If you’re currently the proud owner of a mortgage, you’ve undoubtedly heard of a cash-out refinance, one that allows you to tap into your home equity.

They were quite popular during the early 2000s housing boom, when homeowners serially refinanced and simultaneously pulled “cash” from their homes while property values skyrocketed.

You may have also heard the phrase, “using homes as ATM machines.”

Well, the downside to this seemingly lucrative practice is that mortgage balances also grow when you refinance.

You don’t just get free money. If you refinance and pull cash out, your loan amount grows, no ifs, ands or buts about it.

This can eventually lead to issues if you need to refinance again in the future, or even if you wish to sell your property.

If at some point your outstanding mortgage balance exceeds the property value, you could wind up with an underwater mortgage.

Did You Run Out of Home Equity?

- Many borrowers serially refinanced during the early 2000s housing boom

- And zapped all their home equity in the process

- At the same time home prices dropped rapidly

- Making it impossible to refinance via traditional channels

When the housing appreciation party came to a sudden end around 2006, many of these homeowners became the proud owners of underwater mortgages – that is, they owed more on their mortgages than their properties were worth.

For example, a home buyer may have acquired their property for $400,000, then eventually refinanced it at a value of $500,000.

If they pulled out the maximum amount of cash, which was often 100% LTV/CLTV back then, any price drop would mean they were in a negative equity position.

Original home price: $400,000

Original loan amount: $400,000

New value: $500,000

New loan amount: $500,000

Latest appraised value: $475,000

The scenario above was quite common back in the early 2000s. A home buyer would purchase a property with zero down financing, then eventually apply for a cash-out refinance as the value rose.

This was clearly unsustainable, and eventually led to a massive housing bubble and subsequent burst.

It also led to record low negative equity levels, with millions holding underwater mortgages.

Unfortunately, you typically can’t even do a rate and term refinance if you’re underwater on your mortgage, meaning those looking for payment relief were effectively shut out.

Eventually, programs came along to address the situation, such as the Home Affordable Refinance Program (HARP), which had no upper limit on LTV ratio. In other words, even if you were deeply underwater, you could still apply for a rate and term refinance.

Is It Time to Bring Back a High LTV Refinance?

Times are a lot different today, but with home prices seemingly plateauing in many cities nationwide, and even falling in others, a similar scenario could unfold.

While existing home sales hit their lowest level in nearly 30 years, we still saw about four million transactions take place.

There are also the new-builds, which have grabbed more market share in recent years as affordability tanked with significantly higher mortgage rates.

This means there might be a cohort of borrowers who find themselves in an underwater position if home prices don’t manage to eek out gains, and instead fall.

While I’m optimistic we’ll avoid a full-blown housing crash, it’s possible some might fall into negative equity positions.

The HARP option is long gone (it came to an end in late 2018), and replacements like Fannie Mae’s High LTV Refinance Option have also been temporarily paused due in part to low volume.

There just hasn’t been a need for it lately. But could that change? And if so, what is another solution for those needing to refinance?

One Option for the Underwater Homeowner is a Cash-In Refinance

As noted, the high-LTV refinance options have been been put to rest due to a lack of need. Most homeowners are in a great spot today.

Part of that is due to massive home appreciation since the housing bottom around 2012-2013. The other piece is the ATR/QM rule, which banned risky loan features like interest-only and 40-year loan terms.

Borrowers also increased their down payments in recent years, sometimes to win a bidding war. And LTVs have also been massively reduced on cash-out refinances.

The end result is the highest amount of home equity on record, with few borrowers actively tapping into it.

But as I said, there might be cases for recent home buyers, who may have seen prices fall since they purchased a property.

Unfortunately, these same buyers may have also been saddled with a much higher mortgage rate, perhaps something in the 7-8% range on a 30-year fixed.

If and when rates fall and they apply for a refinance, they may find that they’re a little short.

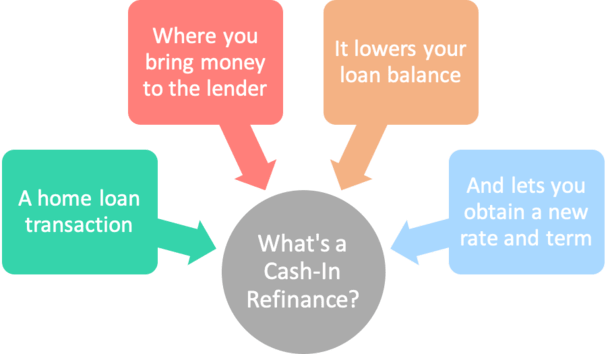

So what are they to do? Enter the “cash-in refinance.”

Simply put, a cash-in refinance is the opposite of a cash-out refinance. When homeowners apply for a cash-in refinance, they bring money to the closing table to lower their mortgage balance.

This allows them to satisfy any LTV limits and qualify for the loan. For example, Fannie Mae has a maximum 97% LTV for a rate and term refinance.

So if your mortgage balance is $502,000 and the home is only appraised at $515,000, you’ll have a problem.

Let’s look at an example of a cash-in refinance:

Purchase price: $525,000

Current home value: $515,000

Mortgage balance: $502,000

Maximum loan amount: $499,550 (97% LTV)

Imagine a homeowner who purchased a property for $525,000 with 3% down in late 2023 when mortgage rates peaked (hopefully) and today, unbeknown to them, it’s worth only $515,000.

They see that mortgage rates are now closer to 6.5% and apply for a rate and term refinance, using an estimated value of $540,000.

The home is appraised and the value comes in low, at just $515,000. The max loan amount at 97% LTV is $499,550 and they still owe $502,000.

The borrower must come up with $2,450 (plus any closing costs) to make up the shortfall and accomplish the cash-in refinance.

Doing so would put their LTV at 97%, which is the max allowed for a conforming loan.

Assuming the borrower has the funds available, they could bring in this money to get the loan amount down to an acceptable level.

Why a Cash-In Refinance?

- To lower your loan amount to an acceptable level

- That is at/below the max LTV allowed by the lender

- Or to keep it at/below a certain threshold like 80% LTV

- To avoid mortgage insurance and obtain a lower interest rate

- Also to stay at/below the conforming loan limit

Borrowers may need a cash-in refinance for several different reasons.

Probably the most common reason in the past decade had to do with the underwater homeowners I just mentioned.

Those short on home equity pretty much have no choice but to bring cash in to qualify for the refinance in question.

In other words, they won’t qualify unless they pay down their mortgage balance to a suitable level.

Lately, this has been any level at/below 97% LTV, which is the typical maximum allowed by conventional mortgage lenders.

Note that FHA and VA borrowers can take advantage of a streamline refinance, which allows borrowers to use the original purchase price for the LTV and/or allows LTVs above 100%.

However, cash-in refinances aren’t just for the distressed homeowner. Borrowers can also utilize them in order to lower their loan balances so they can qualify for a lower mortgage rate.

An example would be a homeowner whose outstanding loan balance puts them at say 90% LTV.

If they bring in another 10%, their LTV drops to 80%, pushing their interest rate lower thanks to more favorable pricing adjustments.

At the same time, they avoid the need for mortgage insurance, which can cost hundreds per month.

Bringing in cash will also lower your loan amount, which equates to a lower monthly mortgage payment and reduces the amount of interest you pay throughout the life of the loan.

So it’s a triple win: smaller loan amount, lower interest rate, and no MI!

Another reason to bring in cash is to ensure the conforming loan limit isn’t exceeded, thereby avoiding jumbo loan pricing.

It can be more difficult to obtain a jumbo home loan, or the pricing may just be less favorable, so a borrower may choose this type of refinance to keep costs down and improve approval chances.

[Can you refinance with negative equity?]

Why a Cash-In Refinance May Not Always Be the Best Move

- Consider the alternatives for your cash

- You might be able to earn more elsewhere

- Such as in a retirement account or another investment

- Remember to diversify your assets and maintain liquidity

All of the above sounds pretty awesome, right? Well, unless you have to bring in cash to qualify for the refinance, it might not always be the best move.

If your money will earn more in an investment account, paying down your mortgage early won’t necessarily be the right choice. The same basic principle applies here.

But do the math if you’re close to a certain LTV threshold, and the mortgage rate could be much lower. Especially if you’re close to 80% LTV and can get rid of mortgage insurance!

Just note that if home prices slip further or you need cash for an emergency, having it locked up in an illiquid investment won’t do you much good.

Sometimes it’s best to keep less money tied up in the home, and perhaps put more time in shopping for a more competitive rate.

Read more: What is a short refinance?

- Mortgage Rates Could Drop as Much as Half a Percent with Basel Re-Proposal - June 30, 2026

- Mortgage Rates Face Big Week of Jobs Data - June 29, 2026

- Are Mortgage Rates Finally Poised to Start Falling Again? - June 25, 2026