It’s starting to feel a little like 2006 again. Recently, we’ve seen mortgage lenders launching interest-only mortgages, 40-year mortgage terms, and now a company by the name of “ZeroDown” has launched in San Francisco.

Before we worry that it’s the coming of yet another housing crisis, let’s learn more about this startup that aims to tackle the ongoing “affordability crisis” taking place in the Bay Area.

While the name appears to say it all, ZeroDown actually offers even more than a home with no down payment requirement, with a twist.

They let customers make all-cash offers on homes of their choosing and help them close in less than a week.

How ZeroDown Works

- Bay Area residents can buy homes on a lease-to-own basis

- With no required down payment

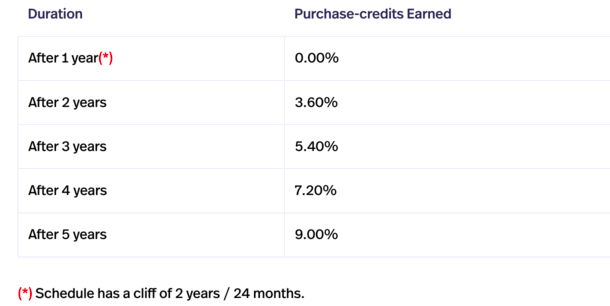

- Can purchase the home after 2 years and up to 5 years later

- Or simply cash out purchase-credits earned during that time

First off, this program is only available in the San Francisco Bay Area, similar to the POPPYLoan that launched a few years back for similar reasons.

Anyway, to get started prospective home buyers fill out an online application to determine eligibility, with a soft credit pull and typical income/asset stuff verified.

Assuming the applicant qualifies, they choose a home to purchase, which ZeroDown pays for in cash.

Customers then have five years to “build up credit toward their down payment” via regular fixed monthly payments that do not change.

With each payment made, borrowers earn so-called “purchase-credits,” which the company likens to stock options (something Bay Area employees might be familiar with).

These credits have a “two-year cliff,” meaning they can be used to purchase the underlying property as long as you live in the ZeroDown home for at least two years.

At that time, you will have the option to purchase the property at a pre-determined price from the company using the credits for down payment, or simply move out and cash out the credits.

You can live in the ZeroDown home for up to five years, at which point you’ll either need to buy it or move on.

So in a sense it’s kind of a rent-to-own situation, since you don’t own or straight up rent the property.

The company owns title to the home and you’re effectively leasing the property with the option to purchase it in the future.

When it comes to maintenance, they will only cover large repairs like an HVAC or roof replacement. If the property has HOA dues, they are your responsibility.

ZeroDown Fees and How They Make Money

- They charge an upfront $10,000 flat fee

- In lieu of typical closing costs associated with a mortgage/home purchase

- And earn some of the real estate agent commission on the buy side of the transaction

- May also earn money on projected home price appreciation

The company charges a one-time flat fee of $10,000 when they make an offer on a home on your behalf.

This compares to the typical closing costs associated with a mortgage, not to mention the sizable down payment requirement.

The good news is they pay for the closing costs associated with the transaction, along with property taxes and homeowners insurance (well, it’s built into your monthly payment to them).

The bad news is monthly payments made to the company aren’t tax deductible, which can make it more expensive.

They also split the buy-side commission with real estate agent partners to earn additional money on the transaction.

Then there’s also the money they may make from the home appreciating in value.

This is determined upfront using average home appreciation in the applicable neighborhood for comparable homes over the past decade.

Doing the Math

Using a hypothetical $1,000,000 acquisition cost for a property in San Jose (I think that gets you a studio), you’d earn the following:

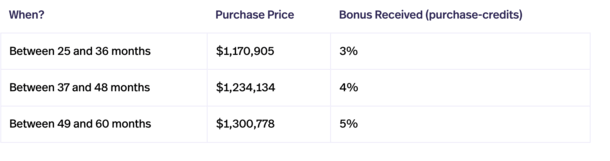

Assuming you stayed for five years then decided to buy the place, the pre-determined sales price at that time might be $1,300,778, citing their example.

They provide bonus credits if you purchase the property (as opposed to cash out), so you could wind up with $90,000 plus an additional $50,000 if I’m interpreting this correctly.

For the record, the monthly payment to them was $6,700 in the example on their website.

In total, you’d have $140,000 to apply toward the down payment on a home now valued at $1,300,778.

That’s a down payment of roughly 11%, leaving the borrower to obtain financing for the remaining 89%.

Many jumbo loan lenders require a minimum down payment of 20%, though there are lenders out there willing to go lower.

At that time, you’d have to arrange traditional mortgage financing using a combination of the credits you received from ZeroDown and any additional money you want to put toward the down payment.

Assuming you can get a loan at 90% LTV, you won’t need additional down payment funds.

But if it turns out you need a 20% down payment, you’ll face a similar predicament as you did when you originally moved in.

Of course, one of the advantages of this new program is flexibility, like most things Silicon Valley.

You can dip your toes in the homeownership waters to see if it’s right for you.

If it turns out it’s not, you simply move on, and even if the property goes down in value over that period, you can still cash out your purchase-credits (they offer downside protection).

The catch is that there’s always a cost for convenience, so the monthly payment during your tenure in the home might be higher than it otherwise would be in a different, more traditional arrangement.

It also begs the question of why you’re quasi-buying a home when you could just rent and buy when you’re truly ready to do so.

But I suppose if there’s a home you just can’t pass up, but can’t afford through traditional means, it could make sense.

- Mortgage Rates Catch a Break as Job Growth Goes Negative - August 7, 2026

- Mortgage Rates Move Higher on Jobs Report Defense - August 6, 2026

- Mortgage Rates Are Now Higher Than They Were a Year Ago - August 5, 2026