With mortgage rates exceeding 7% again and home prices reaching new heights, some critics are sounding the alarm.

The argument is that we’ve got an unhealthy housing market, in which the typical American can’t afford a median-priced home.

And when payments are out of reach, it’s just a matter of time before things correct. It is, after all, unsustainable.

Some are even arguing that it’s 2008 (or whatever early 2000s year you want to use) all over again.

But is the housing market really on the brink of another crash, or is housing simply unaffordable for new entrants?

What Could Cause the Next Housing Crash?

Over the past few years, I’ve been compiling a list of housing market risk factors. Just ideas that pop in my head about what could cause the next housing crash.

I’m going to discuss them to see what kind of threat they pose to the stability of the housing market.

This is what my list looks like at the moment:

- Single-family home investors selling all at once

- Climate-related issues

- Spike in mortgage rates

- Overbuilding (home builders going too far)

- Crypto bust (bitcoin, NFTs, etc.)

- Forbearance ending (COVID-related job losses)

- Mass unemployment (recession)

- Contentious presidential election

- Mom and pop landlords in over heads

- Airbnb and STR saturation (especially in vacation markets)

- Increase in overextended homeowners (high DTIs, HELOCs, etc.)

- Student loans turned back on (coupled with high outstanding debt)

- Buy now, pay later (lot of kicking the can down the road)

The Spike in Mortgage Rates

I had this on my list from a while back, and this one actually came to fruition. The 30-year fixed jumped from around 3% to over 7% in the span of less than a year.

Rates have since bounced around, but generally remain close to 7%, depending on the week or month in question.

However, this hasn’t had the expected effect on home prices. Many seem to think that there’s an inverse relationship between home prices and mortgage rates.

But guess what? They can rise together, fall together, or go in opposite directions. There’s no clear correlation.

However, markedly higher mortgage rates can put a halt to home sales in a hurry, and obviously crush mortgage refinance demand.

In terms of home prices, the rate of appreciation has certainly slowed, but property values have continued to rise.

Per Zillow, the typical U.S. home value increased 1.4% from May to June to a new peak of $350,213.

That was nearly 1% higher than the prior June and just enough to beat the previous Zillow Home Value Index (ZHVI) record set in July 2022.

What’s more, Zillow expects home price growth of 5.5% in 2023, after starting the year with a forecast of -0.7%.

They say that rate of appreciation is “roughly in line with a normal year before records were shattered during the pandemic.”

So we’ll move on from the high mortgage rate argument.

Overbuilding and a Flood of Supply

The next risk factor is oversupply, which would surely lead to a big drop in home prices.

After all, with housing affordability so low at the moment, a sudden flood of supply would have to result in dramatic price cuts.

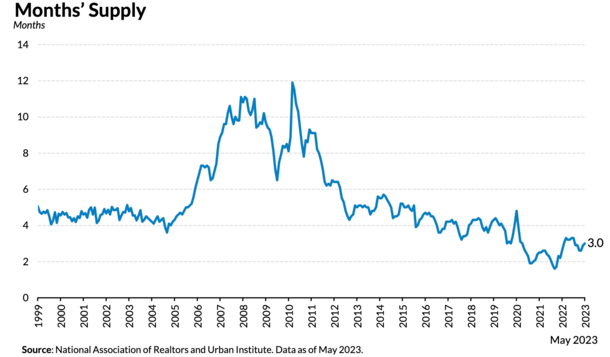

But the problem is there’s very little inventory, with months’ supply near record lows. And it’s about a quarter of what it was during the lead up to the housing crisis.

Just look at the chart above from the Urban Institute. If you want to say it’s 2008 all over again, then we need to get inventory up in a hurry, close to double-digit months’ supply.

Instead, we have barely any inventory thanks to a lack of housing stock and a phenomenon known as the mortgage rate lock-in effect.

Ultimately, today’s homeowner just isn’t selling because they have a super low fixed mortgage rate and no good option to replace it.

But New Construction Isn’t Keeping Up with Demand

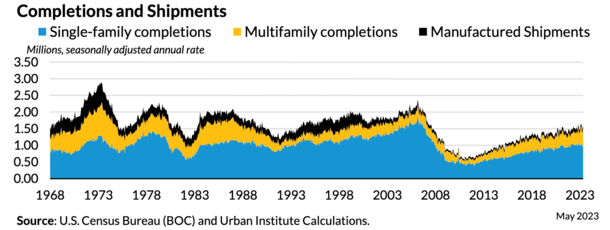

At the same time, new construction isn’t keeping up with demand. As you can see from the chart below, completions are on the rise.

But new residential production, including both single-family and multifamily completions as well as manufactured housing shipments, was only up 2.2% from a year earlier.

And at 1.60 million units in May 2023, production is just 67.2% of its March 2006 level of 2.38 million units.

The other great fear is that mom and pop landlords will flood the market with their Airbnb listings and other short-term rentals.

But this argument has failed to show any legs and these listings still only account for a tiny sliver of the overall market.

What you could see are certain high-density pockets hit if a large number of hosts decide to sell at the same time.

So specific hotspot vacation areas. But this wouldn’t be a national home price decline due to the sale of short-term rentals.

And most of these owners are in very good equity positions, meaning we aren’t talking about a repeat of 2008, dominated by short sales and foreclosures.

A Decline in Mortgage Quality?

Some housing bears are arguing that there’s been a decline in credit quality.

The general idea is recent home buyers are taking out home loans with little or nothing down. And with very high debt-to-income ratios (DTIs) to boot.

Or they’re relying on temporary rate buydowns, which will eventually reset higher, similar to some of those adjustable-rate mortgages of yesteryear.

And while some of that is certainly true, especially some government-backed lending like FHA loans and VA loans, it’s still a small percentage of the overall market.

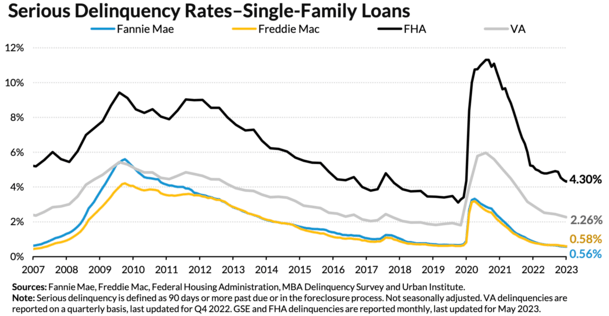

If we look at serious delinquency rates, which is 90 days or more past due or in foreclosure, the numbers are close to rock bottom.

The only slighted elevated delinquency rate can be attributed to FHA loans. But even then, it pales in comparison to what we saw a decade ago.

On my list was the end of COVID-19 forbearance, but as seen in the chart, that seemed to work itself pretty quickly.

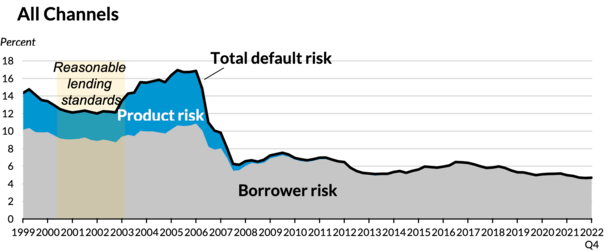

At the same time, lending standards are night and day compared to what they were in the early 2000s. See chart below.

Since 2012, mortgage underwriting has been pretty solid, thanks in no small part to the Qualified Mortgage (QM) rule.

The majority of loans originated over the past decade were fully underwritten, high-FICO, fixed-rate mortgages.

And while cash-out refis, HELOCs, and home equity loan lending has increased, it’s a drop in the bucket relative to 2006.

In the prior decade, most home loans were stated income or no doc, often with zero down and marginal credit scores. Typically with a piggyback second mortgage with a double-digit interest rate.

And worse yet, featured exotic features, such as an interest-only period, an adjustable-rate, or negative amortization.

What About Mass Unemployment?

It’s basically agreed upon that we need a surge of inventory to create another housing crisis.

One hypothetical way to get there is via mass unemployment. But job report after job report has defied expectations thus far.

We even made it through COVID without any lasting effects in that department. If anything, the labor market has proven to be too resilient.

This has actually caused mortgage rates to rise, and stay elevated, despite the Fed’s many rate hikes over the past year and change.

But at some point, the labor market could take a hit and job losses could mount, potentially as a recession unfolds.

The thing is, if that were to materialize, we’d likely see some sort of federal assistance for homeowners, similar to HAMP and HARP.

So this argument kind of resolves itself, assuming the government steps in to help. And that sort of environment would also likely be accompanied by low mortgage rates.

Remember, bad economic news tends to lead to lower interest rates.

Maybe the Housing Market Just Slowly Normalizes

While everyone wants to call the next housing crash, maybe one just isn’t in the cards.

Arguably, we already had a major pullback a year ago, with what was then referred to as a housing correction.

Not easily defined like a stock market correction, it’s basically the end of a housing boom, or a reversal in home prices.

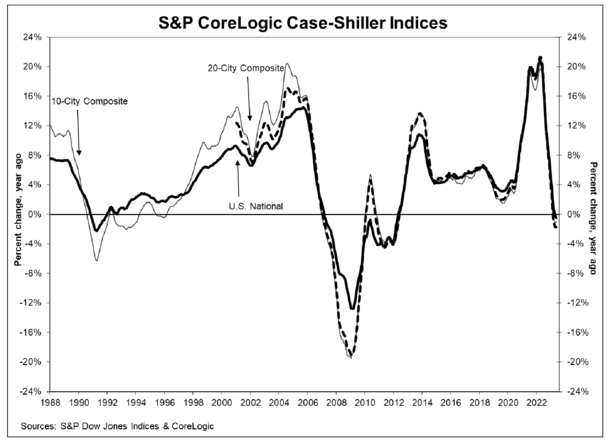

We did recently see home prices go negative (year-over-year) for the first time since 2012, which made for good headlines.

But it appears to be short-lived, with four straight monthly gains and a positive outlook ahead.

Instead of a crash, we might just see moderating price appreciation, higher wages (incomes), and lower mortgage rates.

If supply begins to increase thanks to the home builders and perhaps less lock-in (with lower mortgage rates), prices could ease as well.

We could have a situation where home prices don’t increase all that much, which could allow incomes to catch up, especially if inflation persists.

The housing market may have just gotten ahead of itself, thanks to the pandemic and those record low mortgage rates.

A few years of stagnation could smooth those record years of appreciation and make housing affordable again.

Where We Stand Right Now

- There is not excess housing supply (actually very short supply)

- There is not widespread use of creative financing (some low/0% down and non-QM products exist)

- Speculation was rampant the last few years but may have finally cooled off thanks to rate hikes

- Home prices are historically out of reach for the average American

- Unemployment is low and wages appear to be rising

- This sounds more like an affordability crisis than a housing bubble

- But there is still reason to be cautious moving forward

In conclusion, the current economic crisis, if we can even call it that, wasn’t housing-driven like it was in 2008. That’s the big difference this time around.

However, affordability is a major problem, and there is some emergence of creative financing, such as temporary buydowns and zero down products.

So it’s definitely an area to watch as time goes on. But if mortgage rates ease back to reasonable levels, e.g. 5-6%, we could see a more balanced housing market.

As always, remember that real estate is local, and performance will vary by market. Some areas will hold up better than others, depending on demand, inventory, and affordability.

Read more: When will the next housing crash take place?

- Soft Jobs Report Takes Pressure Off Mortgage Rates - July 2, 2026

- Kevin Warsh Throws Cold Water on Lower Mortgage Rates - July 1, 2026

- Mortgage Rates Could Drop as Much as Half a Percent with Basel Re-Proposal - June 30, 2026