If you haven’t been feeling 30-year mortgage rates recently, maybe an ARM could suit you better.

This is especially true if you don’t plan to stay in the home for a very long period of time.

There are a variety of adjustable-rate mortgages available to homeowners today, with varying fixed-rate periods.

One of the shorter of the hybrid-ARMs, which are home loans that are fixed before becoming adjustable, is the “3/1 ARM.”

Let’s learn more about how it works to see if it could be a good alternative to the 30-year fixed mortgage.

3/1 ARM Meaning

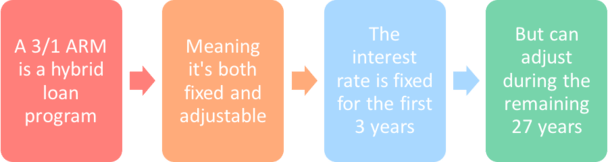

- It’s a hybrid home loan program with a 30-year term

- Meaning it’s fixed before becoming adjustable

- You get a fixed interest rate for the first 3 years

- Then it can adjust once annually for the remaining 27 years

As the name suggests, it’s an adjustable-rate mortgage with two key components.

The first number (the “3”) indicates the period of time in which the mortgage interest rate is fixed. In this case, it’s three years. This means your initial interest rate won’t budge for 36 months.

This is great news if you fear a rate adjustment (higher), and also quite handy if you only need short-term mortgage financing.

The second number (the “1”) represents the adjustment frequency, which as you may have guessed, is annually. Yep, this means the rate can adjust each year once the first three years are up.

For the record, the 3/1 ARM is still a 30-year loan, so you get a fixed rate for the first three years, and an adjustable rate for the remaining 27 years. This is why it’s sometimes referred to as a 3/27 ARM loan as well.

Once those three years are up, your interest rate will adjust based on the margin and associated mortgage index, such as the SOFR.

This is known as the fully-indexed rate (FIR), and is limited by the caps in place, which dictate how much a rate can rise or fall initially, periodically, and over the life of the loan.

Let’s look at an example of a 3/1 ARM:

| $350,000 Loan Amount | 3/1 ARM | 30-Year Fixed |

| Mortgage Rate | 5.375% | 6.5% |

| Monthly P&I Payment | $1,959.90 | $2,212.24 |

| Total Cost Over 36 Months | $70,556.40 | $79,640.64 |

| Remaining Balance After 36 Months | $334,716.08 | $337,460.25 |

| Total Savings | $9,084.24 |

3/1 ARM Rate: 5.375% (for first 36 months)

Margin: 2.5 (fixed for life of the loan)

Index: 1-Year SOFR (5.25% variable)

Caps: 2/2/5

Imagine a 3-year ARM with a start rate of 5.375%, which is fixed for the first 36 months of the loan. During this time, you’d save about $9,000 versus a 30-year fixed priced at 6.5%.

You’d also pay off a little bit more of the loan balance due to the lower interest rate offered.

But you also need to consider what happens for the remaining 27 years.

If the margin is 2.5 and the related mortgage index is 5.25%, your FIR could rise to 7.75%, assuming the caps allowed such movement.

Using our example, the interest rate may adjust 2% above the start rate upon its first adjustment, so an increase from 5.375% to 7.75% wouldn’t be permitted.

Instead, the rate would max out at 7.375%, but it could rise a further 2% at the next adjustment just 12 months later.

Obviously, this would be a big hit to the wallet, which is why most homeowners would look to sell their home or refinance their mortgage before that time.

Unfortunately, mortgage rates may not be attractive during the three-year period after you take out your loan.

It’s also possible that you won’t qualify for a refinance if your credit score or income drops, or if underwriting guidelines change over time. Falling home prices could also dent your plans to refinance or sell.

In short, you’re taking a pretty big risk for a lower interest for 36 months, so have a plan in place if and when rates increase.

3-Year ARM Mortgage Rates

- 3/1 ARM rates can be significantly cheaper than the 30-year fixed

- But the difference in rate will vary bank/lender (some don’t offer a big discount)

- The spread between products can also widen or shrink over time based on market conditions

- Shop around extensively to find a lender willing to give you a 3/1 ARM at a low rate

Now let’s talk about 3-year ARM rates, which as I alluded to, come cheaper than 30-year fixed-rate loans.

How much cheaper is the big question, as the reduced rate will determine if a 3/1 hybrid ARM is worth the risk.

After all, there is plenty of risk involved when your mortgage rate isn’t set in stone. If it can move substantially higher, you could face mortgage payment problems in the near future, and potentially lose your home if things really take a turn for the worse.

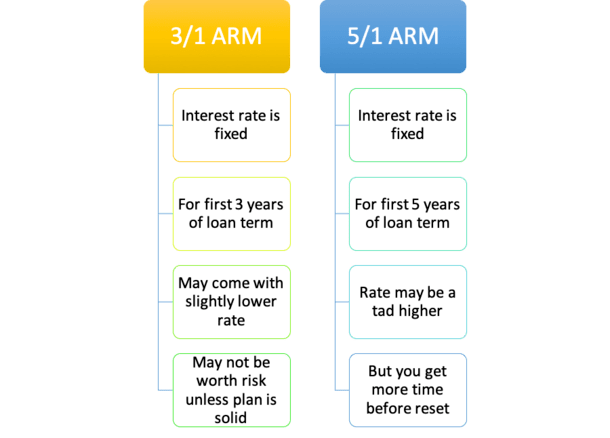

I dug around a bit to see how 3/1 ARM rates stack up against the 30-year fixed and the 5/1 ARM, which offers an additional two years of fixed-rate safety.

I found that rates vary considerably, but can often be significantly cheaper than 30-year fixed-rate mortgages.

For example, I recently saw some 3/1 ARM rates advertised as low as 5.75%, whereas the 30-year fixed was pricing closer to 7%, with no mortgage points on either option.

Of course, I saw tighter spreads too, with some 3/1 ARMs priced at 5.875% or even 6%.

But you should expect a rate discount of at least a percentage point, maybe more if you’re lucky considering the risk involved.

Qualifying for a 3-Year ARM Isn’t Ideal So You Might Want to Skip It

One major drawback to the 3-year ARM is that the qualifying rate used is typically 5% above the note rate.

Yes, you read that correctly. A full five percentage points higher. In other words, if your rate is 5.375%, the lender would need to qualify you at a rate of 10.375%! Good luck getting through underwriting.

This is a rule employed by both Fannie Mae and Freddie Mac that many other lenders follow, including credit unions. Perhaps there are some that don’t, but it’s good to assume this when shopping for an ARM.

Meanwhile, qualifying for a 5/1 ARM is much more favorable for borrowers.

Lenders use the greater of the note rate plus two percentage points or the fully-indexed rate. So that might be a much more reasonable rate of 7.375% in our example.

And because 3-year ARMs and 5-year ARMs are priced fairly similarly, it might make sense just to skip the former altogether and get two more years of fixed-rate goodness.

3/1 ARM vs. 5/1 ARM Pricing

If we compare the 3/1 ARM to the 5/1 ARM, you might only be looking at a rate discount of 0.125% to 0.25%, depending on the lender in question.

One credit union I just checked out was priced at 5.875% for a 3-year ARM and 6% for a 5-year ARM. Barely a difference.

And the 3/1 ARM isn’t even offered by all mortgage lenders. In fact, Wells Fargo, Chase, and Quicken Loans don’t even advertise them, though both openly offer the 5/1 ARM and the 7/1 ARM.

This isn’t to say they definitely don’t offer the 3/1 ARM, it’s just not listed as a loan option.

Ultimately, the 3/1 ARM and 5/1 ARM are pretty similar, so banks and lenders tend to offer the 5/1 ARM instead, especially since it provides two extra years of fixed rates.

Another reason it’s more common today is due to the Qualified Mortgage (QM) rule, which requires lenders to consider the maximum interest rate that may apply during the first five years.

Because 3/1 ARMs will see their first adjustment after just three years, lenders have to consider the fully-indexed rate (margin + mortgage index), which might be a lot higher than the start rate.

As such, the borrower may have more difficulty qualifying for a 3/1 ARM thanks to DTI ratio constraints and the like.

In other words, lenders may just avoid the home loan program altogether in favor of simpler loan types like the 5/1 ARM.

If you’re looking for a jumbo loan, you might have more luck finding this type of mortgage loan as high-net individuals often favor shorter-term financing.

These loans were actually quite popular before the mortgage crisis that took place in the early 2000s, but have since become more of a rarity.

Ultimately, three years can come and go in the blink of an eye, which partially explains their relatively low popularity.

Also Look Out for the 3/6 ARM (The 3/1 ARM’s Cousin)

- Nowadays it’s common to see the 3/6 ARM advertised as well

- It’s also an adjustable loan and fixed for the first three years

- But it adjusts twice annually after the first 36 months of the loan term

- This means you have two adjustments per year to worry about

Another common variety of three-year ARM is the “3/6 ARM,” which works pretty similarly to the 3/1 ARM.

The only difference is that after the first three years, the loan adjusts semi-annually (twice per year).

So you get two adjustments each year during years 4-30. Every six months, there will be an adjustment.

This makes the 3/6 ARM more work, as you have to pay closer attention to the corresponding rate index.

It seems mortgage lenders are favoring the six-month adjustment period over the 12-month adjustment a lot more these days.

Don’t be surprised to find that they only offer the 3/6 ARM vs. the 3/1 ARM. But if you only keep it for the first three years or less, it won’t matter.

It could technically work in your favor if rates are moving lower and your rate goes down every six months instead of once annually. But don’t count on it!

I also recently found a 3/5 ARM being advertised by Navy Federal CU, which is fixed for the first three years, then it adjusts every five years. So year 4, year 9, year 16, and so on.

3/1 ARM Pros and Cons

The Good

- You can get a lower mortgage rate relative to other loan options

- The rate is fixed for the first 3 years (36 months)

- This will allow you to save money and pay down your loan balance faster at the same time

- Can always refinance, sell your home, or prepay your mortgage before it adjusts if approved

The Bad

- The interest rate will adjust after just 3 years

- Harder to get approved because the lender must use a higher qualifying rate

- Depending on the caps the rate could jump up considerably

- May have difficulty making higher mortgage payments

- Rate may not be discounted enough to justify the risk of a rate reset

- Could be stuck with the loan if you can’t refi/sell/prepay

- Mortgage Rates Catch a Break as Job Growth Goes Negative - August 7, 2026

- Mortgage Rates Move Higher on Jobs Report Defense - August 6, 2026

- Mortgage Rates Are Now Higher Than They Were a Year Ago - August 5, 2026