, trended credit data may lower/raise credit scores and that can affect your mortgage rate.

Either way, the takeaway is to pay all bills in full each month, not only to save on interest, but to avoid any unwanted attention from your mortgage lender. Also stop swiping months before you apply.

Automated Underwriting for Borrowers with No Credit Scores

Now let’s turn to another key change rolling out with DU 10.0. Fannie will now use automated underwriting (DU) for borrowers who lack the traditional credit necessary to generate a credit score.

Previously, borrowers without credit scores had to have their loan applications manually underwritten, and my assumption is that few lenders made such loans due to the complexity and risk involved.

Beginning with this release, lenders will be able to run the numbers through DU, which should provide both peace of mind and more approvals for borrowers who lack traditional credit.

So if you’re that person who eschews credit, this is great news if you still don’t have several hundred thousand dollars available to purchase a home with cash.

Requirements to Get a Mortgage with No Credit Score

[checklist]

- Owner-occupied single-unit properties only

- 10% minimum down payment

- Max DTI of 40%

- Max loan amount of $417,000

- Must provide two lines of nontraditional credit (one must be housing-related)

- Purchase and rate/term refi only

[/checklist]

If you don’t have any credit scores, lenders will likely be pretty critical of your borrowing profile. Let’s take a look at what Fannie Mae demands in order to get a mortgage without a credit score.

Fannie is the leader in this space so expect most others to follow suit and/or enact similar guidelines.

Most importantly, you must be able to document a “housing-related source of nontraditional credit,” aka rental payments. That must be one of your two nontraditional credit sources. Another might be a cell phone bill or utility payment.

Additionally, you are restricted in what you can purchase. The property must be an owner-occupied, single-unit house or condo, excluding manufactured housing.

Financing is limited to purchases and rate and term refinance transactions – no credit score, no cash out!

The loan amount must be at or below the conforming loan limit of $417,000 (no high balance permitted).

Borrowers must also be able to muster a minimum down payment of 10%. The max CLTV is also 90%, so no getting around that requirement with a second mortgage.

Lastly, your DTI ratio must not exceed 40%, which is a bit lower than the 43% limit for QM loans and the 45-50% allowed under certain circumstances when strong compensating factors are present.

As you can see, it’s not very easy to get a mortgage without a credit score, though Fannie is opening the door a bit more by letting its robot make the decision.

My take is that you’re better off just establishing a traditional credit history. I understand there are individuals who hate credit, but a mortgage is a form of credit, so if you want one, it’s good to have some prior experience…

- Rocket and Redfin Join Forces to Offer Up to $20K in Home Buyer Savings - May 20, 2026

- How Can Mortgage Rates Go Down From Here? - May 20, 2026

- If Bond Yields Are at 52-Week Highs, Why Aren’t Mortgage Rates? - May 19, 2026