If you own a second home or hold a high balance loan amount, you may want to refinance sooner rather than later. That’s assuming you were thinking of refinancing.

The same goes for those planning to purchase a second home or take out a mortgage with a high balance, which is a loan amount above the baseline conforming limit.

The conforming limit for 2022 is $647,200, so if your loan amount will be north of that, take note.

Fannie Mae and Freddie Mac are raising loan-level price adjustments (LLPAs) for both types of transactions come April 1st.

Depending on the details of your loan scenario, this could drastically increase your closing costs and/or mortgage rate.

Second Home Mortgages and High Balance Loans Going Up in Price

In an effort to bolster its support for affordable housing and sustain equitable access to homeownership, the Federal Housing Finance Agency (FHFA) will be raising (LLPAs) for certain transactions.

These LLPAs get passed onto consumers in the form of either more expensive closing costs or higher mortgage rates.

As noted, they pertain to the financing of second homes, whether a purchase or refinance, and high-balance loans, those which exceed the conforming limit.

The idea here is that these types of home loans go toward more affluent individuals. And they also create more risk for Fannie Mae and Freddie Mac, which are backed by taxpayers.

After all, large loan amounts and vacation properties are more likely to default and/or create larger losses for the Enterprises.

And that could jeopardize the mission of Fannie and Freddie, which is mainly to provide affordable financing to first-time home buyers, as well as low- and moderate-income borrowers.

Looked at another way, these new fees will subsidize programs like HomeReady, Home Possible, HFA Preferred, and HFA Advantage, which provide cheaper financing to lower-income borrowers.

Speaking of, fees won’t be going up on those programs, or for first time home buyers in high-cost areas with incomes at/below 100 percent of area median income.

How Much More Expensive Will Mortgage Rates Be in April?

Before you get too worried, the cost of these changes may be minimal, depending on the loan scenario in question.

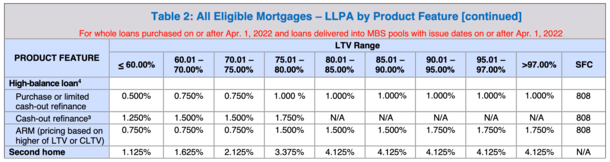

For example, upfront fees for high balance loans will increase anywhere from 0.25% to 0.75%, depending on the loan-to-value (LTV) ratio.

If we’re talking about a loan amount of $750,000 on a primary residence, another .25% in fee is roughly $1,875.

This might move the dial on your 30-year fixed mortgage from 3.25% to 3.375%, or simply increase closing costs.

If that fee is .75% higher due to an LTV of 80%, we’re talking $5,625 in cost, which will more than likely increase your mortgage rate an eighth of a percent or more.

It’s not the end of the world, but it’s yet another thing working against homeowners and home buyers as mortgage rates have started off 2022 higher.

And they tend to peak during spring and early summer, which means financing will be that much more expensive.

The situation is even worse for second home buyers or owners, where pricing adjustments will increase anywhere from 1.125% to a staggering 3.875%.

Using our same loan amount of $750,000, even at a low LTV ratio, the increase in upfront costs could equate to around $10,300.

If we’re talking a high balance loan on a second home at 80% LTV, which isn’t out of the question, it’s an additional cost of about $31,000.

Again, depending on if you let the rate absorb these additional costs, you could be looking at a rate that’s .25% to .50% higher, or more.

Second Home Owners and Those with Large Loan Amounts Should Review Their Mortgages Now

If you believe these changes may affect you, it could be a good time to review your outstanding home loans.

The same goes for prospective home buyers thinking about purchasing an expensive property or a vacation home, which are en vogue due to COVID.

As illustrated above, these higher pricing adjustments have the ability to raise mortgage rates considerably. Or at the very least bump up your closing costs.

With home prices and mortgage rates also seemingly headed higher by spring, it could make sense to accelerate any refinance or home purchase plans to avoid these looming fees.

The FHFA said the new fees won’t go into effect until April 1, 2022 to “minimize market and pipeline disruption,” aka higher pricing for confused customers.

But watch out for mortgage lenders beginning to price in changes earlier on. Simply put, this is yet another reason to make any planned move sooner rather than later.

If you own an investment property, the same types of pricing changes might be on the horizon. So if you’re looking for better terms or cash out, now might be the time.

- Kevin Warsh Throws Cold Water on Lower Mortgage Rates - July 1, 2026

- Mortgage Rates Could Drop as Much as Half a Percent with Basel Re-Proposal - June 30, 2026

- Mortgage Rates Face Big Week of Jobs Data - June 29, 2026