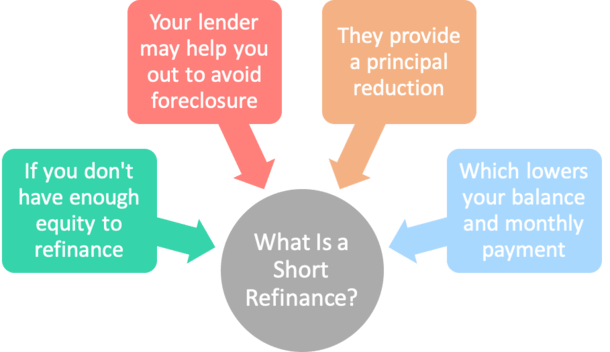

A “short refinance” is a transaction in which your bank or mortgage lender agrees to pay off your existing mortgage and replace it with new a loan with a reduced balance, essentially helping you avoid foreclosure.

In that sense, it’s more a loss mitigation tool than it is a standard refinance loan.

It benefits both the bank and the homeowner, as the bank ideally loses less than they would via foreclosure, and the homeowner gets to stick around in their property.

A Short Refinance to Save Your Home

- A short refinance may allow you to keep your home

- Even if you can’t afford your existing mortgage(s)

- The lender provides a principal reduction

- That lowers your monthly mortgage payments to affordable levels

A short refinance is a cross between a short sale, which involves selling your home for less than the existing lien(s), and a rate and term refinance, where you replace an old loan with a new one.

So why would someone want to execute a short refinance anyway?

Well, if property values plummet, and millions of homeowners are upside down on their mortgages, meaning they owe more on their home loan(s) than the property is worth.

Short Refinance Example

Purchase price: $500,000

Mortgage balance: $450,000

Current home value: $400,000

Short refinance loan amount: $380,000

Forgiven debt: $70,000

In the above scenario, the homeowner wouldn’t be able to refinance without bringing in at least the $50,000 difference between current appraised value and existing mortgage balance.

In reality, the homeowner would need to bring in even more money to execute a traditional refinance because most banks and lenders no longer offer mortgages with no money down, and closing costs would also need to be considered.

This can be a huge roadblock for homeowners looking to take advantage of the record low mortgage rates currently on offer, especially those experiencing difficulty paying the mortgage every month.

The short refinance is a great solution for distressed homeowners because it not only reduces the loan balance to an LTV below 100%, but also comes with a fresh interest rate, likely one lower than what the borrower had before.

The result is a significantly reduced monthly mortgage payment, enough to keep the homeowner in their property.

The drawback is actually convincing a bank or lender to offer you a short refinance, as it’s not necessarily in their best interest (or the investor who actually owns the mortgage).

Unless they’re completely certain you’ll default on the loan, and the eventual foreclosure will be more expensive for them.

Either way, it could takes months to get a short refinance done, and there’s never any guarantee it’ll happen.

If one is eventually granted, the bank will essentially settle your old debt for less, which will probably harm your credit score too depending on how it’s reported.

Of course, the impact may be similar to that of a foreclosure or short sale, so it’s not necessarily any worse than the alternatives, especially if you can’t keep up with mortgage payments.

Short Refinance Advantages

- You keep your home

- You get a reduced mortgage balance

- You may get a lower interest rate

- You get equity in your home

- Reduced monthly payment

Short Refinance Disadvantages

- Hurts your credit score

- Time consuming

- No guarantee the lender will actually approve it

- Need to qualify with full documentation

If you’re interested in getting a short refinance done, contact your lender to see if they’re willing to work with you.

If not, you might want to explore other options, such as HARP 2.0, which no longer carries any LTV constraints.

This is now known as a High Loan-to-Value Refinance.

These days, mortgage lenders are more likely to offer a solution that doesn’t reduce your principal balance on their dime, which explains the popularity of programs like HARP.

Read more: How to refinance with negative equity.

- Mortgage Rates Could Drop as Much as Half a Percent with Basel Re-Proposal - June 30, 2026

- Mortgage Rates Face Big Week of Jobs Data - June 29, 2026

- Are Mortgage Rates Finally Poised to Start Falling Again? - June 25, 2026